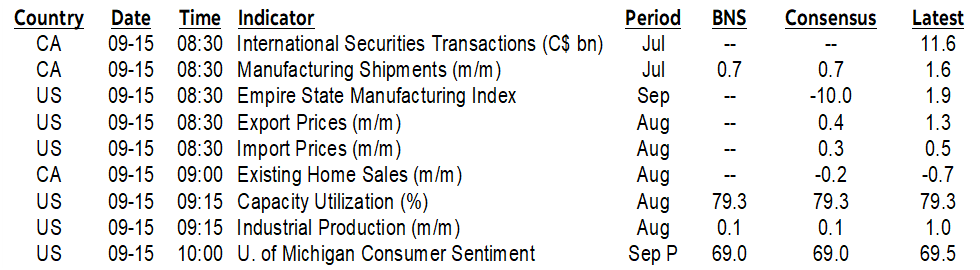

ON DECK FOR FRIDAY, SEPTEMBER 15

KEY POINTS:

- Risk-on appetite is encouraged by China’s economy

- China’s economy rebounded in August

- PBOC holds after RRR cut, injects liquidity

- Markets shake off the ECB’s wishy-washy all-options-open decision

- US autoworkers begin targeted strikes…

- …with limited likely effect on September payrolls

- The UAW is emboldened by NAFTA 2.0 changes

- Peru’s central bank cut and joined its LatAm peers

- BoJ officials indicate overreaction to Ueda’s remarks

- Russian central bank hikes 100bps

- US industrial output is expected to be soft after Empire soared

- US UMich to inform how consumer sentiment is holding

- Canada is recording evidence of rebounding activity

- Canada’s populist assault on grocery chains

Global markets are in risk-on mode across asset classes partly driven by rebounding China macro data. The USD is broadly softer. Stocks are rallying with European cash markets up by between ½% and 1½% following gains of about 1% in Tokyo and Seoul, ¾% in HK and slight declines across mainland China. N.A. equity futures are by led higher by the TSX’s ½% rise amid little change in US stocks. Oil is up another few dimes.

The UAW is on strike right into the nonfarm reference period which is the pay period including the 12th day of each month, and at the tail end of the companion household survey’s reference week. A modest effect on September payrolls is likely, given the timing but also the fact that so far only a fraction of 150,000 workers walked out in targeted strikes. A long strike is feasible, given that the union is aggressively seeking a 36% pay hike over a 4-year contract period plus a COLA clause, fewer temp workers, increased benefits and a shortened work week to 32 hours from 40. Righto. Good luck with that. See below for comments on how NAFTA 2.0 fits into this.

Anonymous BoJ officials indicated in a Bloomberg story that the market overreacted to Governor Ueda’s comments on the possibility of moving away from a negative policy rate. The yen softened and JGBs were flat but outperformed other global benchmarks.

China’s central bank held its 1-year Medium-Term Lending Facility Rate unchanged at 2.5%, preferring to rely upon yesterday morning’s RRR cut. A net 258B yuan withdrawal of 7-day repo liquidity was accompanied by a net 191B liquidity injection through the term facility.

Chinese macro indicators rebounded in August, easing fears about mounting near-term downside risks to the economy. Retail sales were up 4.6% y/y (3% consensus, 2.5% prior) and 0.3% m/m SA following a flat print in July. Industrial production was up 4.5% y/y (3.9% consensus, 3.7% prior) and 0.5% m/m SA after a flat print in July. Fixed asset investment was stable at 3.2% y/y. The jobless rate ticked lower to 5.2%.

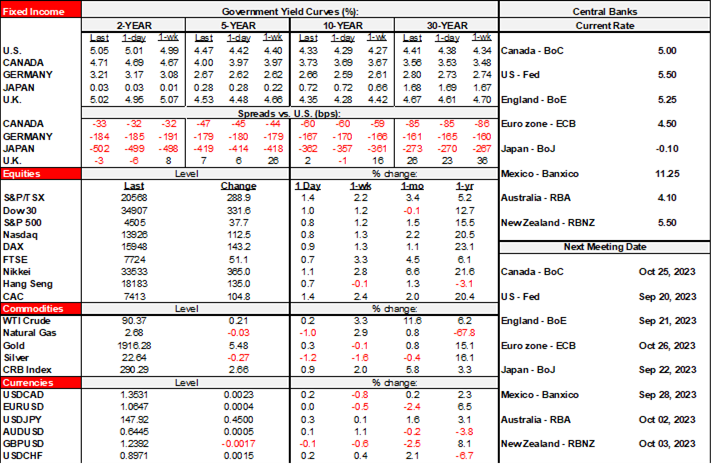

The ECB’s decision yesterday is having little to no real durable effect on EGBs net of other developments. Why? Because the language used in the statement and frequently referred to by President Lagarde during the press conference was so wishy washy that it left open options to either hold at current levels for as long as data informs such a bias, or to continue hiking. Markets are pricing in a partial chance at a further 25bps hike by year-end. Key are the following points:

- The obvious first point is that they hiked by 25bps when it wasn’t fully priced and consensus was divided. That’s an obviously hawkish initial starting point.

