ON DECK FOR FRIDAY, SEPTEMBER 22

KEY POINTS:

- A calmer end to the week may be in store for markets...

- ...after gullible markets believed in the Fed’s random dots

- BoJ’s Ueda tamps down speculation about policy shifts that he provoked...

- ...but Japanese core inflation keeps it alive

- Mixed global PMIs

- UK retail sales post a mild rebound

- Canada to update retail sales for July and August

Global markets are sailing into the weekend under relatively more stable conditions compared to the volatility we’ve seen on other days this week. The week's main event was no doubt the Fed and the market's extreme gullibility when it came to believing the little scribbled dots that Committee participants jot down on paper about next year's intentions and thereafter that showed a more modest pace of rate cuts than previously. In reality, the dots are largely useless in terms of forecasting what actually happens and are dirtied by the objective of trying to micro manage markets. I’m biased to fading the curve reaction and have difficulty understanding how most folks know the dots are of extremely limited use and yet the herd followed them by chasing 2s10s bear steepeners.

Sovereign bonds are slightly richer across gilts, EGBs and US Ts. N.A. equity futures are up by ¼% to ½% and with London performing similarly versus as slightly negative bias across the rest of Europe. Asian equities saw a strong 2.3% gain in HK and 1½% to 2% gains at mainland China’s exchanges amid speculation toward further pending stimulus measures. The USD is a bit firmer mainly against the yen, sterling and euro.

Drivers include no surprises from the BoJ and mixed but generally mild data surprises. US auto strike action may intensify today.

The BoJ left its policy rate and 10-year JGB yield target range unchanged while Governor Ueda declined to speculate on if and when further policy adjustments may be delivered. He generally leaned on the need for continuing stimulus including this quote:

“Because we aren’t in a state where inflation accompanied by wage growth—sustainable and stable inflation—is in sight, we’re patiently continuing with monetary easing under the current framework.”

That walked back his earlier casual remark. Ueda recently said that the chances of ending negative rates into year-end “aren’t zero” if further evidence of wage and price pressures emerges. The selective hearing of markets heard “what, he’s ending negative rates?!” Anonymous BoJ officials subsequently put out guidance indicating markets went too far and Ueda did not pursue the topic any further. The yen softened overnight and the curve slightly richened.

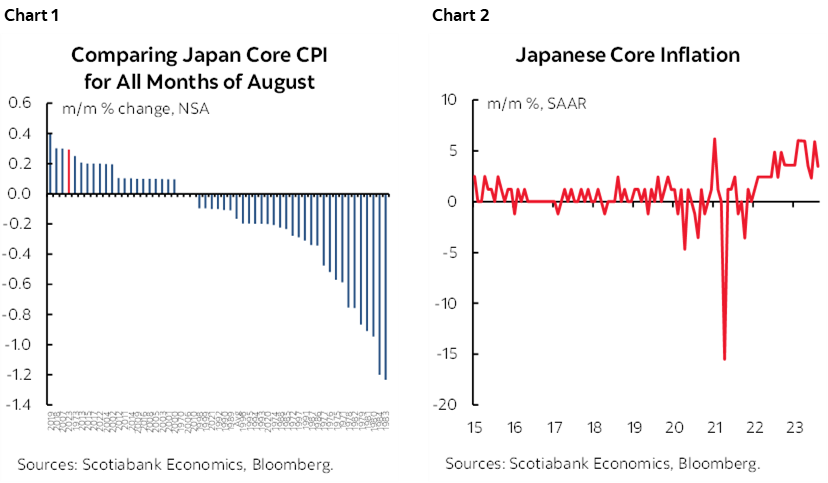

Just before the BoJ delivered its communications, Japanese core CPI put in among the strongest readings compared to like months in history (chart 1). Core CPI in seasonally unadjusted terms declines more often than not in August, but this time it was up by about 0.3% m/m NSA for the fourth strongest gain on record. That has been a generally persistent pattern all year (chart 2) and if it continues while being accompanied by ongoing wage gains then the BoJ may very well take another step to the exit over coming meetings. When it does so, it will be a surprise given the central banks proclivity toward catching markets off guard twice since December.

A wave of global purchasing managers indices for September arrived overnight. Charts 3–6 illustrate one reason why they can matter given correlations to GDP growth.

- Australia’s composite PMI climbed 2.2 points to 50.2, signaling mild improvement in the economy driven entirely by a jump in the services PMI (50.5 from 47.8) as manufacturing’s decline accelerated (48.2 from 49.6).

- Japan’s composite PMI fell to signal softer growth (51.8 from 52.6). Both services (53.3 from 54.3) and manufacturing (48.6 from 49.6) weakened.

- The UK economy deteriorated as the composite PMI fell further into contraction (46.8 from 48.6) as a worsening in services (47.2 from 49.5) offset a slightly slower pace of decline in manufacturing (43.4 from 43.5).

- The Eurozone composite PMI was little changed and remained in contraction (47.1, 46.7 prior) as a slightly softer pace of contraction in services was accompanied by little change in the pace of contraction in manufacturing).

UK retail sales were in line with expectations as a mild rebound from the prior month’s weakness unfolded in August. Sales were up 0.4% m/m with ex-gas up 0.6%.

Canada will also update retail sales this morning (8:30amET). Statcan had previously guided that sales were tracking a small gain of 0.4% m/m SA. It will also provide preliminary guidance for August sales. Canada’s numbers will inform July and August GDP tracking but it would take a large surprise to deviate from my current estimate of mild growth for July.

The US updates the S&P PMIs (9:45amET) that speak to global operations of US companies versus the Fed’s preferred ISM gauges that focus upon domestic operations.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.