ON DECK FOR THURSDAY, MAY 18

KEY TOPICS:

- Debt ceiling optimism and jobless benefit fraud drive higher yields

- Why the debt ceiling optimism?

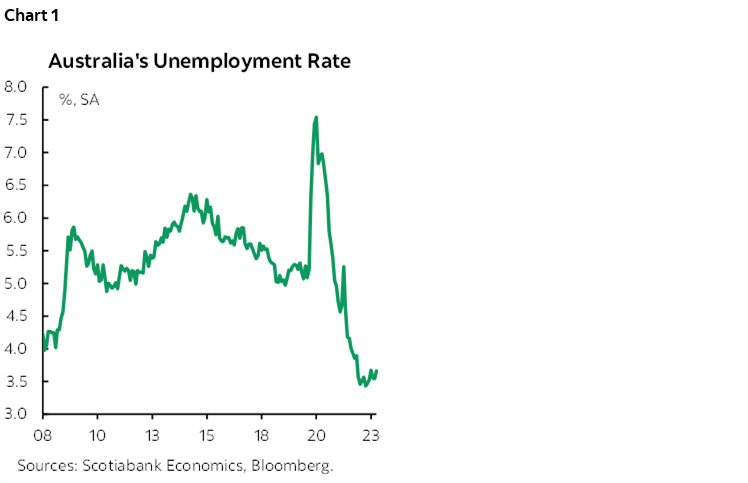

- The fake rise in initial jobless claims

- BoE warns QT pace could pick-up

- BoC’s Macklem can’t divorce stability from monetary policy this time

- Banxico expected to pause

- AU jobs mildly disappoint, rates didn’t care

- NZ budget adds to curve pressures

- Chile’s economy probably accelerated in Q1

The prime catalysts to global market movements are optimism around striking a deal on the US debt ceiling and fresh speculation that the recent rise in US initial jobless claims has been a mirage (see below for both). There are regional variations around these points through the overnight session into today.

Stocks are rallying across most markets with the exception of slight softness in TSX futures perhaps due to soft oil prices and BoC speculation. Sovereign debt curves are cheaper across European markets as they react to yesterday’s sell-off in US Ts on debt ceiling optimism. US Ts are also mildly cheaper while Canada’s curve continues to underperform as BoC risks are being fundamentally reassessed. The USD is broadly stronger but with the won, yen, NZ$ and CAD somewhat holding their own.

At issue is that if a debt ceiling solution lies at hand in such fashion as to possibly remove a major near-term source of uncertainty, then the trade-off may be greater conviction for the FOMC to hike again as members openly debate their stances and with key data still between now and the June 14th decision. Optimism around the debt ceiling has increased because a) Treasury’s cash position has diminished more rapidly than expected to just US$85B as we monitor daily updates, and b) that strengthens the validity of Yellen’s guidance that June 1st or so may truly be the effective x-date after which technical default on US government obligations becomes a bigger risk, and because c) all of this is motivating a more serious attempt toward getting a deal done in the nearer team with the ‘A-team’ of negotiators taking over as both sides speak more optimistically.

