ON DECK FOR THURSDAY, NOVEMBER 23

KEY POINTS:

- European PMIs, impaired liquidity drive cheaper sovereign bonds

- What BoC Governor Macklem said, the risks and the pitfalls

- Gilts cheapen on upside PMI surprise

- EGB yields rise as Germany drivers slight EZ PMI gain

- Sweden’s Riksbank delivers surprise hold

- Norway’s economy turned in a worse performance

- Turkey’s central bank delivers mega-hike

- Bank Indonesia holds

First, here’s to wishing a safe and happy Thanksgiving to our US friends and colleagues and safe travels to everyone else as well. This will be a pretty dull session with the US and Japan on holiday today and ahead of an early US close tomorrow, for those that aren’t taking the whole day off. Liquidity will be strained, but fortunately there are no major on- or off-calendar surprises.

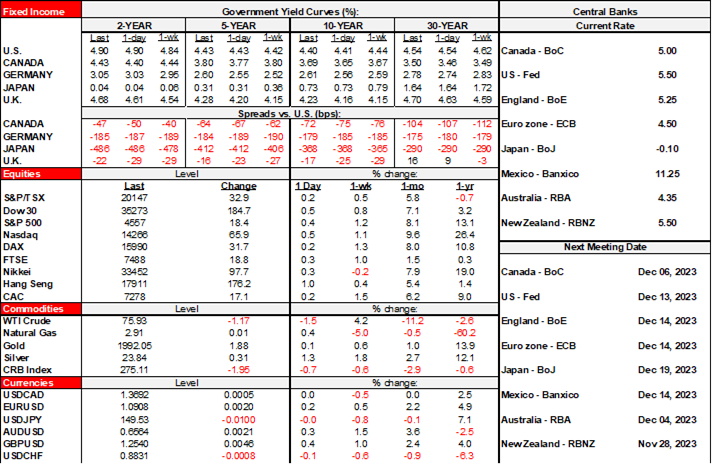

A round of very mildly better-than-expected European PMIs is driving cheaper sovereign curves across Europe. The gilts curve is shifting upward with the 2s yield about 8bps higher and 10s similar. EGBs are generally bear steepening with 10s yields up by 6bps and milder moves across core front ends. European currency crosses are among the outperformers on a morning of general USD softening, except for underperforming Scandies on a pair of overnight surprises. Equities are little changed but slightly positive.

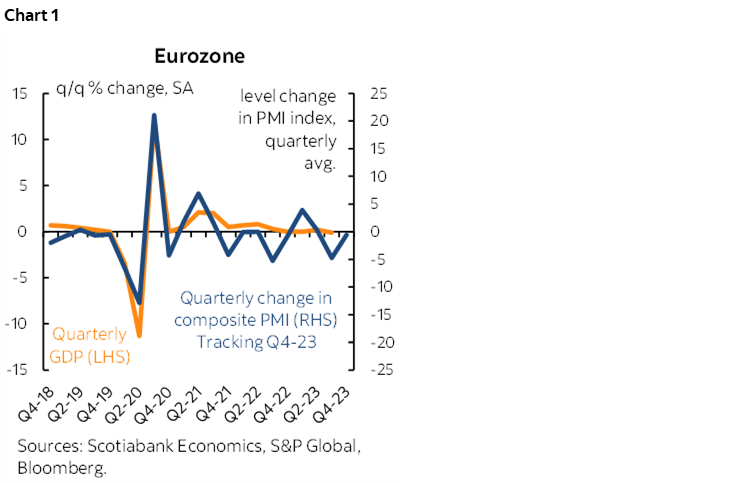

Eurozone purchasing managers’ indices were very slightly better than expected, but it’s soft data and the moves are small and so the market reactions look a bit overdone as far as I’m concerned. The composite PMI moved up six-tenths to a still contractionary reading of 47.1. Both the services PMI (48.2, 47.8 prior) and manufacturing PMI (43.8, 43.1 prior) improved a touch. Chart 1.

