ON DECK FOR WEDNESDAY, NOVEMBER 15

KEY POINTS:

- Equities continue to rally as markets may be prematurely pricing Fed cuts

- Rates, FX markets move on from yesterday’s US CPI

- Shutdown averted, but US government dysfunction will return

- PBOC holds policy rate as most expected

- Chinese macro readings were mixed

- Australian wage growth skyrockets, markets probably shouldn’t have ignored it

- UK core CPI wasn’t that weak

- US retail sales are expected to be soft

- US mortgage purchase applications jump for a second week

- US PPI could largely mirror CPI

- US Empire gauge to kick off the march to the next ISM-manufacturing print

- Canada to updated home sales, manufacturing, wholesale

- Colombian GDP may rebound

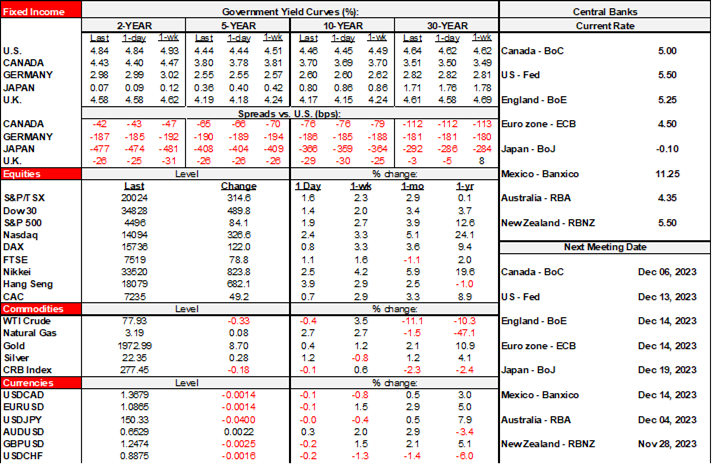

There isn’t much follow-through on yesterday’s rallies across asset classes following a mildly softer than expected US CPI print (recap here) and traction toward averting—or perhaps merely delaying—a US government shutdown. I still think the market reaction to CPI was overdone; markets are far too sensitive in both directions to minor swings in data over recent months and not demonstrating much by way of an ability to think about bigger picture thematic matters over time. Nothing overnight proved to be terribly impactful as markets await US retail sales. Treasuries have a very slight cheapening bias along with Canadas and longer dated gilts whereas EGBs have a very slightly richening bias. Stocks are up by ¼% to 1% across NA futures and European cash markets following stronger gains across Asia-Pacific benchmarks that played catch up overnight. The USD is stable on a DXY basis.

Here’s a recap of developments from late yesterday through the overnight session and before turning to expectations into the North American session.

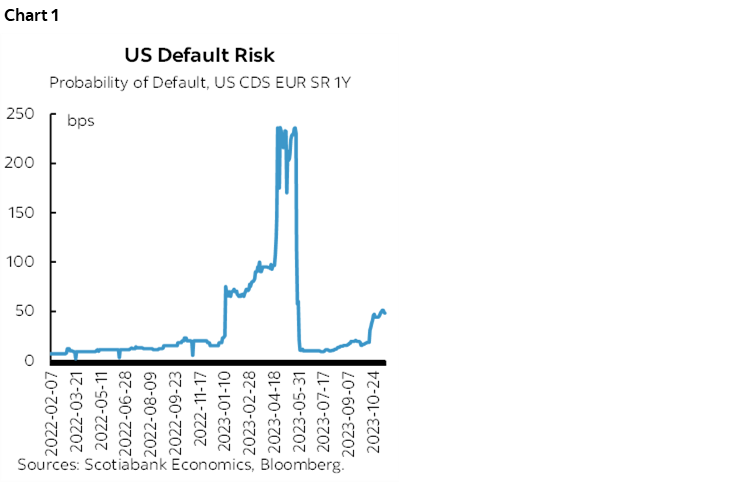

US GOVERNMENT SHUTDOWN AVERTED/POSTPONED

The US House of Representatives voted 336–95 in favour of a continuing resolution to fund the government past this Friday’s expiration of the current funding agreement. Now it’s onto the Dems-controlled Senate which is likely to pass it given that 209 Dems supported the bill in the House. After that it’s onto President Biden’s desk and must be signed by Friday at midnight in order to avert even a temporary government shutdown on Saturday. The dysfunctional US political system will be back at it all again given the two-stage approach this time with some funding expiring by January 19th and other funding expiring by February 2nd. CDS default pricing never climbed as high as it did around the debt ceiling fracas earlier this year but may remain volatile on path to the next round of turmoil (chart 1).

