ON DECK FOR WEDNESDAY, NOVEMBER 29

KEY POINTS:

- Markets rally on weaker Eurozone, AU inflation

- German, Spanish inflation was weaker than expected especially on core

- Australian inflation was also weaker than expected

- Kiwi dollar outperforms on hawkish sounding RBNZ…

- …that flagged immigration as part of a tightening bias

- OECD updates lagging global projections

- US Q3 GDP, core PCE revisions on tap

- US mortgage purchase applications are still on a tear

- Sweden’s krona weakens after GDP disappoints

- BoT held as expected

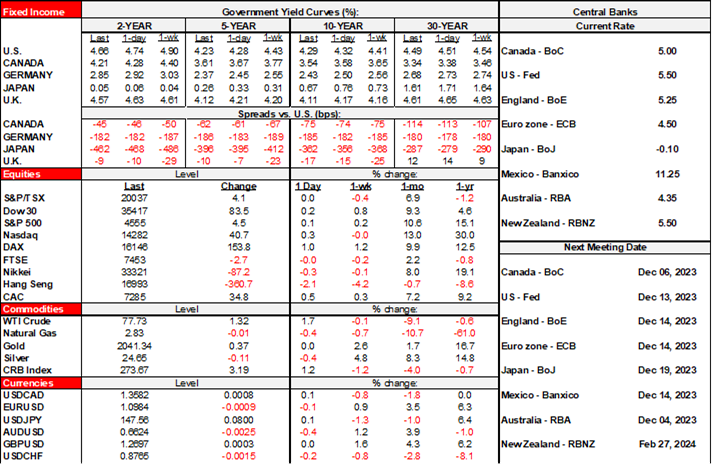

The dollar was looking set for a down day until Eurozone inflation readings hit the Euro and related crosses and added to pre-data curve richening across EGBs and elsewhere including into N.A. Kiwis went the other way on the market bias after the RBNZ’s hawkish tone. The result is helping to buoy equity markets with mild gains between about ¼% in Toronto, up to about 1% gains in the Dax and Italian equities. Oil is up by over a buck ahead of OPEC+ tomorrow. N.A. developments will be light with just US GDP and core PCE revisions. The TSX is underperforming between bank results.

Headline German inflation came in weaker than expected at –0.4% m/m (-0.1% consensus) and with the EU-harmonized reading falling by 0.7% m/m (-0.5% consensus). Most of that information had been digested earlier in the European session after the individual states released estimates between -0.3% m/m and -0.4%. Much of the weakness was in core prices ex-food and energy.

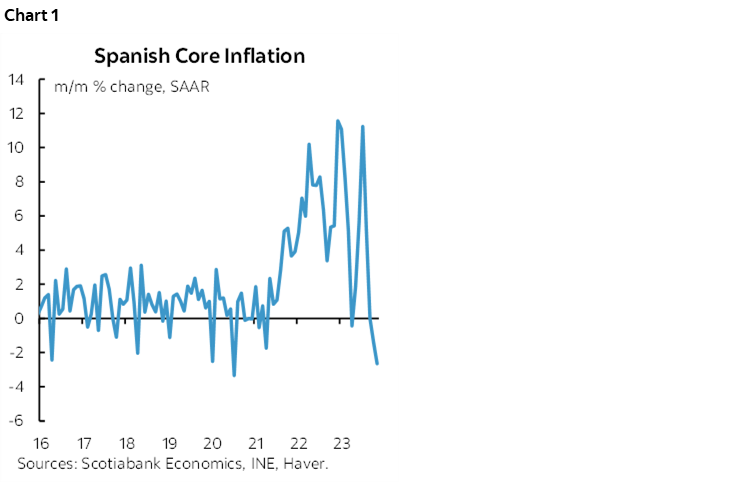

Spanish inflation then backed up the initial reactions to the German state-level data when Spain recorded a -0.6% m/m drop in EU-harmonized inflation (-0.1% consensus). Core inflation pulled back to 4.5% y/y (5% consensus, 5.2% prior). That reading is super volatile but dropped like a stone (chart 1).

The Eurozone tally arrives tomorrow morning along with figures from France and Italy, but there is probably enough evidence to point to downside risk to the -0.2% m/m headline CPI consensus for the overall monetary region.

The results added to pricing for ECB cuts with the first cut mostly priced for April along with roughly 100bps of cuts by the end of 2024 which seems aggressive to me.

The A$ fell and the two-year yield dropped a further 7bps to add to a pre-data overnight rally. The culprit was that Australian CPI also fell by more than expected (4.9% y/y, 5.2% consensus, 5.6% prior). Part of the reason is that a year-ago cut in fuel taxes dropped out of the comparison in October. Nevertheless, core CPI also ebbed from 5.5% y/y to 5.1% with trimmed mean down a tick to 5.3%. CPI was down -0.3% m/m substantially due to a 2.9% drop in fuel prices.

