ON DECK FOR THURSDAY, NOVEMBER 30

KEY POINTS:

- Yields up as month-end consolidates bond gains

- Oil is up on OPEC+ cut speculation that may fan renewed inflation risk

- Canadian GDP is likely to be a weak set of figures…

- …but there’s a high bar set against recession hype

- Fed’s preferred inflation gauge could be weaker than CPI

- Eurozone CPI confirmed as softer than estimated..

- …as a weak core CPI trend takes root

- China’s state PMIs continue to signal little momentum

- Canada’s mixed bank earnings season

- Chile’s economy performed a little better than expected

- India’s economy also performed better than forecast

- Bank of Korea stays on hold as widely expected

- Japanese consumer spending soft, industrial output beat

Month-end brings with it a panoply of key developments from whether OPEC+ will agree to deeper production cuts to top shelf global macro releases and a wave of Canadian bank earnings.

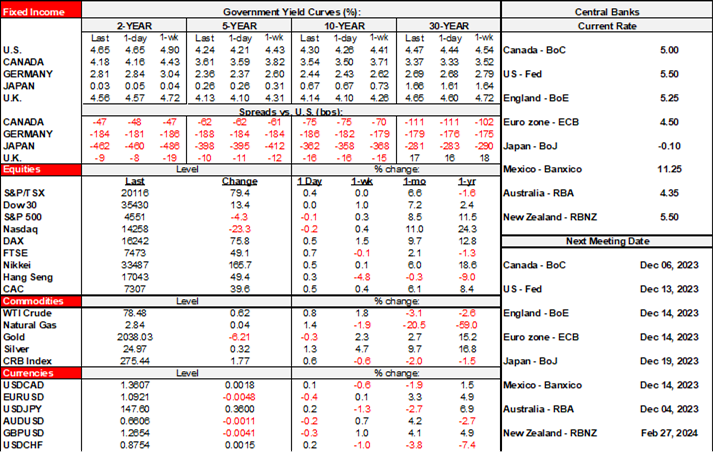

Sovereign yields are mostly pushing gently higher particularly across longer maturities. US 10s rallied big this month from 4.93% to about 4.30% now and so perhaps month-end rebalancing is taking some gains here. Equities are slightly bid across N.A. futures and European cash. The USD is a touch dearer on a DXY basis. Oil is up again on OPEC+ speculation (see below).

Let's get the generally dovish overnight stuff out of the way first before what matters into the North American session by way of Canadian and US macro risk.

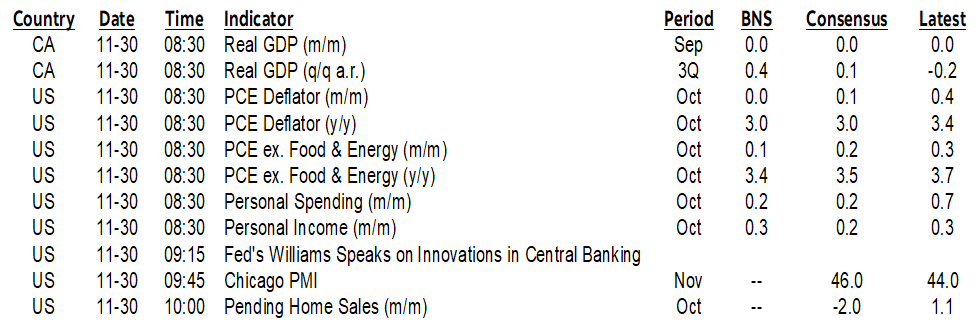

China’s state PMIs were fairly stable (chart 1). The November composite PMI landed at 50.4 (50.7 prior) as the non-manufacturing PMI slipped a touch to 50.2 from 50.6 and the manufacturing PMI was little changed at 494 (49.5 prior). The economy remains on a knife’s edge between contraction and expansion and marginally tilted toward the latter.

