ON DECK FOR THURSDAY, SEPTEMBER 14

KEY POINTS:

- China stimulus props up risk appetite into major developments

- China applies further easing by cutting reserve requirements at banks

- Two reasons why the ECB will probably hike and why they shouldn’t say they’re done

- US retail sales, PPI and claims could photobomb the ECB

- The UAW strike deadline is tonight

- Australia posted a strong jobs recovery but it was all part-timers

Modest movements across multiple assets classes could change very quickly this morning. The simultaneous release of the ECB’s decisions and US data on retail sales, PPI and claims could spark some fireworks at around the same time. We’ll find out as soon as tonight whether UAW workers at Ford, GM and Stellantis will strike which seems likely, given exorbitant wage and COLA demands. Whether the PBOC eases again could be more impactful but thsi morning’s RRR cut may lessen the odds of another rate cut now.

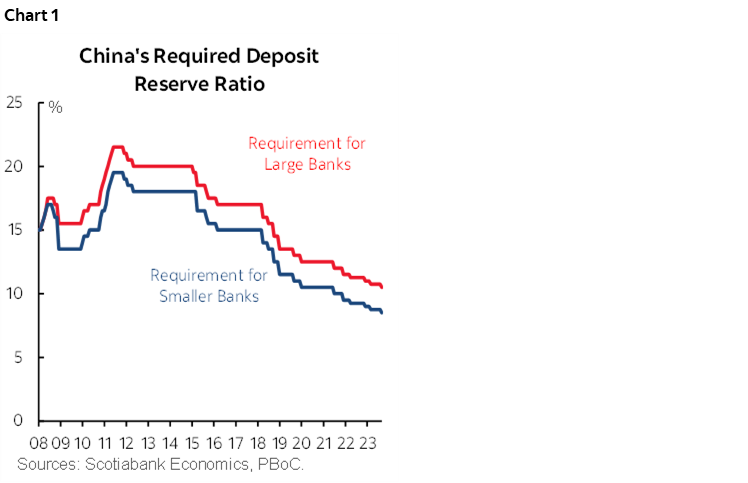

China cut the required reserve ratios for large (10.5% from 10.75%) and small (8.5% from 8.75%) banks while keeping rural banks unchanged at 5% (chart 1). This is a further step toward applying stimulus and it’s consistent with my narrative for some time now that sentiment toward China has been too bearish relative to what has been priced in measures such as depressed equity P/Es to the yuan. The move had been somewhat telegraphed by a Chinese newspaper before China released credit figures earlier this week when the paper correctly guided that credit figures would surprise higher and that further reductions in the required reserve ratios were coming.

Australian jobs sharply rebounded in August, but the details were soft. 65k jobs were created which smashed consensus expectations for 25k and the prior month’s 14.6k drop was revised away to being flat (-1.4k). All the jobs that were created were part-time in both months which doesn’t translate into as much of an effect on hours and pay as full-time positions. Australia’s curve was dearer across maturities partly due to the weakness under the hood.

On tap into this morning will be the following developments:

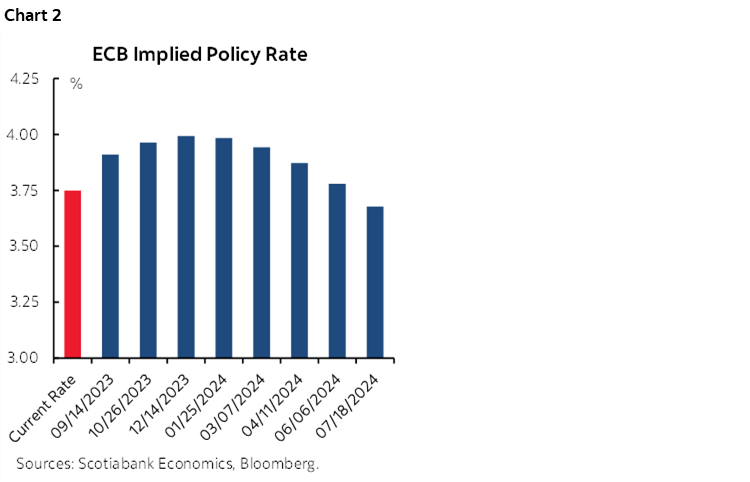

1. A slim 34–32 majority in Bloomberg’s consensus thinks that the deposit rate will stay at 3.75%. I would expect a hike and cautious data dependent guidance from Lagarde in her presser. That consensus may be stale in light of yesterday morning’s anonymous guidance that the forecast for 2024 inflation may be raised higher than June’s 3% forecast. Around two-thirds of a 25bps hike is priced for today (chart 2). To not hike would risk the unusual signal that financial conditions could ease despite ongoing pressures particularly in terms of second-round wage-price effects. Furthermore, second-round wage pressures on inflation in a region where collective bargaining decisions drive lagging and arguably bigger effects for longer than the US labour market that clears supply and demand somewhat more readily. As for the bias, I would think they shouldn’t deliver a clear bias that they are done hiking versus being data dependent and keeping the door open to more. If they signal they are clearly done then markets being markets will pounce and take it as a clearer signal to buy the front-end. That may be very premature.

2. US retail sales are expected to be soft given what we know about how lower auto sales and higher gasoline prices cancel each other out. Core sales may also face downside risk after the prior month’s large 1% jump. It’s a nominal print, so one upside could be yesterday’s 0.6% jump in CPI and 0.3% core rise and so watch lagging volume measures that strip out price effects.

3. US producer prices risk adding to yesterday’s mild upside surprise to core inflation. Headline PPI is expected to rise on higher commodity pressures, but core producer prices are expected to be up by a fairly mild 0.2% m/m.

4. Will last week’s US weekly initial jobless claims reverse or build upon the prior week’s pre-holiday effect? California was estimated two weeks ago and so were some others, and the Friday into a long weekend may have seen folks delaying applications.

5. Canada only updates wholesale sales for July, but it should add to rebound evidence that may build into Friday when manufacturing sales and existing home sales get updated. I was left feeling duped by all this build-up to a big housing announcement by Ottawa yesterday afternoon only to find it was a total non-event and photo-op. The Feds have been serially overstimulating housing demand with fiscal measures, rates of immigration that the economy cannot handle and aided by the BoC’s too-low-for-too-long bias through the pandemic and in prior years such as former Governor Poloz’s inappropriate easing in early 2015. Now they’re pivoting toward blaming municipalities which is partly correct but also rather rich. It’s going to be impossible to bring to market enough supply in a short enough period of time to meet the surging housing demand when the country is taking on new arrivals at a pace of about 100k per month as per the latest figures for population growth.

6. Tonight’s after-market brings out decisions by the PBOC (9:20pmET) and Peru’s central bank (7pmET). Midnight is the UAW strike deadline but whether they announce at that time or soon afterward is unclear.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.