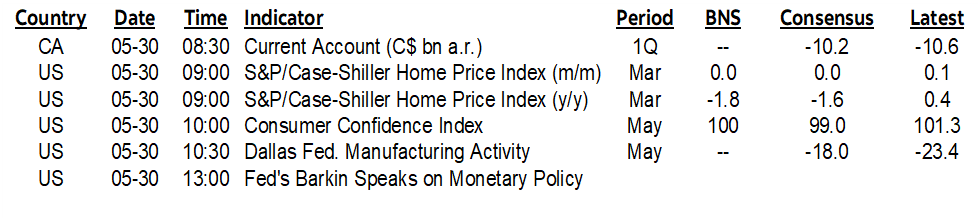

ON DECK FOR TUESDAY, MAY 30

KEY POINTS:

- Three factors are dominating global markets this morning

- EGBs, US Ts rally after Spanish CPI falls short and drones hit Moscow

- Sterling gains, gilts cheapen on surge in shop prices

- US consumer confidence on tap...

- ...as consumers’ inflation expectations remain high

- Alberta’s UCP majority outcome unlikely to alter provincial spreads

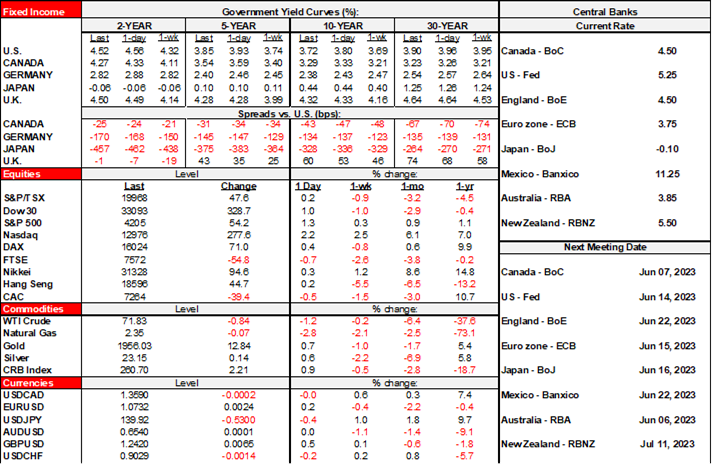

Stocks and bonds are both generally richer into the N.A. session. US Treasury yields are down by 5–7bps across the curve, Canada’s curve is performing similarly to the US at the front-end but underperforming across longer maturities, and yields on EGBs are similarly lower across maturities and countries with slightly cheaper gilts the exception. S&P futures are up by about ½% while the Nasdaq is up by 1¼% and with TSX futures a touch higher amid mixed European cash markets that have London and Paris down by ¼% but other exchanges up by around ½%. The USD is slightly weaker with sterling leading gainers.

US and UK market participants are returning from holidays to monitor debt ceiling developments before tomorrow’s probable vote in the House but yields across EGBs fell as soon as Spanish inflation hit and around the same time that drones hit Moscow and escalated tensions. The two effects spilled over into Treasuries and Canadas.

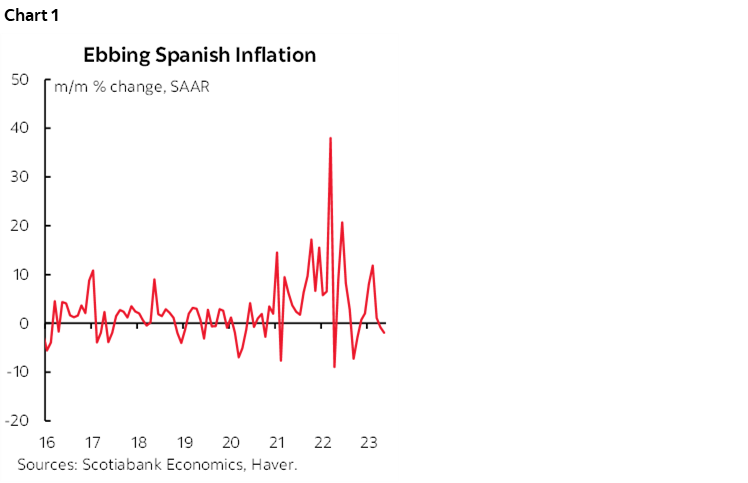

Spanish CPI inflation landed quite a lot softer than expected in May. On an EU Harmonized basis, it fell by -0.2% m/m NSA (consensus +0.2%) with the year-over-year rate ebbing to 2.9% (3.3% consensus, 3.8% prior). Chart 1 shows our seasonally adjusted m/m change and how pressures have ebbed. This is just one country, however, and Germany, France and Italy all report tomorrow before the EU tally on Thursday.