- The statement said “Based on its current assessment, the Governing Council considers that the key ECB interest rates have reach levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return to the target.” You could look at this as introducing the prospect of a long hold period, or you could say it’s not quite that strong because they say the current rate will only make a “substantial” and hence incomplete contribution to achieving 2% inflation.

- “The Governing Council’s future decisions will ensure that the key ECB interest rates will be set at sufficiently restrictive levels for as long as necessary.” The tense is what matters here. They are not necessarily saying they are at sufficiently restrictive levels and are instead saying that they “will” strive to be.

- “The Governing Council will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.” Phew. Basically this continues to say that they will craft decisions by following the data versus pre-committing a bias ahead of decisions. Such is the era we’re in now at the fine-tuning stage for monetary policy.

Peru’s central bank joined its LatAm peers by cutting the reference rate by 25bps to 7.5%. Forward guidance leaned against going in a straight-line path of further reductions by saying “This decision doesn’t necessarily imply a cycle of successive reductions in the interest rate.”

Russia’s central bank surprised with a 100bps hike in the key rate to 13% that only a minority within consensus anticipated. The ruble has been steadily depreciating this year and CPI inflation jumped to 5.2% y/y in August from 4.3% the prior month as core CPI was up 0.75% m/m and 4% y/y.

Canadian manufacturing data supports the rebound narrative. Sales were up by 1.6% m/m in nominal terms during July which blew away the initial ‘flash’ guidance by about a full percentage point. Volumes were up by 0.9% m/m and so it wasn’t just higher prices that drove sales up. We now have rebounding manufacturing plus wholesale sales volumes that were slightly higher the other day, alongside gaisn in hours worked during Q3 to point to by way of some of the rebound evidence. Also watch existing home sales and particularly inventory and supply dynamics in what is typically a soft month for sales that is more about seasonal adjustments (9amET).

Solid US data included a big beat by the Empire manufacturing gauge that offers a good start to tracking the path to the next ISM-manufacturing report. Empire jumped 20 points higher to +1.9. We need more evidence from bigger regional manufacturing areas in the other US surveys before getting too excited here. Up next will be industrial output that is expected to be soft (9:15amET), plus UMich consumer sentiment (10amET) that will be watched for signs that gas prices and cooling labour markets may be weakening attitudes alongside a focus upon updated inflation expectations. Also note that import prices were up 0.5% m/m which fans the inflation side of the narrative, while the US terms of trade improved because of a bigger 1.3% m/m jump in export prices partly fed by higher oil prices in August.

NAFTA 2.0 EMBOLDENED THE UAW

Somewhat perversely, the changes to NAFTA that Trump secured give a boost to their wage demands and with material implications for price pressures.

NAFTA 2.0 changed the rules to require 75% N.A. content in order to avoid import duties, up from 62.5% previously. Further changes required that 40% of auto content must be made by workers making US$16 or more per hour which didn't affect Canada or the US but does affect Mexico where wages were much lower. Also recall that at least 70% of metals used had to be bought in N.A.

These were major gifts to the US autoworkers unions and N.A. metals producers. They lessened the ability to move production out of N.A. and also gave the UAW bargaining a boost as Mexican plants had to adapt to higher wages.

What they do to the competitiveness of the N.A. auto industry is another matter. Ditto for consumers. Basically NAFTA 2.0 built a bigger tariff wall around wages and prices and we'll see how that all works out in the end. For now, I think this is part of why the UAW is feeling rather emboldened right now. In the end, Trump got his wall, just not the kind he meant, and you and I will pay for it.

CANADIAN POLICY MEASURES

This link was initially titled “fighting-middle-class” when it was posted yesterday afternoon, versus this morning’s correction. Perhaps they found the mole in the IT group. Here are a few thoughts on the government’s latest action plan for the economy and inflation that was announced yesterday afternoon.

Grocery prices

Grocery CEOs will be summoned to present a plan by October 9th to “stabilize” food prices. If their plan does not meet with the government’s approval, then they will face higher taxes and possibly “other tools” that were not spelled out.

