ON DECK FOR WEDNESDAY, MAY 31

KEY POINTS:

- Global sovereign yields dip on soft overnight data, debt ceiling uncertainty

- The debt ceiling agreement almost failed at the committee level…

- …amplifying uncertainty into tonight’s full House vote

- Oil drops as China’s PMIs weaken, adding to sovereign yield dips

- Eurozone headline CPI is looking soft…

- …but reserve some judgement as core will be key

- Canadian GDP the last piece of evidence pre-BoC

- A$, rates shake off upside surprise to Australian CPI

- US ADP, JOLTS on tap

Safe havens are in vogue this morning following a squeaker of a House committee vote on the debt ceiling that amplifies risk into the full vote tonight and after a round of soft Chinese growth and European inflation prints with month-end rebalancing in the mix. Canadian GDP and US job market readings are on tap for the day along with the House vote. If that’s not enough, there is more hawkish Fed-speak to consider (Mester, FT, no “compelling reason” to halt hikes, nonvoting 2023, voting 2024).

The dollar is broadly stronger against all major crosses. Sovereign yields are moving lower across the US, Canada and especially Europe including all maturities. US equity futures are down by ¼%, TSX futures are off by double that and European cash markets are down by up to about ½%. That followed a weak Asian session that saw stocks in Tokyo and HK fall by 1–2% and smaller declines in Seoul and across mainland China’s indices. Oil prices are off by almost 3%.

Here's the round-up of overnight developments:

1. It’s debt ceiling crunch time and the first test has been passed, but just barely. The US House of Representatives Rules Committee passed the debt ceiling deal by a squeaker of a margin (7–6) last evening and the deal now heads to the full House floor for a vote probably at around 8:30pmET. If that passes, it then heads to the Senate perhaps by the weekend. Media commentary pinned the Treasury rally on last evening’s vote but US 2s shook it off when the news hit at about 8:45pmET and rallied later through the overnight session as soft global data was digested.

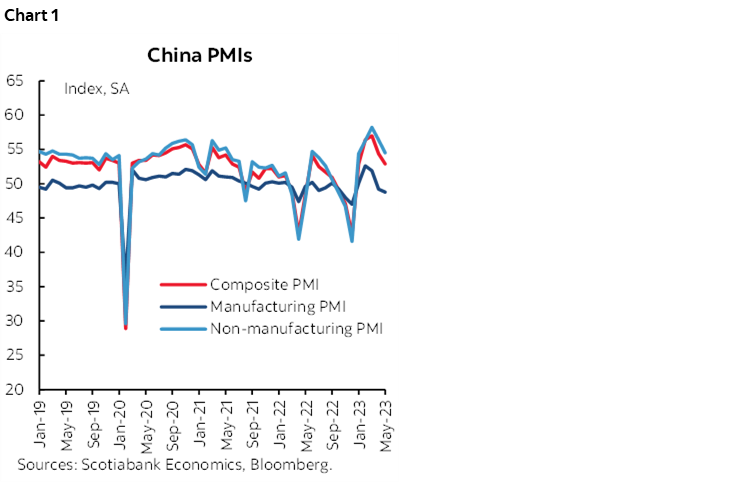

2. China’s PMIs disappointed overnight. The May composite gauge fell 1.5 points to 52.9 mainly because the non-manufacturing PMI fell by 1.9 points to 54.5 but also because of a small drop in the manufacturing PMI to 48.8 from 49.2. Chart 1 shows the readings coming off the initial reopening-driven jump.

