ON DECK FOR THURSDAY, SEPTEMBER 21

KEY POINTS:

- The Fed’s aftermath is dominating risk-off sentiment…

- …even as a couple of other central banks got cold feet

- Markets are ill-advised to take the FOMC’s dots so literally

- BoE holds, opts for higher for longer, increases QT pace

- SNB holds with a tightening bias

- Riksbank hikes, guides more to come, sells reserves

- Norges Bank hikes and says it will hike again in December

- BI, BSP, CBCT hold

- Turkey’s central bank hike 500bps and the lira still fell again

- SARB is expected to hold

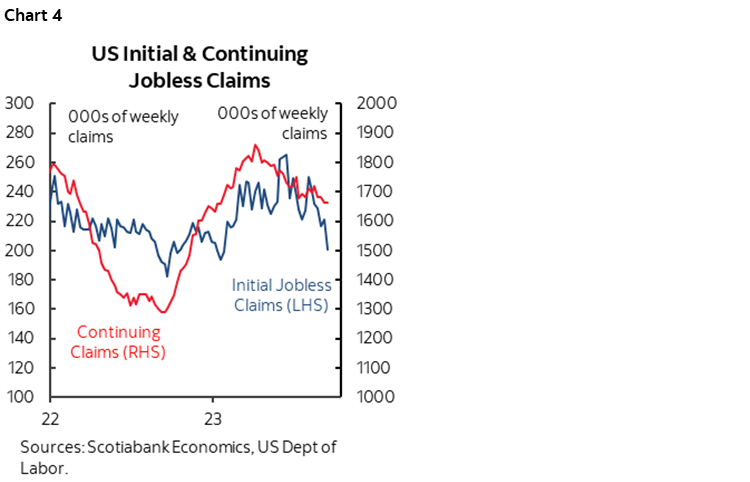

- US initial jobless claims drop to the lowest since January

- US Philly Fed plunges, home resales on tap

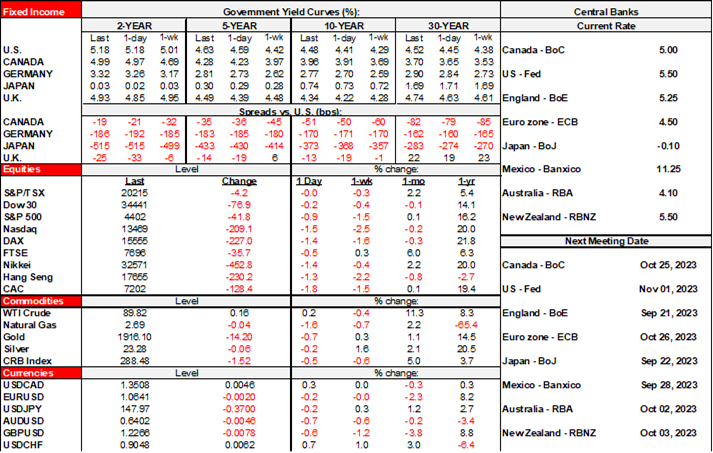

While a couple of central banks got cold feet this morning, global markets are primarily being influenced by carry over effects from yesterday afternoon’s Fed decision and whether that affects the outlook for multiple other central banks. The dollar is broadly stronger, except against the yen. Equities are broadly lower with European cash markets all down by 1½–2%, except for a milder ½% drop in London after the BoE whiffed and following widespread declines of 1–2% across Asian equity benchmarks. N.A. equity futures are down by about ½% to over 1% across the main benchmarks. Sovereign yields are up by single digit basis points across gilts and EGBs after Australia’s curve underperformed the most. There is little carry over into the N.A. front-ends this morning but the rest of the US Treasury and Canada curves are slightly cheaper.

It all boils down to the believability of the Fed’s dots and I have to admit that I’m a bit surprised by the extent to which markets suddenly believe in the dot plot. This recap was sent yesterday.

