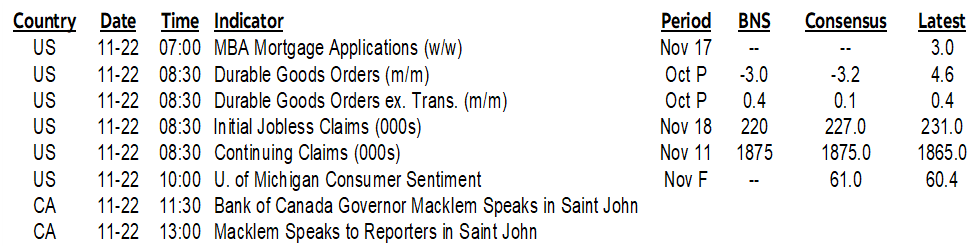

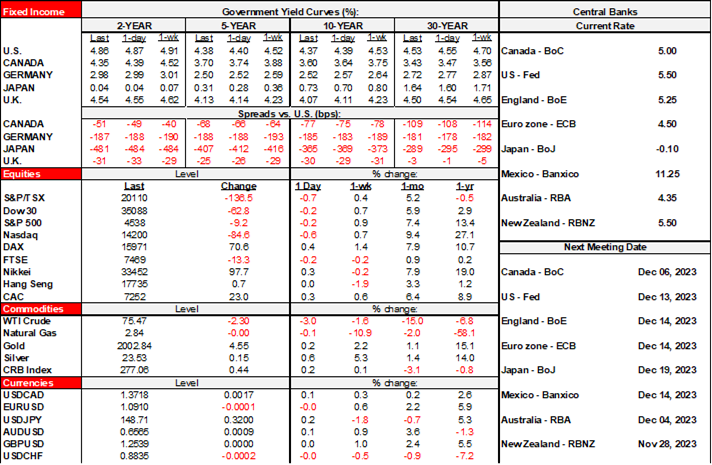

ON DECK FOR WEDNESDAY, NOVEMBER 22

KEY POINTS:

- Markets are about to go very quiet as US markets begin shutting down

- BoC’s Macklem to speak on inflation’s costs

- What I liked and didn’t like about Canada’s federal fiscal update

- US durable goods orders to drop as plane orders move lower, but not low...

- ...but watch core orders as cap

Don’t stand by the exits on any US trading floors this afternoon. You’ll get burned by the breeze created by folks fleeing toward unofficial early exits in order to hop into planes, trains and automobiles ahead of US Thanksgiving. Then all goes quiet stateside and quieter elsewhere. In some ways, it already has.

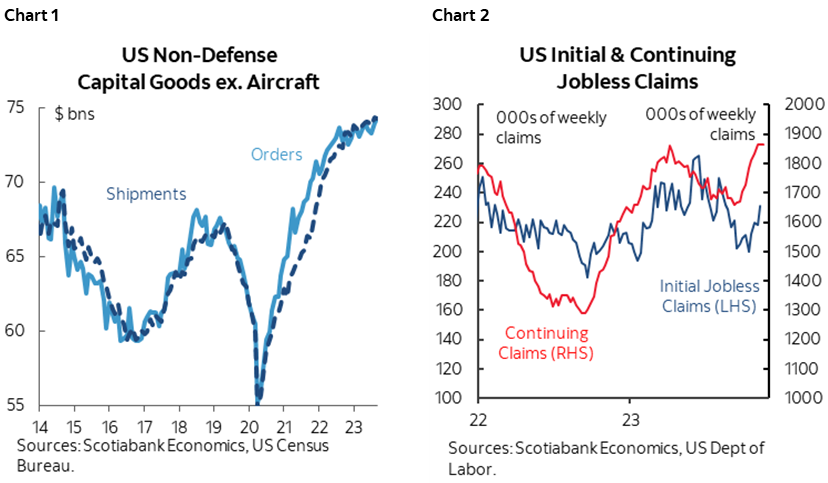

Before we get to that, however, there will be minor US data. Watch durables that are expected to decline on lower (not low) plane orders, but core orders will matter more and they have been levelling off at high levels albeit with growth petering out (chart 1). Also watch claims to see if the prior week’s mild rise and slight upward trend have been aberrations (chart 2).

Then it’s over to BoC Governor Macklem and his speech on “the cost of high inflation.” It will go live at 11:30amET followed by a 1pmET press conference. Expect him to turn his nose up at yesterday’s Federal fiscal update. He won’t embrace specifics but will very likely repeat his earlier warnings about how government spending will add to inflation risk into next year and yesterday’s added spending doesn’t help. Nor will it at the provincial level.