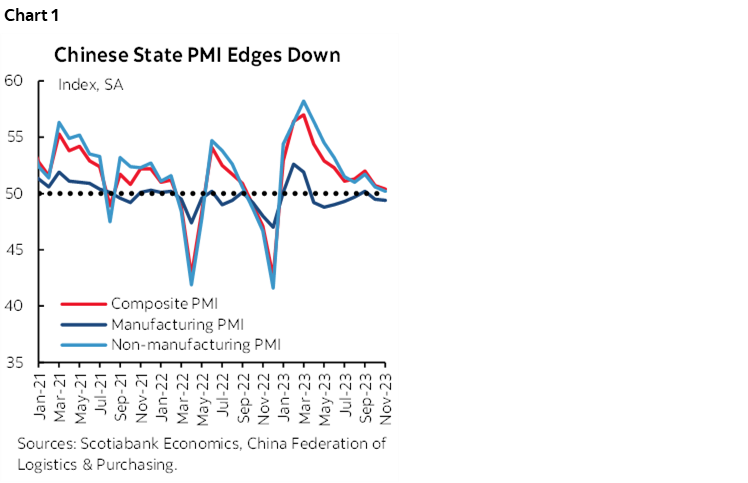

Eurozone CPI landed softer than expected at -0.5% m/m (-0.2% consensus) and 2.4% y/y (2.7% consensus). Core also weakened by more than expected at 3.6% y/y (3.9% consensus). That was because the month-over-month core reading was another soft one, extending the streak to three consecutive months of below-average monthly core inflation readings (charts 2–4). Most of the fixed income shock was probably priced in after yesterday's German and Spanish figures that were reinforced by softer than expected readings from France and Italy this morning.

Japanese macro data was mixed. Retail sales unexpectedly fell by 1.6% m/m (+0.4% consensus) in October and only a part of that was explained by an upward revision to +0.4% m/m (from -0.1% m/m). Industrial output climbed 1% m/m (0.8% consensus).

The Bank of Korea left its base rate unchanged at 3.5% as widely expected. What mattered more to markets was weak data as industrial production fell 3.5% m/m SA in October (+0.4% consensus).

Chilean macro indicators were better than expected. Industrial output was up 1.1% y/y (0.7% consensus) led by manufacturing (+9.5% y/y, 2.6% consensus). Copper production increased. Retail sales fell by less than feared (-6.9% y/y, -8.7% consensus) but are still weak.

India’s economy grew faster than expected and avoided a material slowdown that was expected. GDP was up 7.6% y/y (6.8% consensus) with the prior quarter left at 7.8%.

Here are the top things to focus upon in into the N.A. open in chronological order and see the Global Week Ahead for further elaborations.

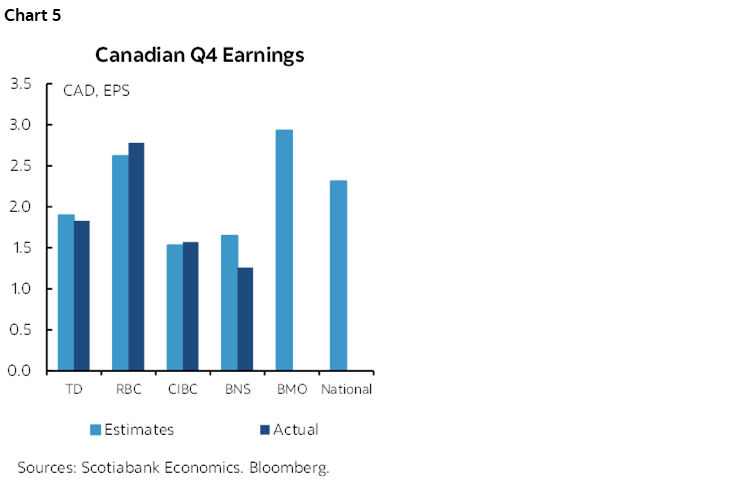

1. Canadian bank earnings. BMO will be the tie breaker tomorrow among the ‘big five’ banks (chart 5). RBC reported adjusted EPS of C$2.78 ($2.62 consensus). CIBC reported adjusted EPS of $1.57 ($1.53 consensus). TD whiffed by posting adjusted EPS of $1.832 ($1.9 consensus) but beating on revenues.

