ON DECK FOR MONDAY, OCTOBER 30

KEY POINTS:

- A fresh trading week starts with US-European yield divergence…

- …as US Treasuries await step 1 of the week’s debt announcements…

- …and EGBs digest softer than expected inflation updates

- The shock potential of this week’s US debt news may not be as large this time

- BoC’s Macklem has a chance to clarify his remarks today

- Global Week Ahead reminder

As a reminder, please see the Global Week Ahead—The QT and Refunding Tango here. The full publication is in clients’ inboxes along with the summary slide deck. Key topics on tap this week will include:

- Treasury’s debt sales plan may be taken more in stride this week

- FOMC is expected to stay on hold amid upside risks to inflation

- US productivity to offset higher labour costs

- BoJ watchers on guard for policy tweaks

- BoE expected to hold as the macro environment sours

- Will US nonfarm payrolls repeat the prior big gain?

- BoC’s Macklem gets another chance. Two in fact.

- Canada’s economy is plodding along despite shocks aplenty

- Will acute Canadian wage pressures abate?

- Norges Bank expected to pause

- BanRep expect to extend its hold

- Brazil’s central bank likely to cut again

- Bank Negara playing defence on ringgit weakness

- China’s PMIs to inform Q4 growth momentum

- Eurozone CPI expected to continue easing

- GDP: Eurozone, Canada, Mexico, Peru, Sweden,

- CPI: Peru, SK, Indonesia, Switzerland

- Heavy earnings calendar

- Other Global Macro

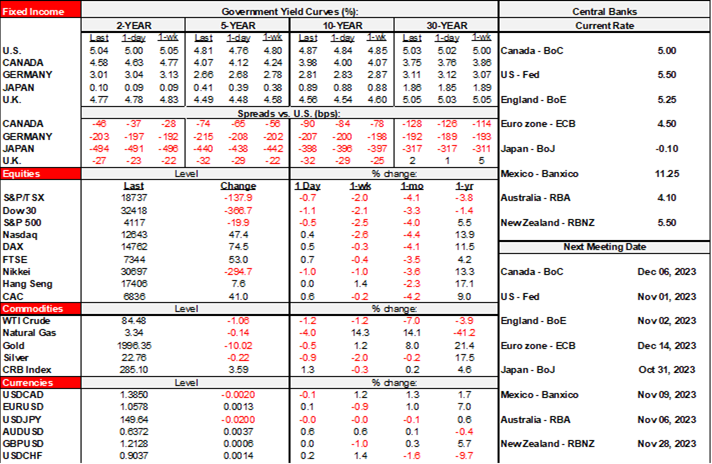

Yield divergence between N.A. and Europe is a defining feature of the start to a fresh trading week.

Treasuries are cheapening by a few basis points perhaps partly out of fear toward what this afternoon’s debt estimates may reveal. European yields are comparatively outperforming by modest margins as further evidence of softer than expected CPI is taken down after Friday’s limited evidence from one German state. Equities are mildly higher by about ½% to 1% across N.A. futures and European cash markets. Oil is down by over a buck across the main benchmarks as yet again the weekend came and went without feared major escalation in the Middle East.

The US Treasury announces Q4 marketable borrowing estimates today at 3pmET. It’s round one of the two-step process to determine whether bonds face a repeat of what happened starting on July 31st and August 2nd. On Wednesday at 8:30amET, Treasury will then announce the Q4 Quarterly Refunding Statement that lays out the size and frequency of auctions. As noted in Friday’s Global Week Ahead and accompanied by further details, the debt issuance plans of the US government could well steal the show from Chair Powell and the FOMC this week, although the shock potential is probably much lower now after markets have digested the higher issuance numbers and the accompanying forward guidance to expect more in future quarters. Furthermore, recall that the last time around also dealt with the BoJ surprise a few days earlier on July 27th and we’ll see if another surprise lurks this time or not when the BoJ announces tomorrow.

Shortly after today’s Treasury announcement, BoC Governor Macklem and SDG Rogers deliver round 1 of their parliamentary committee testimony before the House of Commons Standing Committee on Finance. It starts with an opening statement that will be available at 3:30pmET and then goes into Q&A. He may clarify somewhat mixed remarks last week that started with a hawkish hold on Wednesday and then gave way to more dovish remarks in a radio interview the next day, although the context was likely important.

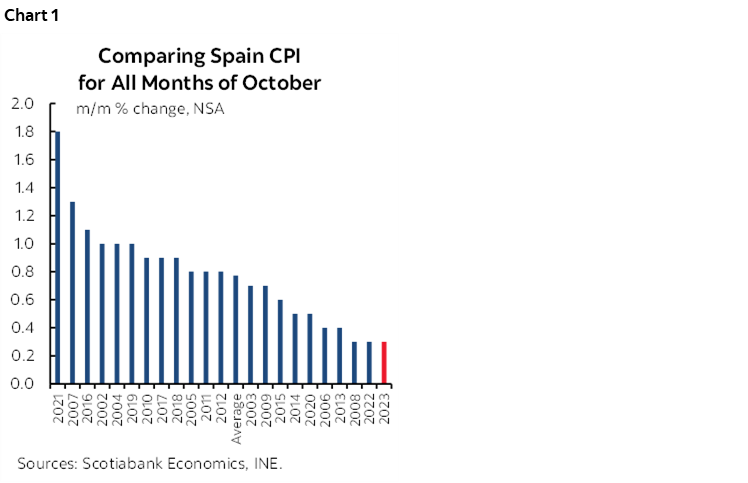

Germany and Spain kicked off tracking of Eurozone CPI on a dovish note this morning. More individual German states released estimates for October CPI and they are tracking beneath consensus estimates for the national add-up that we get a little later this morning (9amET). The individual states revealed estimates of between -0.1% to 0% m/m. Spain also released CPI that landed at 0.3% m/m (0.5% consensus) with core also weaker than expected; the headline rise in Spain was among the weakest seasonally unadjusted gains for like months of October on record (chart 1). The eurozone totals along with France and Italy arrive tomorrow.

German GDP was a touch stronger than expected including on revisions. Q3 contracted by -0.1% q/q SA nonannualized (-0.2% consensus) and the prior quarter was revised up a tick to 0.1%.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.