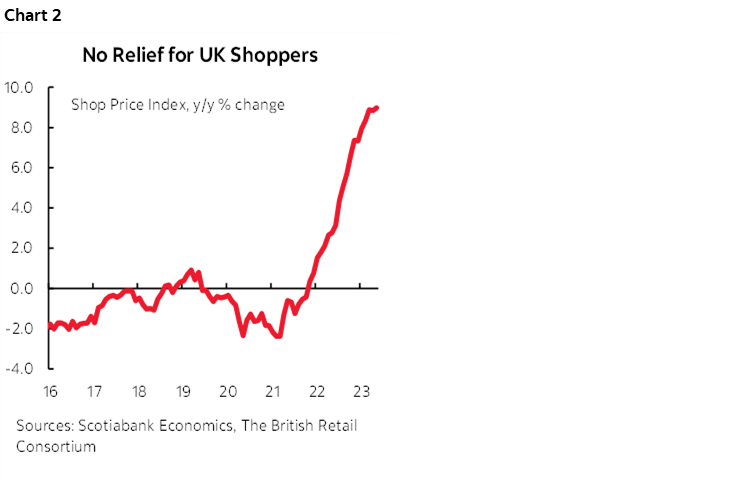

Sterling is outperforming and gilts are cheaper after the British Retail Consortium’s monthly Shop Price Index jumped by 0.5% m/m and that took the year-over-year rate higher to 9%. Both food (15.4% y/y) and non food (5.8% y/y) prices contributed to the acceleration. This measure is not at all ebbing even with year-ago base effects (chart 2).

Alberta’s United Conservative Party won a majority in yesterday’s election and is leading in 49 of 87 ridings with 52.6% of the vote. This is as much a defeat for Trudeau as it is a victory for the UCP that will complicate the Federal Government’s environmental policies. No impact on Alberta spreads is likely given the minimal surprise factor and more important drivers of provincial bond spreads.

On tap into the N.A. session is just US consumer confidence for the month of May (10amET). It could be a tough call given competing effects, but most within consensus expect a mild deterioration (consensus 99 from 101.3, Scotia 100). The prior month’s wage growth picked up and nonfarm payrolls beat expectations to help set the stage for May when gas prices were little changed over April. The S&P spent much of May treading water compared to April when it rebounded from the temporary hit in March that was due to peak concerns around regional bank developments. The 30-year fixed mortgage rate is ending the second half of May a touch higher than during the month of April.

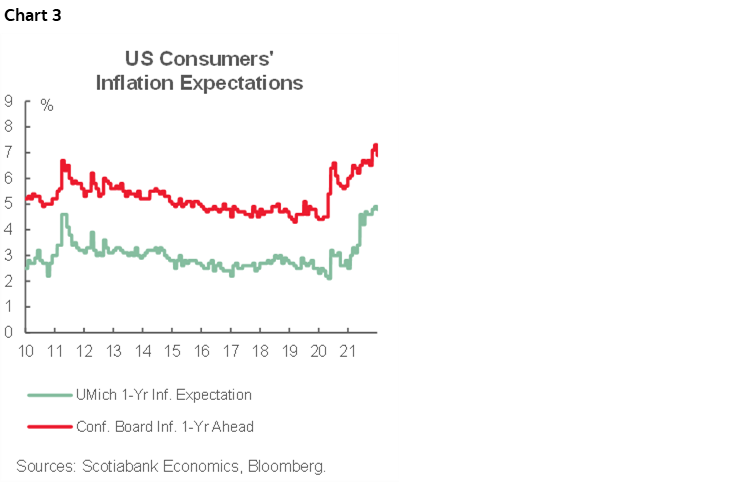

What could also matter is what the confidence survey says about inflation expectations. Chart 3 shows the two measures of 1-year ahead consumer inflation expectations. They are not the greatest gauges, but consumer expectations are not showing signs of relief.

Otherwise, there are only minor gauges due out including US S&P repeat-sales house prices for March that are expected to land flat in m/m terms (9amET) and the Dallas Fed’s manufacturing gauge for May (10:30amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.