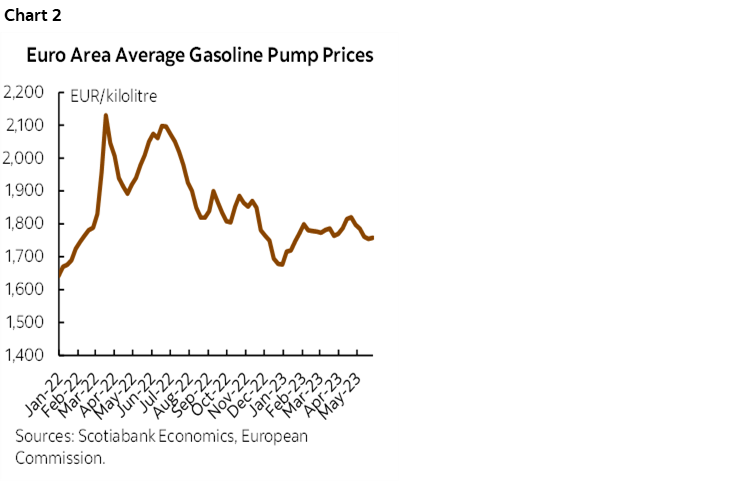

3. Three out of four Eurozone economies are registering softer than expected headline CPI prints ahead of tomorrow’s add-up but there should still be some judgement being reserved until we get the core Eurozone CPI reading. A major reason for this is that energy prices fell in May over April and drove at least some of the weakness across inflation prints (chart 2). Gasoline prices fell by over 2% m/m NSA in May and the CPI prints are all seasonally unadjusted. After Spain landed weaker than expected yesterday, both France and the suite of individual German states followed suit with only Italy surprising higher on total CPI this morning. The German national CPI reading arrives at 8amET, but the 0.2% m/m estimate is now too high in relation to the individual state readings that ranged from -0.3% to +0.1% including three negatives. France’s -0.1% m/m readings was well below the 0.3% consensus but a 3% m/m drop in energy prices played a major role along with a 1.5% drop in fresh food prices as service price inflation remained firm at 0.3%; hence why we need core Eurozone CPI tomorrow to more fully judge underlying price pressures across the monetary union. Italy’s 0.3% was well above consensus (-.2%).

4. Australian CPI surprised higher at 6.8% y/y (6.4% consensus, 6.3% prior). The Australian 2-year yield temporarily shot higher by 3–4bps in the aftermath but much of that reaction was subsequently tamped down as Chinese and European data hit.

On tap into the N.A. session will be the following releases:

1. Canadian GDP (8:30amET): This is the last piece of domestic evidence that the BoC will have to consider before next Wednesday’s decisions, along with external developments like the US debt ceiling deal’s progress.

GDP figures for Q1 plus the months of March and April are due out. Statcan had previously guided Q1 growth at 2.5% q/q SAAR using production-side accounts while the BoC forecast 2.3% q/q SAAR growth using expenditure-based accounts. Statcan had previously guided that March GDP was tracking a small dip of -0.1% m/m based on preliminary evidence. That’s why you see those quarterly and monthly numbers dominating in the incomplete consensus that has missing entries again. I went flat at 0% m/m for March because of a) data since then, b) my simple regression against known variables indicates mild growth, and c) because upward revisions to the initial guidance are not uncommon. For April, my simple model is leaning toward mild growth, but the public sector strikes may dent that somewhat in which case hopefully Statcan will provide an estimate of the strike’s impact or hopefully we can back it out. All of this will also inform early tracking for Q2 GDP growth through the April start and the full Q1 hand-off to the math.

It would likely take a sizeable miss to the BoC’s Q1 2.5% number to matter to next week’s decision and even then it isn’t clear. Details will also matter, such as final domestic demand and the overall composition of growth. April and May data will be dirtied by strikes and wildfires that the BoC may be inclined to look through as transitory effects.

2. US Jobs data starts to arrive today. US ADP payrolls (8:15amET) and JOLTS job openings (10amET) will be the last main macro factors to consider among the other more minor ones listed below. Only fools submit blind estimates for JOLTS, but any surprise to the general downward trend this year that either accelerates or interrupts it could be impactful to markets as they pass the time waiting for Friday’s payrolls. ADP should only matter to nonfarm expectations if there is a big surprise to nonfarm consensus and even then it’s not clear. The consensus guess is 170k and I’m at 200k.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.