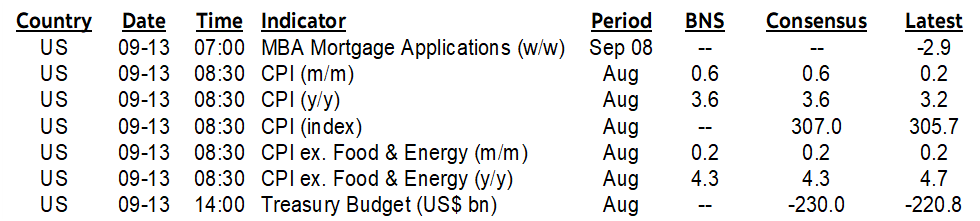

ON DECK FOR WEDNESDAY, SEPTEMBER 13

KEY POINTS:

- Risk-off sentiment ahead of US CPI

- US core CPI expected to be soft…

- …but does it matter if not?

- Japanese PMI Kishida flags coming fiscal supports…

- …that may add to the case for ending the BoJ’s negative rates

- UK data disappoints again

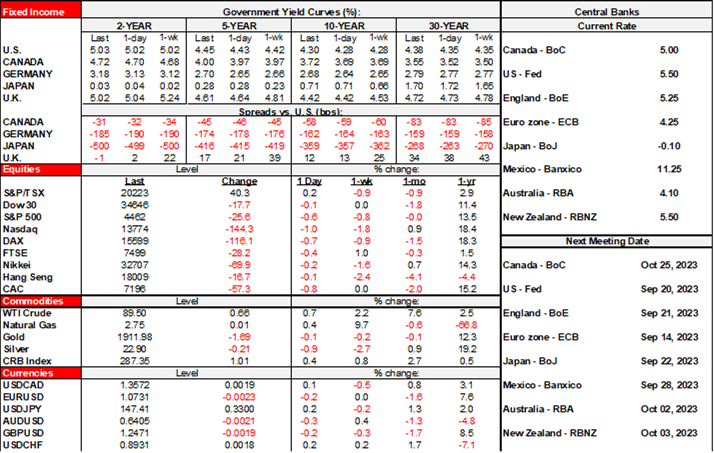

Global markets are treading somewhat carefully ahead of US CPI. Gilts are outperforming following weaker than expected UK releases. Oil keeps gaining.

Comments by Japan’s PM Kishida are worth paying attention to. His remarks reinforce the view that the global tango that has governments taking one stimulus step forward while central banks take one tightening step backward continues unabated. Kishida said his government will introduce policies on higher pay in October that will seek to have wage gains outpace inflation while offering higher gas subsidies in a larger package of fiscal measures. The comments hit after Tokyo markets shut. At the margin, however, they add to sentiment that the end of negative rates at the BoJ lies within reach. OIS markets are pricing a zero rate by December and then a move from -0.1% to a target rate of about 20bps by next summer.

This is a further negative for global bond markets. There are few forms of policy advice that have proven to be more disastrous than the advice offered by some to governments to lock and load with increased long-term spending on the view that bond yields couldn’t possibly go up much. That advice was especially influential in my home country of Canada and the fact it has been dead wrong is contributing to rising long-term structural deficits.

UK GDP fell by -0.5% m/m in July (-0.2% consensus). Services disappointed as the monthly index fell by -0.5% m/m (-0.1% consensus). Industrial output landed on the screws at -0.7% m/m. Construction output also fell by -0.5% and on expectations.

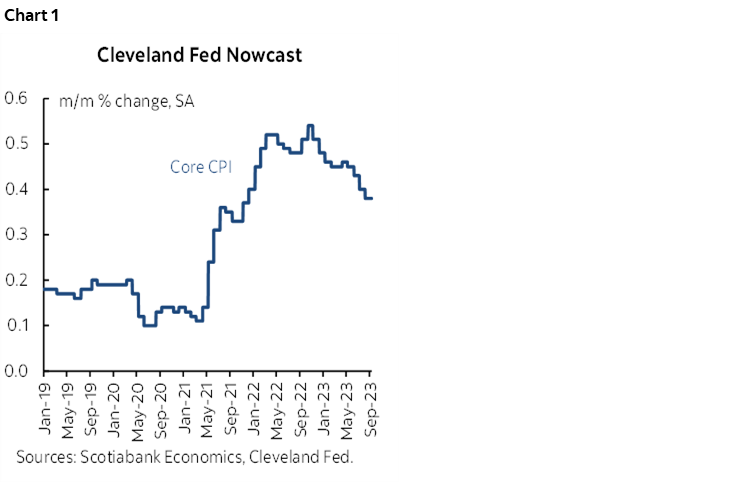

Most of the focus will be upon US core CPI. Most—including Scotia—expect a gain of 0.2% m/m SA. A minority expect 0.3 and one or two are at 0.1. The Cleveland Fed’s ‘nowcast’ is tracking 0.4% but has overestimated core CPI for a while now.

Gasoline will be the big driver of the large, expected jump in headline CPI as the all-grades gasoline price composite hits the year’s highs. Shelter is likely to remain disinflationary at the margin as we’re trending off peak gains in OER and rent of primary residence in lagging response to prior softening of market rent gauges. Vehicle prices should have little effect but there is always risk in how the BLS captures known information through partial samples and adjustments. Core services ex-housing prices are expected to remain subdued compared to the peak rates of increase earlier in the pandemic period.

As argued in my week ahead (here), I don’t think the release will be enough to sway the FOMC away from a pause next week. The trends in core inflation and jobs plus rising downside risk to GDP growth after Q3 could drive a cautious approach. Toss in the risks of a UAW strike announcement as soon as tomorrow and a US government shutdown into October plus student loan payments shock and our best guess at Q4 GDP growth is tracking about 0% growth to err on the side of caution. After that we’ll see, since some of these shocks could reverse into early 2024 and therefore complicate the Fed’s ability to read the tea leaves.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.