ON DECK FOR TUESDAY, NOVEMBER 14

KEY POINTS:

- Markets await US CPI

- The net share of US small businesses planning price hikes hits highest in a year

- The US House might vote on a funding resolution today to avert a shutdown

- UK wage growth slows to a crawl as payrolls pick up

- Speculation toward Chinese housing stimulus

- German monthly surveys start off on a positive note

Today’s prime focal points include US CPI for October, a possible House vote to avert a shutdown if plans survive some mischief making, speculation that China may introduce housing stimulus and very mixed UK labour market readings.

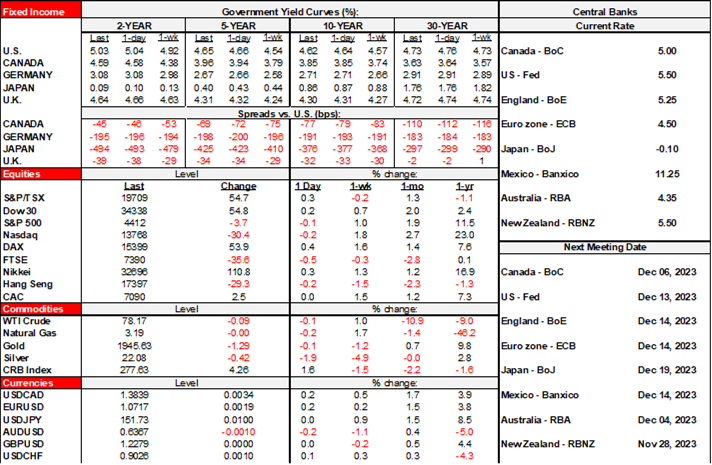

Markets are so far in a slightly constructive mood with mild gains across US equity futures and European equity cash markets notably ex-London and ex-Toronto. Sovereign curves have a slight bid to them and mostly across longer maturities. The dollar is slightly softer on a DXY basis primarily against the euro. Oil prices are little changed.

This will be the first of two US CPI prints (8:30amET) before the December 13th FOMC decisions, the other one arriving the day before. There is a large clustering of estimates for core CPI around 0.3% m/m SA with headline at 0.1% m/m as gasoline prices are expected to weigh on the latter. The core estimate may be little more than extrapolative in nature following two months of 0.3% gains after a milder summertime patch. Fed funds futures are pricing no moves at the December and January meetings and the decisions may come down to the batch of data between now and then on jobs and inflation.

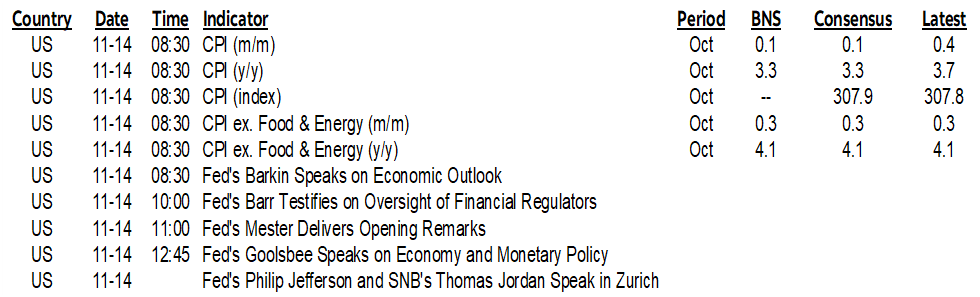

US small business plans to raise prices continue to creep higher in the US. The NFIB’s survey results for October showed that a net 33% of small businesses (emphasize ‘net’) are planning to raise prices over the next three months on a seasonally adjusted basis. That’s the highest reading since last November and the trend is pointed upward going into the peak holiday shopping season (chart 1).

Grossly dysfunctional US politics is back on the radar. A possible House vote on a two-step continuing resolution to fund the government into the new year is expected sometime later today but may not occur if procedural matters thwart the effort. The continuing resolution would fund parts of the government until January 19th and other parts until February 2nd with nothing on funding for wars in Israel and Ukraine. The aim is to avoid a government shutdown when current funding expires on Friday. The mischievous minority in the GOP is seeking to derail the agreement because it doesn’t include spending cuts and stricter immigration controls. Some among the Dems don’t like the two-step feature and absence of war funding. Most probably get that a government shutdown into an election year would be political suicide and particularly for the GOP.

