ON DECK FOR FRIDAY, MAY 19

KEY POINTS:

- Global markets cautiously optimistic...

- ...as guidance points to a possible debt ceiling deal this weekend

- Japanese core inflation is surging, adding to BoJ pivot risk

- Why Fed Chair Powell’s appearance today may matter

- Canada to update retail sales for March and April, debatable BoC interpretations

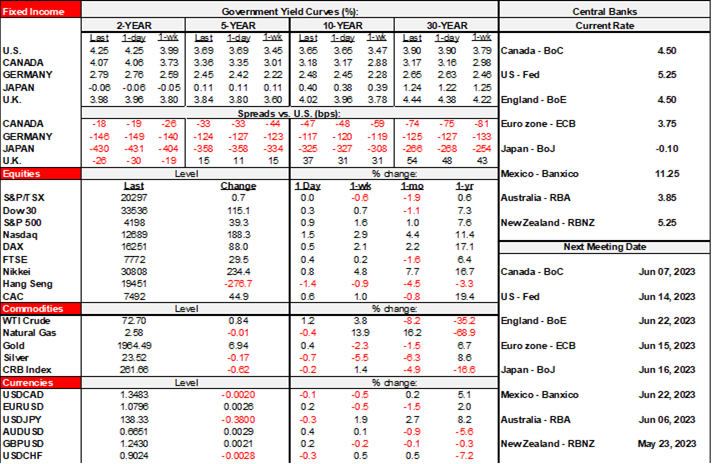

Solid risk-on sentiment is potentially marking an end to the week and there are several key developments to consider. The USD is broadly softer. Stocks are broadly higher including mild gains in N.A. futures plus gains of +/- ½% across European cash markets. US Ts and Canadas are slightly cheaper while gilts and EGBs are headed the other way.

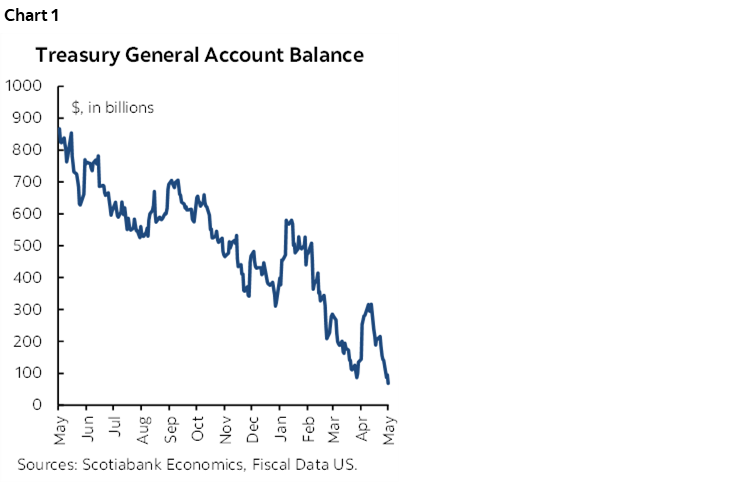

The main catalyst is ongoing enthusiasm that a US debt ceiling deal may be near at hand. House Speaker McCarthy said late yesterday that a deal might be reached by this weekend and a possible vote could be held next week and hence before Yellen’s June 1st deadline. An added catalyst is that the US Treasury’s daily cash position fell again in yesterday’s release to just US$68B (chart 1).

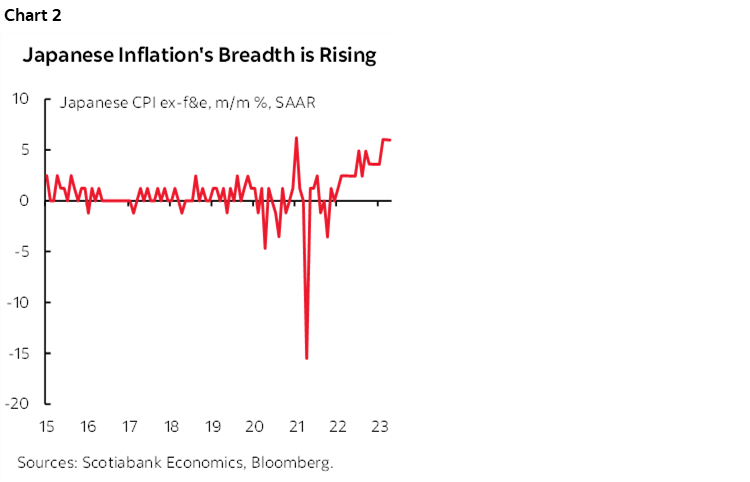

There are increasingly convincing signs that Japanese inflation may motivate a BoJ pivot this year. Japanese CPI accelerated to 3.5% y/y in line with expectations (3.2% prior). Ex-f&e CPI picked up to 4.1% y/y (4.2% consensus, 3.8% prior). More important is that CPI ex-f&e in m/m SA terms was tied with two other months for the hottest increases since a temporary blip in 2014 (chart 2). There is a trend toward rising m/m core CPI SA gains over the past year that indicates that inflation’s breadth is fanning out. Next Thursday’s Tokyo gauge for May will offer a fresher assessment. The implication is that the path to the mid-June BoJ meeting is being marked by reason to upgrade inflation forecasts in the context of ongoing speculation toward a policy pivot at some point.

Fed Chair Powell and former Chair Bernanke appear jointly on a panel at 11amET. In addition to anything Powell may say of relevance to the June 14th decision, there is also a possibility that they share updated views on the natural rate of interest. The occasion is to honour the late Fed economist Thomas Laubach. Laubach is well known in central banking for his work on the natural rate of interest. See the Global Week Ahead for a more detailed discussion of the issues, estimates and possibilities here.

Canada will update retail sales this morning for the month of March and with a preliminary look at April (8:30amET). There may be high revision risk to the preliminary March reading that showed a m/m SA nominal drop of 1.4%. That’s because the 28% sampling rate behind that flash measure was a record low. Hopefully the sampling rate for the preliminary April reading that we’ll also get today will be a tad more impressive.

Canada knocked back pricing for the BoC’s policy rate yesterday in what I think was some folks’ selective hearing toward what the Governor said and confusion over what a stress testing, risk-focused report communicated versus the BoC’s baseline forecast. Journalists talking their PAs blaring the negative stuff absent any balance from the report didn’t help.

Mexico also updates retail sales for March this morning (8amET) and they are expected to be little changed (+0.1% m/m).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.