PBoC HOLDS POLICY RATE AS MOST HAD EXPECTED

The PBOC left its 1-year Medium-Term Lending Facility Rate unchanged at 2.5% as widely expected. A tiny minority had thought they might cut, but they’ve been wrongly saying that for a while. This probably means that the banks will then leave their 1- and 5-year Loan Prime Rates unchanged at the start of next week with the fiver being key to the property market.

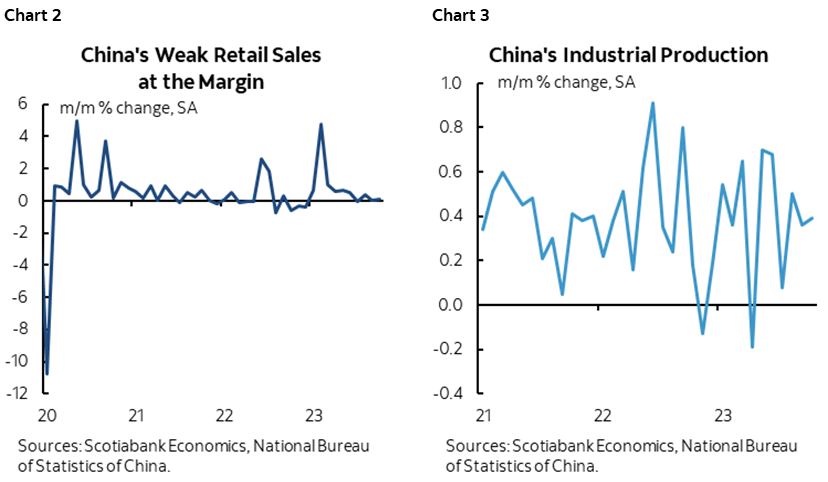

CHINESE MACRO DATA WAS MIXED

Chinese year-over-year macro readings for the month of October were mixed. Retail sales were up by 7.6% y/y (7% consensus) which on the surface looks like a mild beat, but this beat was driven by shifts in year-ago base effects while for the second consecutive month sales were weak in month-over-month terms at just 0.07% m/m SA (chart 2). Industrial production, however, was up 4.6% y/y and roughly in line with consensus at 4.5%, but it was up by 0.4% m/m SA for a sixth straight month of decent gains (chart 3). Fixed asset investment disappointed a touch at 2.9% ytd y/y (3.1% consensus). The jobless rate held unchanged at 5% as expected.