He’ll cite progress on some measures of inflation but emphasize that there is enough going on to say they remain a considerable distance away from durably achieving 2%. Examples include still high breadth, accelerating service price inflation, uncertainty toward core goods price inflation. He could also reference high wage gains relative to productivity and several other upside risks to inflation. His prior guidance in the October MPR pushed out durable achievement of 2% inflation to 2025H2 and said that easing could commence before then, but it would be unlikely to unfold as soon as markets are pricing. Watch to see if he indirectly leans against market easing.

CANADA’S FISCAL UPDATE—LIKES AND DISLIKES

There was plenty of instant coverage right out of the embargo on yesterday’s Canadian Fall Economics and Fiscal Statement and frankly there were few if any material surprises given the ages-old practice of divulging most of the contents through leaks and story plants in advance. Long gone is the era in which folks flocked to morning-after breakfast presentations to hear what economists, consultants and accounting firms think about it. We had Rebekah in the lock-up and her views and portrayal of the numbers are here. Clients can also check out Roger Quick’s piece that was more focused upon debt management. With that in mind, here is my brief take on things I liked and didn’t like about the Statement.

1. It’s based upon stale projections

The private sector forecast inputs are stale. The deadline for sending in forecasts to Finance was September 12th for an update that was delivered yesterday. That means the forecasts are stale by a minimum of just over two months. In some cases, shops submitted forecasts that were even older and from their July rounds. That’s unacceptable. Forecasts should have been much fresher for a November 21st document given the speed of developments including in financial markets over this period. Ergo, take it all with a heavy dose of salt.

2. Spending is excessive

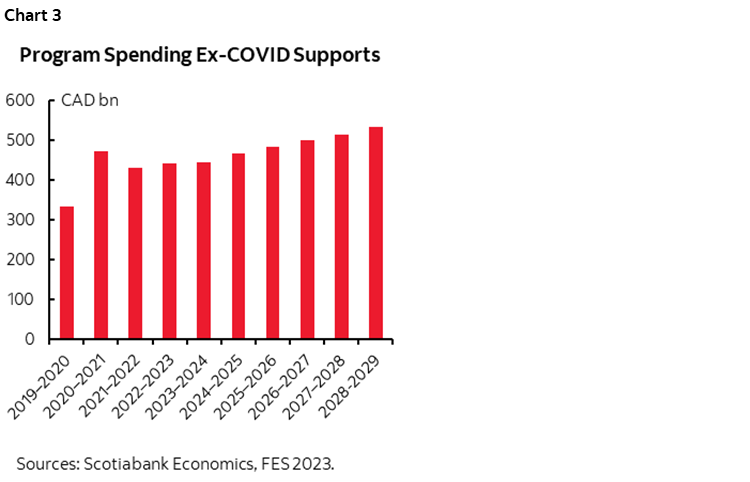

Another roughly C$21 billion in net new revenue and expenditure measures was added over the six-year projection horizon.

Some will say that’s not a big deal in relation to the size of the economy. That’s what they’ve said every time largesse gets bumped up and they wind up sounding like serial apologists. The cumulative result is shown in chart 3. By the fiscal year 2028–29, federal program spending excluding earlier temporary Covid supports will be about C$200 billion higher per year than it was in the fiscal year just before the pandemic struck. That’s a rise of 60%. This reflects the baked in program spending increases contained within prior budgets plus this update. Note the UK’s different approach this morning as Chancellor of the Exchequer Hunt delivered a significantly different plan in his Autumn Statement.

The Canadian plan is hardly about prudent spending in my books and then layer on the even more profligate provincial and municipal governments of all political stripes in a country devoid of any fiscal conservatives in power. Governments were opportunistic in using the pandemic as an excuse to spend more on shiny things for short-term purposes on a permanent basis. They took bad advice from folks who told them bond yields would be uber low forever and inflation would never be a worry and so they opportunistically spent much more on short-term populist things while shunning productivity-oriented measures. Have more candy today, good luck tomorrow.

The result is ongoing pressure on inflation and no help for the Bank of Canada’s inflation fight. I’ve argued for years that fiscal largesse would come at a cost through rate hikes and Canadians are seeing this first hand now whether they can connect the dots or not.

3. Debt myths

There’s nothing to worry about because net debt to GDP especially at the Federal level alone is favourable compared to other countries, right? Nonsense. Try liquidating the financial assets netted out in that calculation if debt servicing becomes imperilled. Gimme those sinking funds, SWF assets and your pensions will ya, please, c’mon, be a pal would ya, pleeeeasse?!

Gross debt to GDP is not an irrelevant metric by any means and yet these documents always downplay it or avoid mentioning it altogether and even fiscal apologists in the private sector dodge the issue. Canada has more debt across all levels of government combined relative to the size of its economy than the OECD average (here). In 2022 Canada stood at 113% on this measure versus the OECD average of 89%. We’re lower than Japan’s largely captive bond market backed by its reserve currency which isn’t terribly comforting. Canada has less debt relative to GDP than the Biden administration which I’m sure is heartwarming to fiscal conservatives. Canada is lower than France that just got rebuked by the EU. Oh, and Canada is lower than Italy, where politics and deep fiscal challenges flare every few years. Nah, nothing to worry about it, it’s all under control folks.

