ON DECK FOR FRIDAY, NOVEMBER 3

KEY POINTS:

- Markets await US, Canadian jobs reports

- Nonfarm payrolls preview

- Canadian jobs preview

- US ISM-services to follow jobs numbers

The week is ending with a nearly exclusive focus upon what may be revealed by job market updates out of the US and Canada this morning. On both counts, the long-established pattern is to expect the unexpected.

The US offers a rich array of job market indicators in advance of payrolls that—hubris within the forecasting community aside—don’t really help in forecasting payrolls. Perhaps Canada’s approach, which is to have little to nothing to offer as a guide to what to expect because of the paucity of other timely gauges, isn’t so much of a handicap after all. In both cases, the statistical noise factor points to ginormous confidence bands around the estimates which makes nailing the numbers largely futile.

This is more about the clean-up and assessing the consequences for the Fed, the BoC, and the broader macro context in the aftermath. In both cases, the numbers are one of two sets that will be available before the next FOMC meeting on December 13th and the next BoC decision on December 6th.

NONFARM PAYROLLS PREVIEW

Nonfarm payrolls, wages and the usual host of other monthly labour market readings arrive at 8:30amET. Here is a brief preview.

- Consensus m/m change median: +180k

- Consensus m/m change mean: 176.6k (so no skewness)

- Range: Most are within 125k to +235k

- Scotia: +200k

- Whisper number: +201k

- 90% confidence interval: +/- 130k. Most estimates fall within statistical noise.

- Std Dev: 31.7k

- Unemployment rate: 3.8% unchanged

- Wages: 0.3% m/m SA nonannualized

- Drivers:

- Most advance readings on the US labour market have performed well but nonfarm doesn’t necessarily follow them. They serve as a rough guide to broad labour market conditions.

- We’re coming off the strongest job gain since January with most assuming we’ll mean revert lower.

- Then again, nonfarm gains have exceeded consensus estimates eight times this year.

- The productivity surge did more of the heavy lifting this time in Q3 which might make for less urgency to continue hiring at a rapid clip.

- Consumer confidence ‘jobs plentiful’ ticked higher.

- Weekly jobless claims were slightly lower between the Sept and Oct nonfarm reference periods.

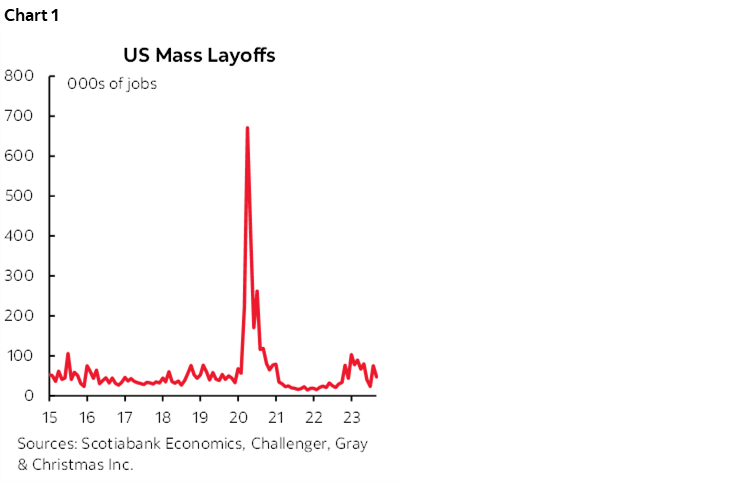

- Challenger jobs cuts inched a bit lower to 46k (chart 1).

- NFIB small business hiring plans inched up a tick. Jobs ‘hard to fill’ also moved up to a four month high.