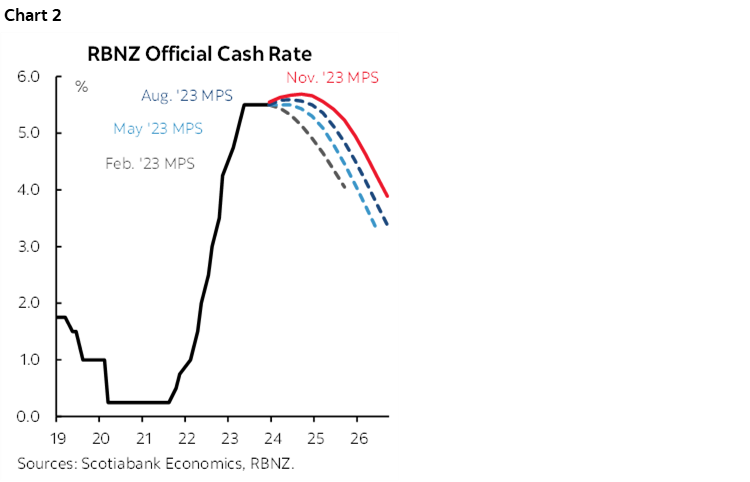

The RBNZ left its official cash rate unchanged at 5.5% as widely expected. A hawkish bias drove underperformance at the front-end that was little changed overnight versus rallies elsewhere and drove NZ$ strength. Governor Orr said that the Monetary Policy Committee was “showing an upward bias to the interest rate” and did not forecast cuts until mid-2025 while raising the explicitly guided profile for the OCR (chart 2). Part of the rationale that was given is that immigration was adding to inflationary pressures which may be familiar as a risk to BoC watchers.

Sweden’s krona is underperforming after GDP disappointed at -0.3% q/q (0% consensus).

The Bank of Thailand held at 2.5% as widely expected.

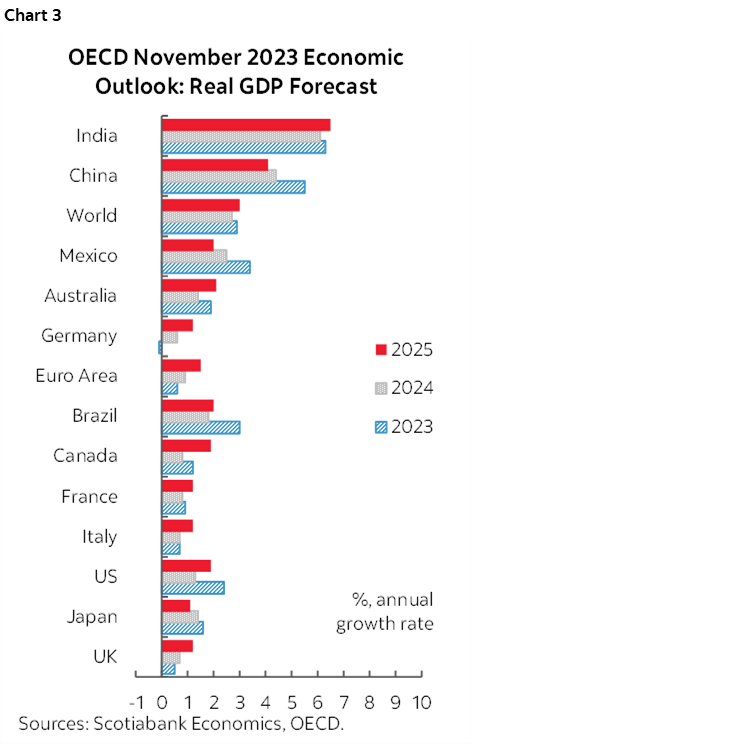

The OECD got into the act with its semi-annual Economic Outlook this morning. It notoriously lags developments, but just for kicks, their latest prognostications for GDP growth are shown in chart 3.

It was another strong week for US mortgage apps. Purchase applications were up by 4.7% w/w which completed a whole month of strong w/w gains. A big drop in refis (-8.9% w/w) offset the gain in purchase apps for a total apps number that was little changed. The seasonally adjusted purchase index is back up to September levels.

On tap will be a few US releases. US GDP and core PCE revisions arrive shortly (8:30amET). The initial prints were 4.9% q/q SAAR for GDP and 2.4% q/q for core PCE. Material revisions are not expected but markets will be particularly sensitive to any possible PCE revisions ahead of Friday’s figures for October.

The US also updates the merchandise trade figures for October (8:30amET) and inventory figures for the same month (8:30amET). The Fed’s Beige Book of regional economic conditions will be released at 2pmET.

Canada’s bank earnings season is on pause until tomorrow when three more step forward including TD, CIBC and RBC.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.