ON DECK FOR MONDAY, MAY 29

KEY POINTS:

- Subdued global market reaction to US debt ceiling deal

- US, UK markets shut for holidays

- Albertans head to the polls today

- Turkish lira falls as Erdogan’s ruinous economic policies to continue

- This week’s main focal points

Global market action is subdued given that both the US (Memorial Day) and London (Spring Bank Holiday) are out today. The main driver of a mild risk-on bias is the tentative achievement of a debt ceiling deal that still faces significant hurdles. There are no calendar-based developments to consider.

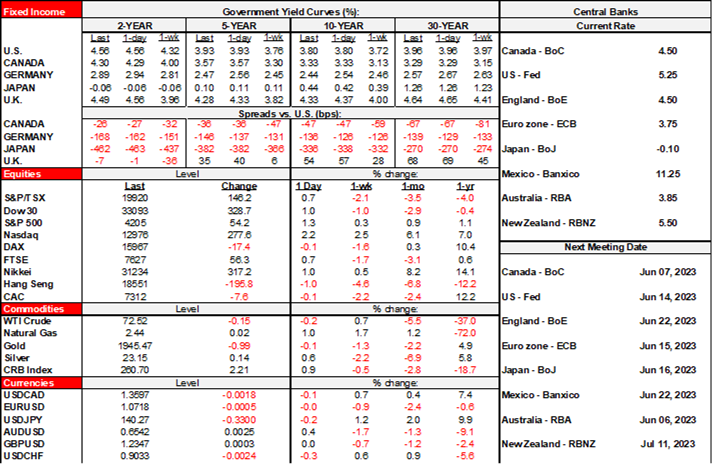

Market reaction to the weekend achievement of a possible debt ceiling deal is quite mild so far. US equity futures are up by about ¼% while TSX futures are flat and European benchmarks are mostly flat. With trading in US Treasuries and gilts out of commission for the day, EGB yields are falling across maturities and countries. The dollar is little changed as gainers including the A$, yen, Swiss franc, CAD and MXN are offset by little changed European crosses.

Why such a subdued reaction to the US debt ceiling deal? It could be because the deal still has to pass votes in the House perhaps on Wednesday, and then the Senate. There could be all manner of antics that get in the way of passing it before Yellen’s revised June 5th deadline. It could also be because a deal reinforces the risk of further Fed tightening. We may also get a clearer reaction when US and UK traders return tomorrow.

Nevertheless, a debt ceiling deal is likely to pass and in a way that meets base case expectations by punting the issues until after the 2024 Presidential election by suspending the ceiling until January 2025 along with spending caps. If passed this week or by early next week, then the issue will have been swept aside in time for all major June central bank meetings including the Fed and BoC decisions.

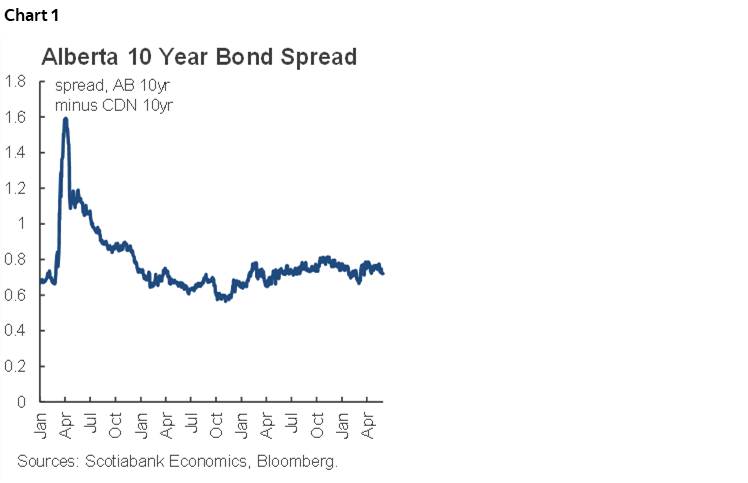

Albertans head to the polls today to choose between granting another term in office to the big-spending incumbent United Conservative Party and its undisciplined leader Danielle Smith or veering to the left-leaning NDP and its leader Rachel Notley. Polls close at 8pmMDT (10pmET). The UCP is leading in the polls with the latest poll indicating the UCP has support of 52% of decided voters versus the NDP at 44% but with about 20% still undecided. When translated into seat projections, the UCP is expected to win a majority with 51 out of 87 seats. Results will begin to become available shortly after polls shut and with about 750k advance voters setting a record. Alberta’s 10-year spread over Canadas has been holding steady throughout the campaign (chart 1).

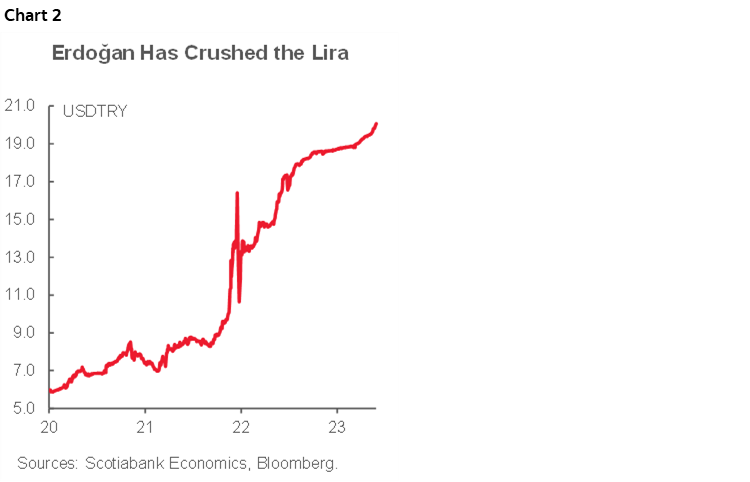

The Turkish lira is depreciating again (chart 2) after Recep Erdoğan won the second-round runoff yesterday to extend his rule along with the era of his ruinous economic policies and his country’s status as a rather two-faced ally. To call it a fair election would be a stretch to say the least. The country faces rising risk of a further currency crisis amid weak investor confidence.

For the week ahead, the main focal points will include monitoring passage of the debt ceiling deal, Friday’s US nonfarm payrolls and wages, Canadian GDP for Q1, March and the preliminary April reading on Wednesday, China’s state PMIs for May tomorrow night, and Eurozone CPI for May on Thursday with country CPI estimates starting the day before.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.