The first pass at the Eurozone PMIs only reveals country-level readings for Germany and France with other countries following later on. It’s noteworthy that Germany drove the Eurozone improvement as its composite PMI increased 1.2 points to a still contractionary reading of 47.1 and that this was driven by manufacturing (42.3 from 40.8) and services (48.7 from 48.2). France’s composite PMI was flat (44.5, 44.6 prior) with little change in either the services or manufacturing readings.

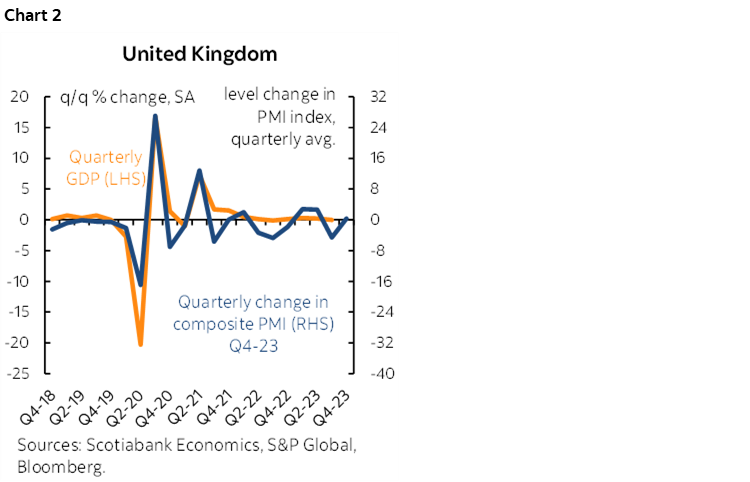

The UK posted a somewhat more material improvement across its PMIs and hence the larger curve movements. The composite PMI is indicating no growth which is an improvement relative to three months of contractionary readings. It edged up to 50.1 (48.7 prior) as the manufacturing PMI moved up 1.9 points to 46.7 and the services PMI moved up one point to 50.5. Chart 2. Recall that 50 is the dividing line between expansion and contraction.

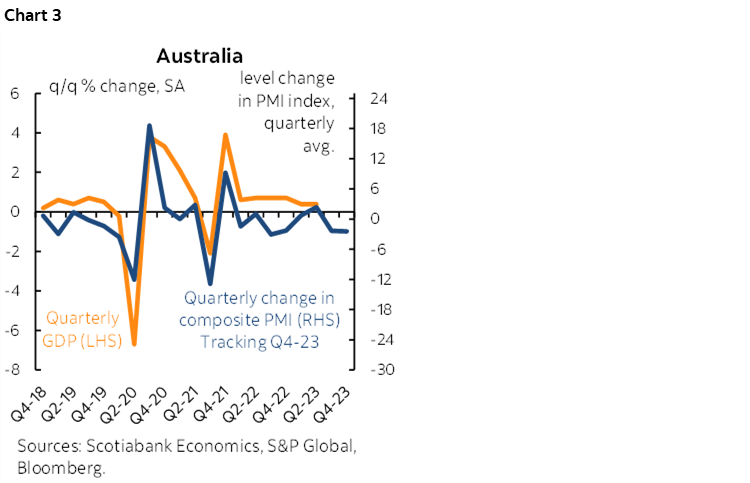

Australia’s purchasing managers’ index disappointed as it fell 1.2 points to 46.4 and thereby signals a further weakening of the economy. The services PMI fell 1.6 points to 46.3 and the manufacturing PMI fell back to 474.4 from 48.2. Chart 3.

Norway’s economy put in a sharply worse than expected performance, but I don’t have a great explanation for why the krone and curve ignored it. GDP shrank -0.5% q/q SA nonannualized in Q3 and the prior quarter was revised down a half point to a -0.5% contraction. One possible explanation for ignored it is that Q3 ended on a high note as monthly GDP was up 0.3% m/m (0% consensus) but that beat was mainly due to a downward revision to the prior month (-0.4% m/m from -0.2%).