I don’t have a big quibble with the FOMC showing a further hike this year that will come down to monitoring the data; if the string of softish core inflation gauges continues and/or payrolls and other data sharply disappoint then maybe that doesn’t get delivered. Or perhaps they deliver it as a final insurance hike as per comments this morning by former St. Louis Fed President Bullard.

If markets are reacting to the higher for longer guidance that cut in half the magnitude of cuts next year, then that’s where the rub lies in my view. The dots are largely useless beyond the near term and have at best a soft track record in terms of lining up with what actually happens to the policy rate (chart 1). The dots are one part what the Committee members think may happen and one part dirtied by efforts to control markets through an extension of the Fed’s long history of seeking to manipulate them. The FOMC doesn’t wish to have anyone piling into rate cut pricing just yet and is not yet prepared to ring the all clear on a final hike. That day will come, but not yet.

Furthermore, recall the roughly three percentage point range of opinions on the magnitude of easing in 2025 that Committee members anticipate. They have no better idea what will happen by then than markets do.

The Bank of England decided to leave Bank Rate unchanged at 5.25% in a close 5–4 vote while unanimously deciding to increase the pace of reducing holdings of gilts by £100B over twelve months starting in October from £80B over the past year. The minutes (here) described today’s decision as “more finely balanced” between doing too much and too little.

"Given the significant increase in Bank Rate since the start of this tightening cycle, the current monetary policy stance was restrictive. This meant that the decision on whether to increase or to maintain Bank Rate at this meeting had become more finely balanced between the risks of not tightening policy enough when underlying inflationary pressures could still prove persistent, and not placing sufficient weight on the impact of the previous tightening that was still to come through on activity and inflation."

“Monetary policy will need to be sufficiently restrictive for sufficiently long to return inflation to the 2% target sustainably in the medium term, in line with the Committee’s remit. Further tightening in monetary policy would be required if there were evidence of more persistent inflationary pressures.”

This bias toward higher for longer instead of more now heavily rests upon whether markets believe the MPC. Voters who preferred to pause including Governor Bailey, Broadbent, Dhingra, Pill and Ramsden while those preferring to hike again included Cunliffe, Greene, Haskel and Mann. No forecasts or press conference accompany this decision.

Here are brief highlights of the other overnight central bank decisions:

- Brazil's central bank cut the Selic rate 50bps to 12.75% as expected last evening.

- SNB unexpectedly held at 1.75% as inflation has ebbed and guided that further tightening may be required.

- Sweden's Riksbank hiked 25bps to 4% as expected, announced it was selling a quarter of reserves and guided the possibility of one more hike. The updated forward path is shown in chart 2.

- Norges Bank hiked 25bps to 4.25% as expected and guided to expect another 25bps hike in December. The updated forward path is shown in chart 3.

- BSP held at 6.25% as expected.

- BI held at 5.75% as expected.

- CBCT held at 1.875% as expected.

- Turkey’s central bank hiked its one-week repo rate by 500bps to 30%. It has been raised by 22.5% since May. What has the lira done? It’s weaker again this morning and has been selling off throughout the hiking campaign. The country remains in the throes of a currency crisis as restoring policy credibility post-election after President Erdogan destroyed it cannot be achieved overnight.

The South African Reserve Bank is expected to hold again at 8.25% at around 9:15amET.

Data risk is light. NZ Q2 GDP solidly beat expectations at 0.9% q/q SA non-annualized (0.4% consensus).

US weekly initial claims fell to 201k last week and therefore to their lowest level since the start of the year (chart 4). So much for the theory that seasonal adjustments may not have controlled for Labor Day holiday effects leading up to and in the week of the holiday as well this year as in the past since that might have given way to a reversal higher last week. The US job market appears to remain in strong shape.

The Philly Fed’s gauge is a bad omen for ISM-manufacturing, but the drop to –13.5 in September from +12 on weaker new orders and higher prices was ignored by markets in favour of the claims data. Existing home sales for August (10amET) are also on tap.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.