Well, yes there is. The interest expense on all that debt will climb to an eye watering C$61B per year by the outer year of the forecasts and even that relies on the aforementioned stale forecast inputs. That’s a doubling of what was being spent on interest expense into the pandemic. This surge hardwires permanent deficits, hence no plan to return to balance because they can’t. Not without severe program spending cuts that this government has no appetite for pursuing. Toss in a nasty recession if one happens despite none being forecast in their numbers and debt issuance and debt charges would balloon even further. That’s how it happened in the past, through policies that entail always living on the edge in the moment while hoping it never rains. If it does, it’ll be someone else’s problem. This public debt charge comes at the expense of future generations and is symptomatic of a government that is spending beyond its means in serial fashion. It makes it vastly harder to pursue wealth-creating and productivity-oriented reforms as the interest bill on social program spending is in the driver’s seat.

4. Nothing to address the country’s real problems

Worried about Canada’s moribund productivity? The lost comparative advantage on corporate tax reform that the country once enjoyed? High personal tax rates that make life less affordable for many? Soaring unit labour costs and the growing loss of competitiveness especially within NAFTA? High inflation and rate hikes caused in part by runaway fiscal largesse? Excessive immigration that is making infrastructure shortfalls and housing deficiencies even worse?

Well, the Feds flipped the bird at anyone with any of those apparently illegitimate concerns and in so doing appear out of touch. There is nothing substantive on productivity beyond six token word references and no proposals on what to do about how awful it is. Their idea of a plan is to pick winners and losers while spending ridiculous sums on subsidies to manufacturers of electric car batteries at an absurd cost per job with apparently most of the proceeds flowing to foreign shareholders and foreign workers. Good one. Beat on grocery chains when Canada’s food price inflation is much lower than many other parts of the world and has common drivers. Wag a judgemental finger at the nation’s key industries while constantly trying to push them down. There was no reference to doing what’s necessary (imo) to reduce excessive immigration. The housing incentives are a drop in the bucket compared to what’s needed and face high implementation risks and the policies are at loggerheads by raising the after-tax cost of capital through the changes to short-term rentals.

What’s unfortunate is that the best way to make homes more affordable and to make future program spending more affordable would be to enact policies that stoke growth in productivity and incomes. The government’s emphasis upon distributional policies doesn’t achieve this.

5. It seeks to buy off the media ahead of the next election

While they stuffed the moms and pops who invested their retirement savings into short-term rentals, they gave more hand outs to the press. Another C$129 million in tax credits with the reasoning being that the sector is losing jobs. It’s a $30k incentive per employed journalist. You’ve got to be kidding me. Canada’s public policy bias to support jobs over productivity, technological change and quality shone through on that one. Talk about how to buy off favourable coverage from the media. This is pork barrel politics plain and simple. Not surprisingly few media outlets pointed this one out but kudos to the one(s) that did. Will there be a hand-out for other sectors that have or will have to cut jobs, or is this just for the influential media that writes stories about your government that’s down in the polls on the path to an election no later than October 2025?

6. The assault on short-term rentals

If you are among the folks of fairly modest means who invested their retirement savings in short-term rental units trying to generate added income in a challenged economy then you just got slammed by the Feds. Creditors financing these units may share in the losses. See yesterday morning’s note for the pitfalls here.

7. Shelved plan to cancel CMBs issuance

Hooray! Love this one. Finance has behaved in curious ways with surprise announcements on core funding programs like cancelling 3s out of the blue and musing about maybe cancelling the CMBs program. That has made it look rather sloppy in terms of consulting the street on debt management and the functioning of financial markets. Frankly most folks can’t really figure out why they tinkered with expectations around this program to begin with.

8. A toothless mortgage charter

On the so-called "New Canadian Mortgage Charter" highlighted on page 27 of the update, Freeland dodged a question on whether this would become legislation. It appears to be voluntary which is an indication that they’ve gotten a fair amount of blowback on it perhaps from within Ottawa itself. No new legislation or regulations will accompany the charter that would implement it. That’s also a good thing.

That means that eliminating the requirement to requalify under the mortgage stress test if they switch lenders at renewal is not backed by legislation. Such a step would have lowered a key safeguard within the financial system in my view.

Eliminating prepayment penalties is also fraught with complications. That would make Canada’s mortgage market take a step along the same path as the US market with one-way refinancing options that raise lending risks that could have been countered through other adjustments to lending terms over time.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.