Sweden's Riksbank surprised most folks when it held its policy rate at 4% this morning, though it had been a somewhat close call. The bias indicated that the policy rate “may be raised further at the start of next year and that monetary policy needs to be contractionary for a relatively long period of time.” 13 out of 21 in consensus thought they’d hike 25bps and 8 got the hold right. Markets thought they’d hike and so the whiff sparked front-end out-performance compared to the rest of Europe as 2s rallied 5bps. The Krona is little changed but underperforming on a morning of general USD strength.

Bank Indonesia held its one-week reverse repo rate at 6% as most had expected.

Turkey's central bank hike another 500bps, or double consensus, to a new one-week repo rate of 40% that only one wheel spinner got correct out of 25 in consensus. So, the lira soared, right? Wrong. It gained a little but is generally underperforming other EM crosses and several major ones. One reason for that is that while the central bank indicated it would keep tightening, it said it would slow the pace and is near the end of the process as explained by the following quote:

“The Committee assessed that the current level of monetary tightness is close to the level required to establish the disinflation course. Accordingly, the pace of monetary tightening will slow down and the tightening cycle will be completed in a short period of time. The monetary tightness will be maintained as long as needed to ensure sustained price stability.”

Another reason is that the real policy rate remains negative by over -20% using backward CPI inflation of 61.4% y/y. Using the consensus forecast for inflation next year of over 50% y/y it doesn’t seem that the real policy rate will turn positive any time soon.

SARB is widely expected to sit things out again this morning (>9amET).

BANK OF CANADA GOVERNOR MACKLEM IS HEDGING HIS BETS

Governor Macklem’s speech (here), audience Q&A and press conference didn’t really leave us with much by way of any new information on net. Salient takeaways from his remarks are summarized below under key sections for individual topics.

My reading is that we're in a period of extreme data sensitivity that the BoC’s bias is struggling to adapt toward. Hikes are improbable, but not impossible. Cuts are premature, but it’s reasonable to be thinking ahead. Forecast with great confidence at your peril. If, for instance, we get several months of low m/m SAAR core inflation measures, then markets are going to run further with it at a super awkward time with the Winter budget season and mortgage pre-approvals season into the Spring housing market. I worry about that scenario the most in terms of reigniting pressures because I want to see bigger cuts later, not smaller ones too soon that then backfire. The case for more cuts on a sustainable business would be better rewarded by some heat over coming months and then relief. If on the other hand this very recent soft patch for inflation proves transitory then we can’t get too ahead of ourselves in ruling out further tightening while being very cautious on pricing cuts.

Struggling to Hit the Right Balance

The key quote in his speech was the following one that struck the balance between not wanting to overdo it versus being concerned about messing up like they did in the 1970s:

"The lesson from the 1970s is that fighting inflation half-heartedly and living with the stress, labour strife and uncertainty inflation can cause would be a huge mistake. The right way to respond is with a firm commitment to restoring price stability. But we don’t want to avoid one mistake only to overdo it on the other side. We are trying to balance the risk of over- and under-tightening. If we do too much, we risk making economic conditions unnecessarily painful for everyone. If we do too little, Canadians will continue to endure the harm of inflation and we will likely have to raise interest rates even higher later."

And Macklem also said they’re probably done hiking, but maybe not:

"This tightening of monetary policy is working, and interest rates may now be restrictive enough to get us back to price stability. But if high inflation persists, we are prepared to raise our policy rate further."

On Timing Rate Cuts

Macklem repeated earlier guidance by saying “We don't have to wait until inflation is back to 2% before we cut but we need to wait until it is clear that we are on that path and then we can start to consider when we may cut interest rates.”

When asked what he will need to see in order to begin to cut he started by saying that the recent inflation number was encouraging and that they expected inflation to come down and it did and that's good news for Canadians. He did, however, caution that we've been down to 3.1% y/y before and then came back up and that there is underlying volatility. They are looking for clear evidence that underlying trend inflation is down. Macklem observed that underlying inflation has been running around 3½% y/y for some time and that one month is not a trend. Macklem reinforced these points by saying:

“We need to see a number of months that we're on a path to 2% inflation. When we are on that path we will begin to think about when to cut interest rates.” He backed that up by saying “Right now we're still assessing whether they are high enough. The lesson from the 1970s is not to be half-hearted in getting inflation back to target.”

