ON DECK FOR FRIDAY, OCTOBER 6

KEY POINTS:

- Bond yields position for a solid payrolls report, vulnerable to a disappointment

- Did Biden hint at what to expect for nonfarm payrolls?

- US payrolls expected to post a decent gain

- Low conviction on Canadian jobs…

- …but repeating stellar wage gains might be tougher this time

- Fed’s Daly apparently never heard of the chicken and egg

- German factories’ order books post a partial rebound

- RBI delivers hawkish hold and sells bonds

- Peru’s central bank cuts as expected

Welcome to the day everyone’s been waiting for and that might not have happened if the US government had shut. Well, maybe not everyone, but probably many people who would be reading a note like this one. It’s payrolls day, with a side order of Canadian jobs, eh. Bonds are positioning in mildly hawkish fashion for the numbers as yields are gently higher across the US, Canada and Europe. The USD is little changed so far. Stocks are gently higher across N.A. futures and European cash perhaps on the assumption that a solid payrolls report would indicate ongoing resilience but aided by some M&A announcements. Ahead of long weekends in both the US and Canada, Canadian fixed income will shut at 1pmET but there is no early close in the US, or at least not technically with the Hamptons calling out to New Yorkers.

So why are bonds positioning in this way? Perhaps it’s the President Biden effect. Late yesterday it was announced that he will issue remarks on the job market at 11:30amET. The Chair of the Council of Economic Advisers gets the jobs numbers the afternoon before and hence so does the President. Who knows, but I think it’s probably more likely he’s going to be speaking about jobs in order to gloat about a solid report rather than to address weakness under his watch into an election year.

There are a few things to get out of the way before turning to jobs previews in both countries.

For one, San Fran Fed President Daly’s remark yesterday that tighter financial conditions suggest less of a need for rate hikes falls into the chicken-and-egg trap that we all learned about as youngsters. Tighter financial conditions are in part because the FOMC told markets they planned on hiking again and staying higher for longer than previously guided. Renege on one or both of those two forms of guidance, and financial conditions would probably ease. Central bankers (almost) never get this. It should be mandatory for them to have basic street training out of academia and their central bank fortresses.

German factory orders rebounded a bit in August. The 3.9% m/m rise that month looks good, until one recalls that the prior month plunged by 11% m/m.

Peru’s central bank cut its reference rate by 25bps to 7.25% as widely expected and said that the reduction does not necessarily indicate they are planning a straight line reduction on a meeting-by-meeting basis. That’s what they said the last time before cutting back-to-back, although in fairness one could justify this latest reduction by pointing to weaker than expected CPI and a drop in a key economic activity index.

The Reserve Bank of India held its repurchase rate at 6.5% as generally expected while repeating a hawkish bias by saying it is still in accommodation withdrawal mode. India’s yield curve bear steepened with double digit increases in yields from 5s through 10s as the RBI said it may sell bonds in order to mop of what it views to be excess liquidity. Governor Shaktikanta Das said “The timing and quantum of such operations will depend on the evolving liquidity conditions.”

Now onto US and Canadian jobs, with fuller previews available in the Global Week Ahead here.

US PAYROLLS PREVIEW

Most estimates for nonfarm payrolls (8:30amET) are within about 140k to 200k with a slight skewness toward the right tail above 200k.

How strike effects play into it remains an uncertainty, although recall that the UAW strike began on September 15th with only a few workers affected at first at the tail end of the household survey’s reference week and into the nonfarm payrolls pay period that includes the 12th day of each month. The BLS indicated that there were only 17,700 striking workers in September (here). ADP was a negative surprise but offers poor tracking ability.

Everything else indicates strength, such as claims between nonfarm reference periods, NFIB hiring and hard to fill, JOLTS, consumer confidence ‘jobs plentiful,’ Challenger layoffs, ISM-employment subindices etc. That’s all just fine and dandy, except those advance readings offer very loose guides at best and revision risk is often a wildcard that could impact the jumping off point for the September print itself. Given a +/-120k 90% confidence interval, you’d have to be down toward zero or up above 300k+ to be offering something other than statistical noise, notwithstanding the fact that markets tend to interpret the number much more literally.