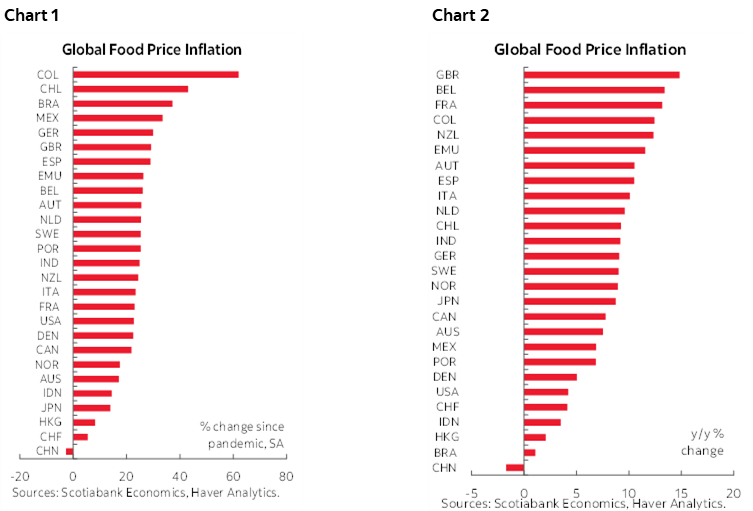

Enter chart 1 that ranks countries according to cumulative food price increases using each nation’s CPI figures since the start of the pandemic, plus chart 2 that does likewise in terms of the latest year-over-year readings. Food prices have gone up a lot everywhere, but Canada is well down the list of this broad set of countries. Little things like, oh, the pandemic, the Ukraine war, the disruptive effects of both developments on global commodity prices and supply chains explain much of this. So does consumer behaviour such as grocery hording early in the pandemic, or not taking full advantage of the choice that exists including what I regularly see to be the packed parking lots at the relatively most expensive grocery stores relative to cheaper alternatives. If competition and choice and thinly veiled government accusations of uncompetitive behaviour are truly worse in Canada than elsewhere, then riddle me this: Why isn’t Canada toward the top of this list?? That’s especially so given protracted weakness in the Canadian dollar’s purchasing power in commodity markets where food prices are typically denominated in USD.

This perspective was entirely absent from the Competition Bureau’s report earlier this year that slammed the industry. Absent from the report that had a high schoolish feel to it was any nod whatsoever to global factors either out of neglect or through political direction.

In my opinion, grocery companies are being summoned to Ottawa to be publicly shamed in an overt tax grab in order to fund even more heavy government spending that has driven some of the inflation Canadians have faced. Interest expense is exploding, heavy prior spending is a burden on deficits for years to come and the government wants to spend even more. That’s what this is really about, but it could come at a cost.

Increased regulatory costs and taxes may deter foreign expansion in Canada and discourage investment in the sector. It may drive further automation against employment. It is likely to lead to other unintended consequences. Maybe package sizes and features will change. Perhaps preferred pricing will go to people who buy memberships that may become more widespread. Don’t want a membership? Well, that’s fine, you’re not wanted as a customer and there is no obligation to serve you. Already have a membership? The price just went up. Perhaps sales of limited quantities will be held outside of convenient hours. And on and on. Enforcement would be a challenge and would be next to impossible to achieve, but the deadweight efficiency losses to the economy would be a concern. The worst case scenario is going back to 1970s price controls with armies of bureaucrats trying to track and monitor individual prices to ensure compliance.

But the bigger point is the ongoing bias against private industry. Today it’s grocery companies and some might think that’s ok in our increasingly divided world that is egged on by divisive, populist, finger-wagging policies. But tomorrow they’re coming for your firm and industry. As a proud capitalist, I’m deeply concerned about the way in which many of my country’s leading industries from energy to financials and now this are being treated. Beating on the successful firms is no industrial policy. It’s also no way to address the country’s mounting economic imbalances.

Competition Policy

Regular readers know that I’m always flashing charts showing Canada’s terrible productivity problem and soaring unit labour costs. Something Ottawa did yesterday may be at odds with what could improve upon this.

The government will remove the so-called ‘efficiencies defence’ in the Competition Act. This is the provision that stipulates that a merger may be allowed to proceed if efficiencies it generates outweigh concern toward potential anti-competitive effects such as prices or choice. I can totally get the need to ensure that competition policy preserves highly competitive markets and fully support that as a professional economist and consumer.

I also get the need for companies to have the flexibility to seek out combinations that help them compete whether against domestic or international firms, or to attract capital or the best talent. Eliminating this defence would have probably resulted in much greater challenges getting past merger proposals approved. It may do so in future. If so, then Canada may have politically tilted the field against merger proposals that would enable them to compete. As flawed as the efficiencies defence may be according to some, what replaces it may be a completely politicized process run according to the whims of Cabinet.

Eliminating GST on Purpose-Built Rentals

This proposal has been the worst kept secret going for quite a while. The Feds will remove the GST on the construction of new apartment buildings for renters (“purpose-built rental accommodations”). It is beseeching provincial governments to do likewise. Such a proposal has been bandied about for a while now and there has been rising sentiment that the government was leaning in this direction.

Policies that increase housing supply in market friendly ways by tearing down barriers are to be welcomed. In determining success of policy actions, timing, order of operations and current circumstances matter enormously.

Caveats to stimulating housing include concerns about being too little too late relative to soaring immigration instead of having opted to reverse the order of actions, plus their application at a time of full employment and tight capacity constraints in the economy and the labour market including the shortage of construction workers.

Incidence effects and unintended consequences will matter enormously here in determining policy success. Will the tax cut truly incentivize building? Is there the even the ability in a tight economy and labour market to build more and soon enough? Will wages, construction costs, prices and margins absorb the tax cut? Those incidence effects will need to be carefully monitored in determining inputs to next steps for monetary policy.

CEBA Loan Repayment Extension

Small businesses that took advantage of the Canada Emergency Business Account program will get another year to repay their loans. The CFIB says that’s not going far enough (here) after warning about the consequences to not extending and forgiving (here).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.