So now the issue is what is “a number” of months, how will the data evolve, and what lags will follow the period from achieving “a number” and the first hike? All three are highly uncertain. Would six months of soft inflation be enough? Maybe, maybe not. Will data cooperate? Maybe, maybe not, we need to be careful in tracking the data and the myriad influences upon inflation risk that go far beyond tracking GDP growth relative to made up estimates of potential growth. Would they want to react instantly once starting the dialogue on cutting? Maybe, maybe not, but I’d think there would be some lag to set it up to a degree. So, if all goes just peachy, then maybe a Summertime cut as we show? Possibly later. March or April as markets have been flirting with? That seems aggressive to me.

Mostly Dismissive of the 1970s

In the rest of his comments, Macklem sounded more like he was less worried about repeating the 1970s experience and more concerned about overdoing it. In dismissing the 1970s, the first caution is that one should naturally expect this from a central banker since saying he won’t be able to control inflation just as badly as central banks messed up back then is basically declaring sheer incompetence. His job is also to cheerlead folks into believing he’ll succeed in bringing inflation lower which is why the street’s job is to challenge the central bank in service to clients.

The crux of his argument for what makes today different from the 1970s, however, is two-fold and on both counts he’s making rather dubious claims to try to jawbone markets into believing what he says.

First is the BoC’s claim to remarkable success in targeting 2% inflation. Macklem says that since adopting this target about 30 years ago, they have spent most of the time in the 1–3% inflation band. That’s generally true, but why? Is it because of their framework? Or was it a fluke as the same held true for many global central banks over this period?

The case for it being a fluke has more to do with disinflationary global macroeconomic forces such as China’s accession to the WTO, technological change and demographics. Central banks should be a little more humble with respect to the period of low inflation that wasn’t all about them versus the structural drivers, and less confident toward their future ability to control inflation if structural forces has shifted in the other direction as I think they have.

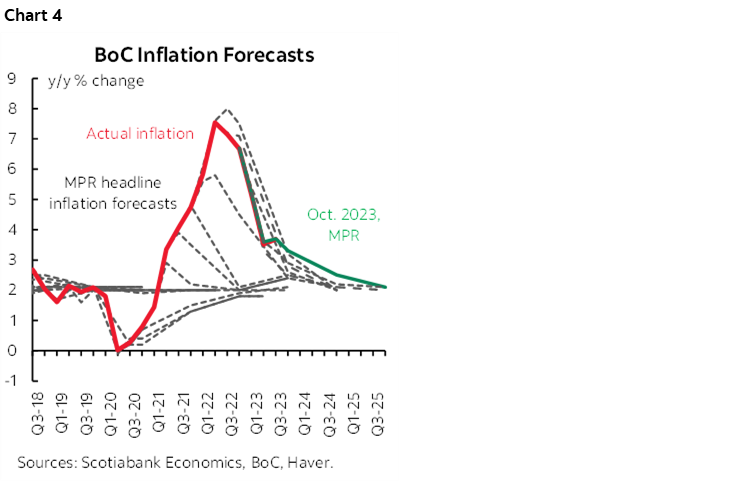

Furthermore, even within this 1–3% target band, what really matters in tracking BoC policy over this period is how successful they were at forecasting inflation in order to guide their policy moves. They can’t forecast inflation. Successive MPRs over a long period of time have proven that by routinely missing the turns and overshoot or undershoot. Chart 4 shows this in a shorter time interval starting just before the pandemic. It also shows that they always show a magical return to 2% inflation within the forecast period versus reality. That matters. A lot. Because when this is the track record, it can drive periods of excessively liberal easing and overdoing it on tightening. The BoC will never, ever admit it, but their wild policy swings have sowed instability in the economy and asset markets including housing over time.