2. OPEC+ ministerial meeting: speculation is rampant toward deeper production cuts of 1 million bpd being delivered. That's helping to buoy oil prices this morning. The decision is expected some time after 9:30amET.

3. Canadian GDP (8:30amET): scroll back to comments shared here yesterday afternoon and in the week ahead. Weak, but not a recession even if we get back to back GDP dips.

4. US core PCE (8:30amET): I went a little lower than consensus (+0.2%) at +0.1% m/m because of PCE’s lower weight on shelter than CPI after shelter came in strong last month. An uncertainty is how yesterday morning’s downward revision affects the math since we don’t know the monthly composition of the downtick to the Q3 estimate. Also watch US jobless claims (8:30amET) as well as mild expected gains in personal incomes and spending (8:30amET) and then pending home sales (10amET).

CANADIAN GDP COMMENT

Canadian GDP could offer sticker shock to markets (8:30amET). While not expecting one, I can’t rule out the optics of a technical recession, even if calling it as such is probably nonsense. The economy shrank by a paltry 0.2% q/q SAAR in Q2. Most economists are between 0% and ½% q/q SAAR for Q3 except for a couple of shops that are not brave enough to slap a name on the estimates. My guesstimate was 0.4%.

If we get back-to-back contractions, then I think some of the hot/flighty money is going to pile into the front-end, kind of like what we saw with Sweden’s GDP figures yesterday morning. Buy first, ask questions later.

Using the monthly GDP accounts to date and Statcan’s preliminary guidance for September, we can convert the figures to tracking 0% q/q SAAR growth in Q3. This approach uses GDP on a production/income basis.

Quarterly accounts estimate growth on an expenditure basis which means, among other things, that they consider how higher/lower output was achieved including through inventory swings and net exports.

A downside to Q3 GDP on this basis is tracking for a negative inventory draw down although the data is incomplete. At least some of that inventory draw down may be offset by less of an import leakage effect which is a plus to GDP in an accounting sense.

But the questions are numerous. Is it a recession if we lost the most hours worked in Q3 due to strikes since the very start of the pandemic that was due to restrictions that shut the economy? I don’t think so, yet folks on picket lines are not making goods and services which means GDP suffers. Many sectors saw strikes over Q2 and Q3 including port workers, civil servants, airline pilots, auto workers, education sector employees, even Montreal cemetery workers! This lost output has nothing to do with rate hikes and if anything is a price paid by not hiking earlier to prevent some of the inflation that sent workers out on picket lines.

Is it a recession if half the country is literally on fire? I don’t think so, but the wildfires can’t be ignored. They disrupted many key sectors including mining, petrochemicals, forestry, agriculture, and travel and tourism. Sorry BoC, can’t claim that rate hikes sparked wildfires.

Is it a recession if inventories drag on growth for back-to-back quarters? That depends upon why. If companies are positioning themselves for a weak spot by running down inventories and with strikes not helping (eg autos), then it’s disinvestment that curtails some of the risks later. It’s acting prudently. Inventories knocked 0.85ppts off of q/q SAAR growth in Q2 and could well play a similar role in tomorrow’s Q3 numbers.

On this latter point, that’s one reason why we should turn to Final Domestic Demand and not just GDP. It nets out net exports and inventories and looks at just C+I+G with I including business and housing investment in an accounting sense to get a better gauge of the domestic economy’s performance. FDD was up 1% q/q SAAR in Q2. We’ll see what Q3 brings, but a genuine recession in my books would require FDD to contract and for reasons beyond the distortions cited above.

Whatever happens, there is one thing Canadians can celebrate, sort of. Despite cost pressures, you could have it a lot worse. Toronto (and other Canadian cities) are relatively cheap places to live (here). I guess if you want a cheaper city to live in then be my guest and give Lagos, Nairobi or Tashkent a whirl! Good times await you, no doubt…

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.