A Bloomberg piece is referencing anonymous folks who are saying that a modest amount of low-cost financing to a segment of the Chinese housing market is in the works. At about US$140B this isn’t shock-and-awe material and the stimulus is aimed at funding on more generous terms that ultimately relies upon buyers taking the bait.

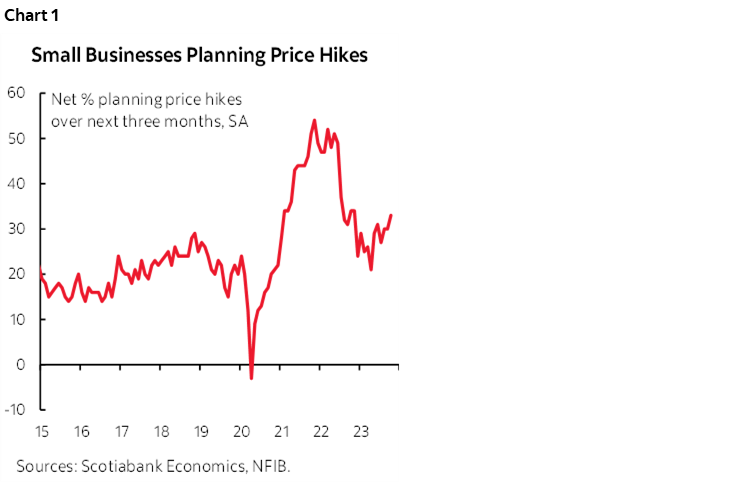

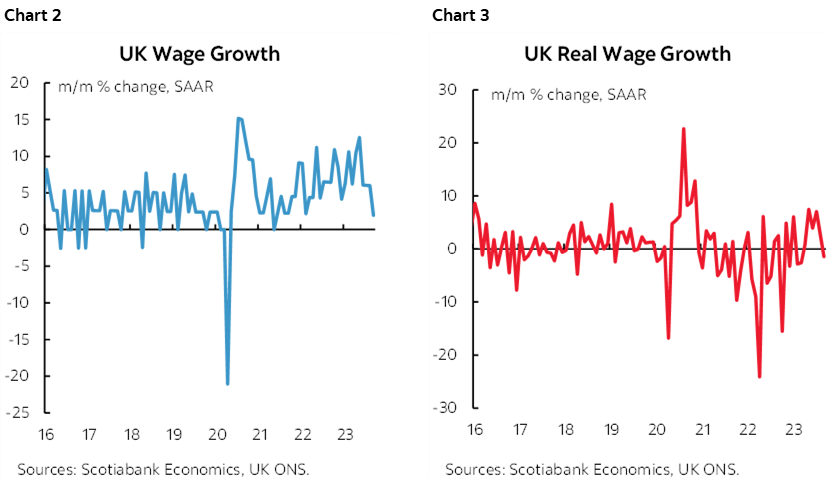

UK job growth picked up a little last month and that added a slight bid to sterling that ignored a sharp deceleration in wage growth. 33k payroll positions were added in October for the second consecutive monthly gain of a similar magnitude following two mild declines (consensus is not meaningful). Jobless claims landed at about 18k and are stuck in a largely sideways trend with mild volatility dating back to late 2022. Wage growth ex-bonuses eased sharply to about 2% m/m SAAR following three months of 6% m/m SAAR gains while marking the coolest gain since May 2021 (chart 2). Real wage growth is back in negative territory for the first time since March using headline CPI (chart 3).

Germany’s ZEW investor sentiment gauge surprised a bit higher by posting the first meaningful gain since early this year after a series of largely sideways moves following the earlier decline. It’s the first of the three main monthly sentiment gauges and may send a positive signal ahead of next week’s PMI and IFO business confidence gauges.

The second swing at Eurozone Q3 GDP was left unrevised at -0.1% q/q this morning. Jobs were up by 0.3% q/q in Q3. Not much to see there on either count.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.