His second argument is that they didn't dither this time versus the 1970s. That's sort of true I guess, but not entirely. They definitely dithered this time when they were dismissive toward inflation risk until starting to hike finally by March 2022, but not for as long as the 1970s experience. Macklem was delivering speeches on targeting fully inclusive maximum employment in 2021. He ignored inflation’s warning signs and all of the data as it was pivoting higher. Let’s not let them be revisionists here. Macklem promised Canadians that the policy rate wouldn’t materially budge for years, reeled in suckers who believed it and borrowed excessively, and then dismissed early inflation signs as driven by year-ago base effects, narrow drivers like gas prices, and was transitory in nature. He and other central bankers let the cat out of the bag on inflation by retaining emergency levels of stimulus for far too long after the emergency had passed and set monetary policy’s focus upon a high-risk experiment to push the frontiers of defining maximum employment.

That’s a little stronger language in favour of being done without explicitly ruling out any further hikes. Why? One possibility is that they genuinely want to leave options open given uncertainty toward inflation risks. Another remains that they are holding out this threat to manage markets away from pricing overly aggressive easing too soon; if that’s their aim, it’s not really working so well relative to market pricing.

Defining the High Costs of Inflation

Macklem explained the high costs of inflation in layperson terms to labour markets, businesses and consumers with the following comments.

He went on to explain some of the costs of high and volatile inflation from a labour market standpoint:

"With higher inflation in the last couple of years, we’re seeing more strikes as employers and workers struggle to reconcile rising costs on each side. Nobody wants this—workers don’t want to strike, and employers don’t want work to stop. But high and unpredictable inflation makes it difficult to agree on fair compensation for work, and that leads to strikes. When inflation is high and volatile, contracts get shorter, negotiations are harder, and uncertainty is higher for everybody."

He did likewise from a business product pricing standpoint:

"Businesses have also changed the way they price their goods and services, raising prices more often and by larger amounts. That hurts their relationships with customers, raising suspicion and blame."

And from a consumer standpoint:

"And inflation is changing behaviour. We can see in our surveys that families are changing their spending to protect themselves from inflation. They’re spending less and trying to find cheaper goods and services."

Setting a High Bar for GDP Surprises

Macklem made it pretty clear they wouldn’t be suddenly knocked off course if growth is weak going forward which implies we’d need to see a sharper downturn than they expect in order to motivate a sudden, early policy pivot. Here’s the quote:

"We expect the economy to remain weak for the next few quarters, which means more downward pressure on inflation is in the pipeline. In short, the excess demand in the economy that made it too easy to raise prices is now gone."

Mortgage Resets

What's not in the speech is also interesting. There was zero reference to mortgage resets.

He was, however, asked about how concerned he was about mortgage resets. He said that about 40% of mortgages have reset and 60% are left. Macklem said this is squeezing Canadians as resets occur each month, but that this s how monetary policy works and brings spending and inflation down. That’s a shot at those arguing that the BoC will be forced to cut to come to the rescue of those facing resets and I still don’t come close to buying into their math in any event. That’s important because he’s basically saying he’s focused upon the bigger picture. He went on to say that they don't want to make this any more painful than they have to but are determined to bring inflation down. Macklem observed that so far Canadians are paying their mortgages but that it is more difficult and this is helping to get inflation down.

Wishful Thinking on Wages and Productivity?

Macklem was asked whether wage gains being secured by union groups are significant and what effect this may have.

He answered by saying that they want to see higher productivity with those higher wages but that wage growth is running at 4–5% (he's using y/y, m/m SAAR trend is double) and productivity is weak. Macklem said that they expect a gradual easing of wage pressures as job markets come back into balance and that they are also expecting a pick-up in productivity growth. In my view, we’ll see about that; the BoC has been expecting productivity to rebound for a while now and has been disappointed, while the drivers of a sustained improvement in productivity are hard to imagine.

