ON DECK FOR WEDNESDAY, MAY 17

KEY POINTS:

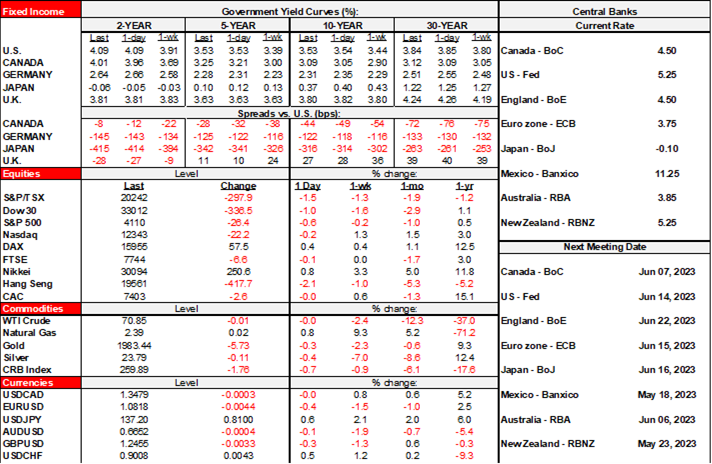

- Canadian rates continue to underperform, CAD outperforming

- BoC myths

- Australian wage growth remains hot

- Japan’s economy doubled expectations

- US housing supply remains very tight...

- ...as the then-and-now real estate alarms are greatly exaggerated

- Quiet N.A. calendar

It’s a very light morning in term of fresh developments. Stocks are mixed with N.A. futures a little higher and European cash markets unchanged on balance. Sovereign bonds are slightly richer across most markets except for Canadian and Antipodean curves including the effects of Canadian CPI on local markets (recap here). The USD is a touch firmer against most majors with the only exceptions being the NZ$, won, CAD and the A$. Overnight developments were very light and there is nothing notable on tap into the N.A. session.

That places ongoing attention upon debt ceiling talks. The main players tried to sound optimistic yesterday as it was pretty obvious that they all agreed to do so at least publicly. We’ll see, but a deal is likely to remain elusive until the Hollywood actors running Congress decide that market pressures and tough choices are staring them in the face. Biden leaves for Asia today but has truncated his trip while leaving negotiations in the hands of others. McCarthy came out of yesterday’s meeting and sounded relatively upbeat for him when he said "We've got a lot of work to do. It is possible to get a deal by the end of the week. It's not that difficult to get to an agreement."

Australian wage growth in Q1 was unchanged from the prior quarter’s 0.8% q/q SA (consensus 0.9%), or 3.4% q/q SAAR. The recent peak was 4.3% in 2009Q3. The trend is still hotter than the roughly 2% readings we were getting from about 2014 through 2022H1 and so wage growth has indeed accelerated notwithstanding the fact that the second derivative has not (chart 1). The Australian front-end richened a touch after the release but still wound up cheaper for the session as a whole.

Japan’s economy grew faster than expected in Q1 with GDP up by 0.4% q/q SA non-annualized (0.2% consensus). Markets didn’t really care. The main drivers of the beat were consumption that grew by 0.6% (0.4% consensus) and business spending that was up 0.9% q/q (-0.3% consensus).

US housing starts were up 2.2% m/m in April but only because the prior month was revised down to a 4.5% m/m drop instead of –0.8%. Building permits were down 1.5% m/m but here it’s the opposite in the sense that the prior month was revised up from –8.8% m/m to –3%. Not great either way. The US has the same tight housing supply as Canada. In the US, there is soft building activity and months of new homes under construction sit at just 2.8 while months supply of resale homes is just 2.6. Both continue to hover around record lows and vastly lower than into the GFC when both supply measures punched into the double digits. This is an important consideration against the fact that at the time of the GFC the real estate problems were vastly greater versus today when they are largely confined to the office property markets and not in all cities. Housing and commercial real estate ex-offices are vastly healthier than past real estate shocks such that I find much of the current real estate narrative is lacking balance.

Canadian markets will continue to debate rate hikes. Further to my note yesterday is the topic of June versus July. I wouldn’t overstate the argument that the BoC needs an MPR and presser in July to hike or Macklem to speak. They could easily go in June with two points to back that up:

a) recall they surprised markets 3 of 8 decisions last year. They couldn’t care less about what markets and the street expect and I swear they wear that as a bit of a mischievous badge of honour, and

b) even if they do think they need to set it up then they can easily point to everything they said in the April statement, MPR, press conference, his IMF media roundtable and his two rounds of parliamentary testimony. His line could very easily be that I told you I'd hike if we're surprised. And my, what a surprise CPI and housing have been to them!

And on the bias, they don’t need full communications as the BoC can simply repeat the line from the April statement that said:

"Governing Council continues to assess whether monetary policy is sufficiently restrictive to relieve price pressures and remains prepared to raise the policy rate further if needed to return inflation to the 2% target."

Lastly, there is the debate over crushing it now versus hanging out higher for longer. The way I settle that is by portraying the challenge of getting inflation under control as a race against the clock. The longer that consumers, businesses, governments and markets see core inflation being persistent if not reaccelerating, the less confidence they have that the BoC will ever achieve its 2% inflation target. It has already gone on too long. We already have survey-based evidence of that from the BoC’s twin consumer and business surveys plus recent collective bargaining agreements that show no one really believes in 2% for years to come. If the BoC doesn’t adopt the crush it, killer mentality, then it may never succeed in getting inflation down to 2%. A pledge to hang out high for longer doesn’t address this problem and nobody would believe it anyway given a heavy discount attached to forecast credibility the further out in time we go.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.