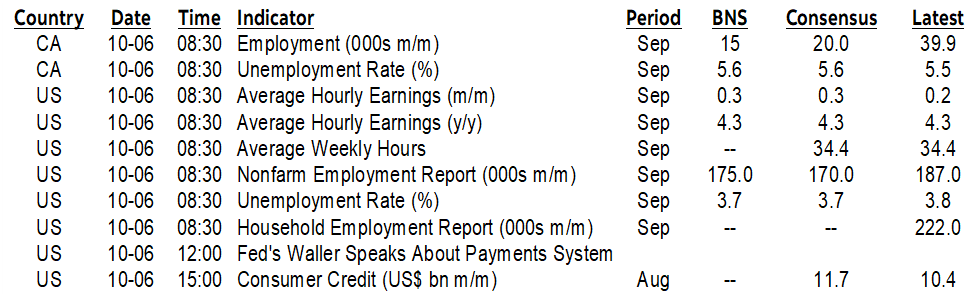

The Fed is hoping for further progress down and to the right along the Beveridge Curve (chart 1) but may not get it this time. JOLTS vacancies surprised higher earlier this week and we’ll see what happened to jobs in a moment.

Wages may dominate payrolls. After a pair of 0.4% m/m SA gains in June and July that positioned wage growth at a 5%+ m/m SAAR pace, August saw wage growth cool to 2.9% m/m SAAR. Markets will be sensitive to any hint of a new trend settling in, or whether that was an aberration on a stronger trend.

CANADIAN JOBS PREVIEW

Plug your nose toward the expanding number of taxpayer-funded bureaucratic socialists running Canada’s farcical industrial policy after their latest populist assault on grocers and move onto Canadian jobs. Canada updates jobs, wages and other statistics within the Labour Force Survey for September at 8:30amET. Its market effects will compete with US payrolls.

Everyone expects a rise. Uh oh. Most estimates are in a roughly 0–30k m/m band. I went with 15k, loosely justified around still high vacancies and immigration as the economy rebounds somewhat from summertime shocks. That’s not with much conviction given how wonky the earlier month was. Recall there was a big apparent loss of education sector jobs, but that was due to difficulty Statcan is having with SA factors given the changed timing of education sector contracts for the school year now versus history. That drop was offset by an equally tough to believe large gain in self-employment that is always among the softest of soft data.

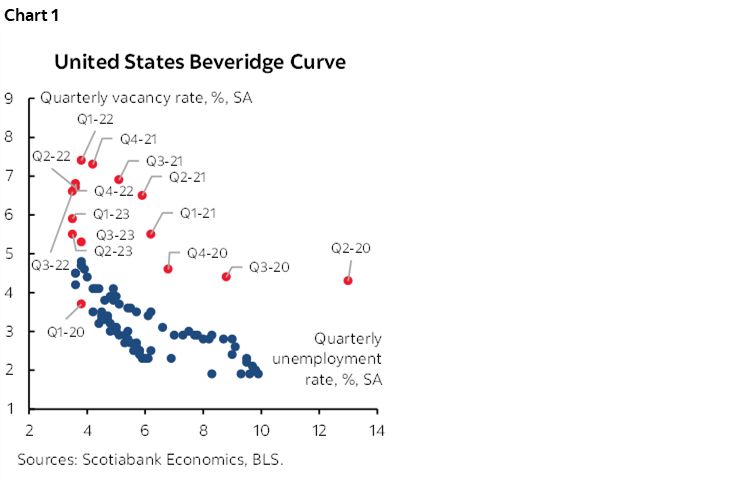

Where Canada may be more vulnerable is on wage growth, but just this once. Promise. Sort of. We’ve had back-to-back 10%+ m/m SAAR wage gains that will be tough to repeat (chart 2). I said the same thing after the first time that it happened, but another whopper was registered and so who knows. It’s key to look at the smoothed m/m SAAR trend anyway and that’s likely to remain very hot. Wage settlements come out next week in the unionized sector that covers about one-in-three Canadian workers. It's also key to look at wages relative to sinking labour productivity and not just in isolation of one another.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.