Not Fussed by the Fed’s Fiscal Update

When asked whether the Federal government was restrained enough in spending to avoid the 1970s inflation risk, Macklem said it’s not their job to comment on fiscal policy and then commented. He said that over the next two years the Federal budgetary balance is little changed in this week’s updated Statement relative to the Budget from earlier this year. Over this time period, he said that the Federal government is not adding new or additional stimulus which is the period over which they will be looking to get inflation back to target. He did note that there was some additional spending in the outer years across Federal and provincial governments that they will be building into their outlook. Recall that Macklem has previously said government spending across all levels was expected to be above the supply side’s ability to manage it such that it would contribute to inflation in 2024.

Are Wages Driving Services Inflation?

Macklem was asked to comment on the connection between services inflation and wages. He said that most services inflation is coming from shelter. Ex-shelter, services inflation is only 2.3%. He argued that therefore we are not seeing much evidence that higher wage growth is passing through into service inflation.

In my opinion, wage growth is partly buoying shelter costs among many other influences. Secondly, there are probably lags that the Governor should be considering. Wage growth has super accelerated of late in m/m SAAR terms this year. If that persists, especially relative to tumbling productivity, then this could carry services inflation higher in future.

Was the conditional pause in January a mistake?

Macklem was asked if January’s conditional pause was a mistake and whether he would agree they are in another conditional pause right now.

Naturally he said it wasn’t a mistake, and that it made a lot of sense given how far they had moved so quickly so they took a breather before coming back with two more hikes in the summer.

In my view, it was a mistake, and his approach to this earlier period presents the non-negligible risk they may do it again. It was a mistake because of its timing and how the bias was mismanaged. They gave the green light to markets to think they’re done and that the next move is down which contributed to cheaper rates on fixed rate mortgages into the highly seasonal Spring market.

On whether they are in a conditional pause now, Macklem said the following:

“We are very much taking it one meeting at a time. Monetary policy may be sufficiently restrictive. We may need to have to do more. We need sustained evidence that underlying inflation is coming down and one month doesn't prove that. If underlying inflation persists there may be a need for higher interest rates.”

Inflation Expectations a Concern

When asked whether inflation is at risk of becoming entrenched in the economy, Macklem started by saying that long-term inflation expectations are around target but shorter-term expectations of inflation have risen. He said their surveys show that expectations are coming down slowly and are above our forecasts which is a concern because it can be a problem for getting back to 2%. He remarked that they will be watching for shorter-term inflation expectations to come back to 2% but that if they saw that those shorter term inflation expectations are stalling above our target then it would be a sign that inflation is becoming entrenched and would concern us. The money quote here was “We are concerned that those inflation expectations are coming down slowly.”

Excess Supply Expected to Build

Macklem was asked whether his remark that excess demand is now gone means that spare capacity now building and for how quarters do you think it will be required for this to occur before you are prepared to consider rate cuts?

He started his answer by saying that a broad range of indicators is at least approaching a flip from excess demand to excess supply. He noted that some indicators suggest we're already in excess supply and others suggest maybe we're still in excess demand so that we're either approaching or already in a little bit of excess supply but it's hard to be super precise. He stated that the excess demand that was contributing to inflation is now gone. He then went on to say that we do expect to go into excess supply through 2024 and then into 2025 that excess supply will begin to be absorbed.

The caveat to all of this is that inflation has many drivers of which the domestic output gap framework of excess demand and supply is only one and a highly difficult one to forecast out of sample alongside made-up estimates of potential growth.

In all, I have to admit that given the costs of high and volatile inflation and how that can be very damaging for a long period of time, I would still prefer the Governor to be willing to embrace overdoing it rather than chickening out. He’s under a lot of pressure mind you. The risks to overdoing it with further hikes (a sharper economic deterioration) are outweighed by the risks to allowing wage and price setting behaviour alongside moribund productivity to define the economic landscape for a generation. That could be especially true if the BoC is misjudging whether inflation risk has fundamentally changed for reasons that are less about their little world and more about broader structural reasons.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.