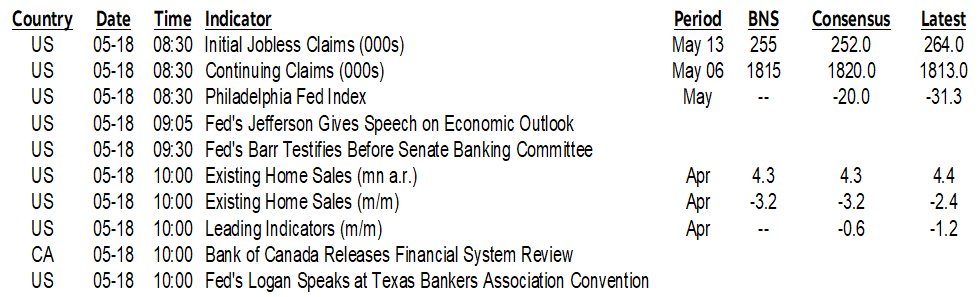

Australian jobs mildly disappointed expectations (-4.3k, +25k consensus) with a small upward revision to the prior month (61.1k from 53k). That was enough to push the unemployment rate up a couple of tenths to 3.7% (chart 1). The details were weak as full-time employment fell 27k but with a 10k upward revision to 83k the prior month. Part-time jobs were up by 23k with a slight negative revision to -21k. The Australian two-year yield fell by about 7bps initially but then fully reversed that reaction as the overnight session continued and wound up about 10bps higher on the day. There were also other developments such as the spillover effects of US debt ceiling optimism from yesterday’s N.A. session, speculation that the RBA may begin actively selling bonds later in the year and that China will begin importing Australian timber again.

New Zealand’s rates curve cheapened by 17bps in 2s and less than that further up the curve as the Budget contributed to other pressures such as debt ceiling spillover effects and ongoing reassessment of RBNZ prospects. The Budget dropped a recession forecast, increased debt issuance by NZ$20B over the next four years, and increased spending while shifting to forecast deficits through to 2026 as the October election approaches.

BoE Deputy Governor Ramsden remarked this morning that “There’s the potential for us to go up a little bit. I don’t see us going down given the experience of the first year.” This was in reference to the current pace of unwinding holdings of gilts that is set at £20B each quarter.

On tap today are the following developments:

1. Banxico is expected to hold its overnight rate at 11.25% this afternoon according to 19 of 24 within consensus (2pmET). Scotia’s Mexico City-based economist Eduardo Suarez is in the hold camp. Ed’s a super experienced economist with great connections on the ground. A minority of 5 economists expect a hike. Part of what they do will depend upon how convinced they are that core inflation is durably ebbing lower and part of it may depend upon the peso connection to their assessment of what the Fed's next steps may be as mild optimism around the debt ceiling has crept back into markets.

2. BoC Governor Macklem makes an appearance to deliver the Financial System Review when it is published at 10amET and when he hosts a press conference at 11amET. Expect a lot of references to housing, mortgages, other aspects of the stability part of the picture. I’d be surprised if they don’t try to walk down the middle on housing/mortgages by saying there are further lagging rate effects on payments for the tail of the most strained mortgages, but at the same time acknowledge that the market is heating up again. In my opinion they should be more incrementally concerned about evidence that the housing market is overheating once more. The BoC was uncomfortable toward hiking just because of housing in the past while inflation was low, but today offers a dangerous and destabilizing combination of the two that requires a monetary policy response. In my personal opinion, there is a need to respond quickly without further delay and 25bps is just a down payment on possible hikes while OSFI stands ready. In the past, Macklem has tended to say he won’t address monetary policy considerations during this presser and prefers to focus upon stability issues. That’s a little tougher to do this time! First, the two are interacting with one another. Second, the speed of recent adjustments in market pricing, inflation and housing may merit a comment on monpol. Stay tuned. In my opinion, Macklem must drop this convention with the June meeting approaching and offer fresh comments on monetary policy risks.

3. Is the rise in US jobless claims a hoax as another update beckons (8:30amET)? We’ll get another update this morning and at issue is whether the prior week’s increase builds upon itself and into the nonfarm reference period for May. Note the debate over the recent rise in initial claims and its concentration upon the single state of Massachusetts (chart 2). That has spawned concern that fraudulent claims in that state account for the rise in total claims. The Massachusetts Department of Unemployment Assistance has openly stated it “is experiencing an increase in fraudulent claim activities where people attempt to gain access to active UI accounts or file new UI claims using stolen personal information so they can fraudulently obtain unemployment benefits.”

The US will also update existing home sales that are expected to weaken in lagging response to what we know about pending home sales (10amET).

4. Chile’s economy is expected to post the quickest growth in 2023Q1 since 2021Q4 after last year was basically a write-off (8:30amET). Meh. It’s Q1.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.