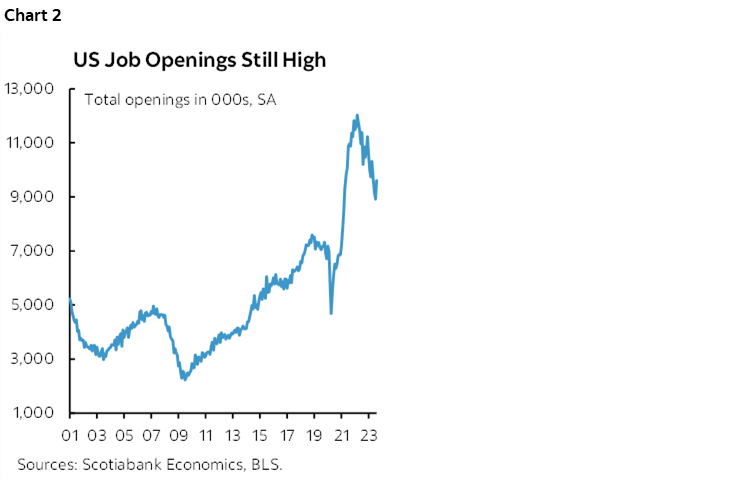

- JOLTS job openings moved higher to 9.55 million in Sept from 9.5 (chart 2).

- ADP was softish at 113k, but also was the prior month (89k) when nonfarm ripped. Poor gauge.

- ISM-mfrg-employment fell by about 4 ½ points into contraction. Small share of total employment.

- ISM-services-employment won’t arrive until after nonfarm today (10amET).

CANADIAN JOBS PREVIEW

Canadian jobs, wages and the usual host of other monthly labour market readings arrive at 8:30amET. Here is a brief preview.

- Consensus m/m change median: 25k

- Consensus m/m change mean: 26.6k (no skewness)

- Range: +10k to +35k

- Scotia: +15k

- Whisper number: n/a

- 95% confidence interval: +/-57k

- Std Dev: 16.2k

- Wages: 5.2% y/y thin consensus

- Drivers: The prior month’s 64k gain was mostly driven by the education sector, self employed and part-time jobs. Both of those sector contributors were wonky. The education sector is having seasonal adjustment issues are the varying timing of teacher contracts now versus the past and so the drop in August righted itself in September. Self-employed can be valued jobs, but it’s the softest of the soft data.

- Unless other categories shake off their dull performance and rebound, then there is downside risk today as these two sectors will probably mean revert.

- Job vacancies are still somewhat above pre-pandemic levels and skewed to sectors like accommodation and food services. They might benefit as the holiday season approaches but probably not yet.

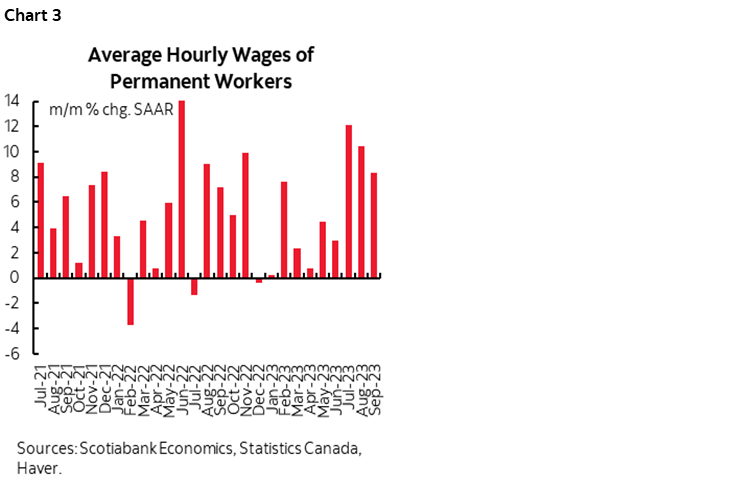

- What could matter more is wage growth. We’ve been seeing three consecutive months of wage gains for permanent employees on the order of about 10% m/m SAAR each time (chart 3). This is backed up by the lagging wage settlements figures that are explosive.

- Soaring wages are happening while productivity tumbles. Unlike the US where recent increases in employment costs have been paid for by productivity, that’s not true in Canada at all. Hence one of the BoC’s concerns in marked different to the Fed.

- Whatever happens to wages, it’s the trend that matters.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.