ON DECK FOR TUESDAY, OCTOBER 3

KEY POINTS:

- Minor moves across global asset classes...

- ...except Canadian rates post-holiday and a BoC warning

- Former BoC official warns on rate hikes if core inflation remains high

- US job vacancies still falling?

- US vehicle sales expected to rise

- RBA extends hawkish hold as expected

- ISM-manufacturing recap

- Order books are improving in the US

- China, SK shut for Golden Week

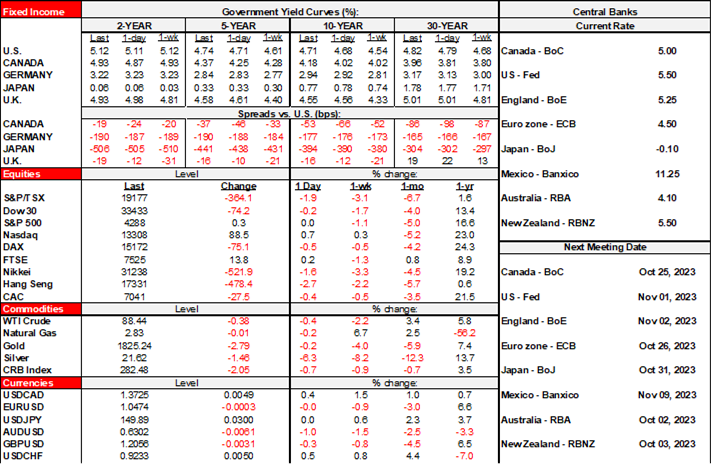

Global markets are characterized by relatively minor moves absent major catalysts. Canada is returning from holiday and catch-up to yesterday’s global moves is driving underperformance in rates alongside the effects of comments by a former BoC official (see below). Canadian 2s are up 6bps with 10s up 16bps. US Treasuries and EGBs are mildly steeper as gilts outperform a touch. The USD is flat as the stability of the euro, yen and MXN offset some softness across CAD, the A$/NZ$ and a few others. Stoccks are little changed as tiny gains in London and the US are mixed in with slight declines across the rest of Europe and Canada. Canada is returning from holiday today. Markets are shut in China and South Korea for Golden Week. Recall that all US data releases this week will proceed as planned given the surprise deal to avoid an imminent US government shutdown over the weekend.

First, I’ll recap a couple of yesterday’s developments since it was a Canadian holiday.

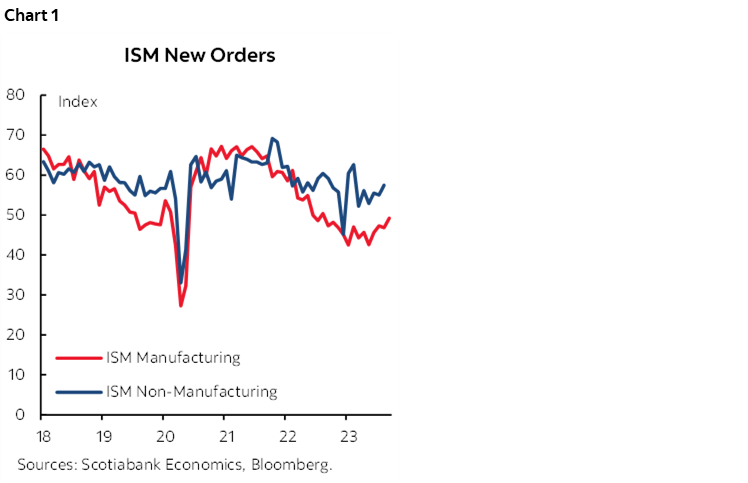

US ISM-manufacturing surprised higher yesterday and barely remained in contraction territory in September’s reading. The 49 print (47.6 prior, 47.9 consensus) inched closer to the key 50 dividing line between expansion and contraction. Prices paid ebbed by 3.6 points to 43.8 and hence further into falling territory as reported declines in items like steel and aluminum offset increases in energy prices. Perhaps some of the metals softness may be related to the auto strike. Employment increased into expansion territory (51.2, 48.5 prior). New orders improved but are still slightly contracting (49.2, 46.8 prior). New orders have been gently improving over recent months both for services and manufacturing (chart 1).

Former BoC Deputy Governor Beaudry remarked yesterday that if core measures of inflation “don’t come down, that really brings a danger that maybe there is a point where the Bank of Canada will need to tighten more.” He also warned that further downside to house prices may lie ahead given where fixed rates have risen. He did not comment on immigration.

The RBA extended its cash rate target hold at 4.1% as widely expected while retaining a data dependent tightening bias.

Here are today’s developments:

- BoC part-time external non-executive Deputy Governor Nicolas Vincent, an academic, will speak on “pricing practices and monetary policy”. Speech at 8:25amET, audience Q&A but no press conference. It’s his first speech since his appointment in January.

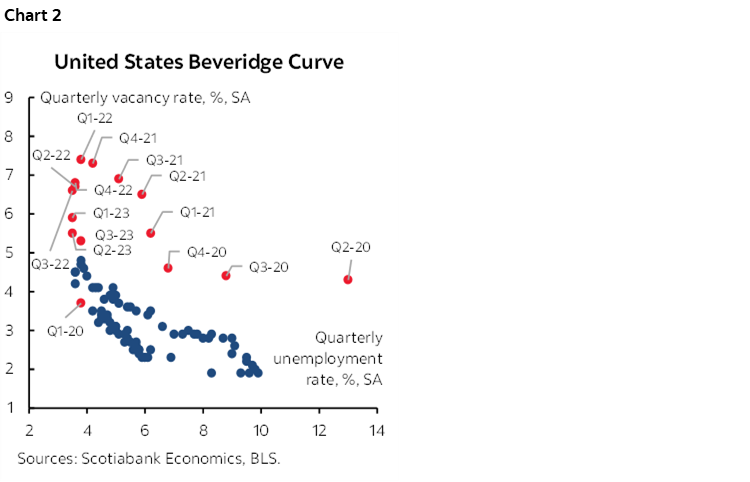

- The US will update JOLTS job vacancies for August this morning (10amET). They are still elevated at 8.83 million, well off the 12 million peak in March of last year, but still above the roughly 7 million pattern just before the pandemic and 4.5 million longer-run average before the pandemic. Chart 2 shows the Beveridge Curve that depicts marginal improvement in excess demand conditions in labour markets primarily through lower vacancies as the unemployment rate remains low.

- The US will also release vehicle sales for September later today. A modest rise of about 2% m/m SA is expected to 15.4 million based on industry guidance.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.