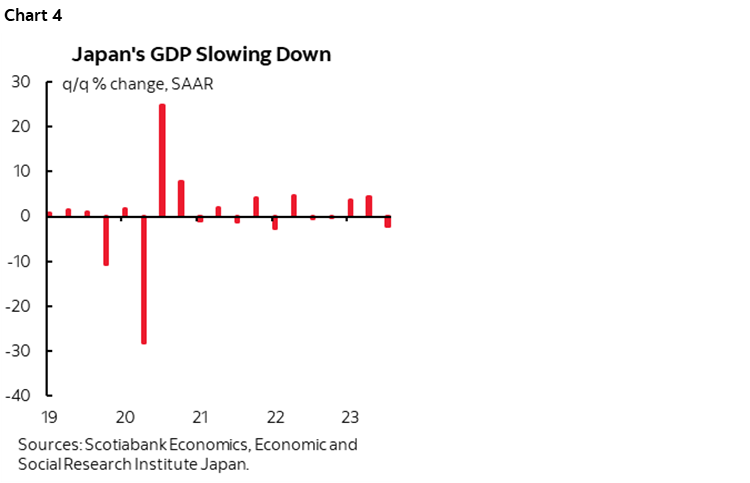

JAPAN’S ECONOMY DISAPPOINTS

Japan’s Q3 GDP landed considerably worse than expected and the details were weak. GDP contracted by 2.1% q/q SAAR (-0.4% consensus) and should have gotten a mild assist from a slight downward revision to Q2 (4.5% instead of 4.8%) but clearly did not (chart 4). The downside surprise came through consumption that was flat (consensus 0.3% q/q SA nonannualized) and revised down for Q2 to -0.9% q/q SA from -0.6%. Business spending also disappointed at -0.6% q/q SA nonannualized (+0.1% consensus). The yen shook it all off and retained the appreciation to the USD that had followed the prior day’s US CPI figures.

AUSTRALIAN WAGE GROWTH SOARS

Australia’s wage growth matched expectations at 1.3% q/q SA nonannualized and reinforced the RBA’s decision to hike last week alongside a hawkish bias. The annualized rate of increase is over 5% q/q SAAR (chart 5). That’s the fastest gain since the inception of the series in 1997. The A$ nevertheless shook it off and the Australian rates curve rallied on US CPI effects which I’m not sure was the correct response to the kind of wage-price dynamics the RBA is facing. It could be that markets played it safe ahead of tonight’s job market figures.

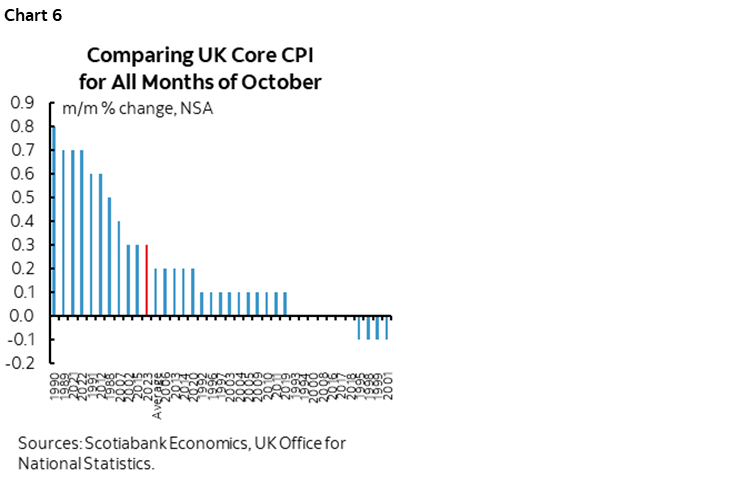

WHY GILTS LARGELY IGNORED WEAKER THAN EXPECTED UK CPI

UK CPI landed a tick weaker than expected at 0% m/m NSA. Core CPI was also a tick weaker than expected at 5.7% y/y but at 0.3% m/m NSA it was slightly firmer than the average of past months of October which is the way to look at seasonally unadjusted data (chart 6). This merely reinforced pricing for no change at the December meeting and pricing for later meetings initially fell but subsequently reversed as the morning progressed. The gilts front-end largely ignored the data after rallying yesterday following US CPI. Sterling, however, is among the weaker crosses to the USD this morning.

On tap into the N.A. session will be the following developments after US mortgage applications jumped by 2.8% with purchase applications up by about 3% w/w for the second consecutive week.

- US retail sales are expected to dip due to what we know for auto sales and gasoline prices but may post mild nominal growth in core sales (8:30amET).

- US producer prices are expected to almost mirror yesterday morning’s CPI numbers in terms of soft headline and slightly more resilient core measures (8:30amET).

- The US Empire manufacturing gauge (8:30amET) kicks off the regional surveys’ march to the next ISM report.

- Canada updates existing home sales that will probably slip again which remains the point of the exercise to tighten monetary policy (9amET).

- Just before that we’ll get Canadian manufacturing sales for September (8:30amET) that was previously guided to be little changed at –0.1% m/m SA, and Canadian wholesale sales ex-energy and grains (8:30amET) that were previously guided to be unchanged.

- Colombia releases Q3 GDP (11amET) that is expected to rebound from the Q2 contraction.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.