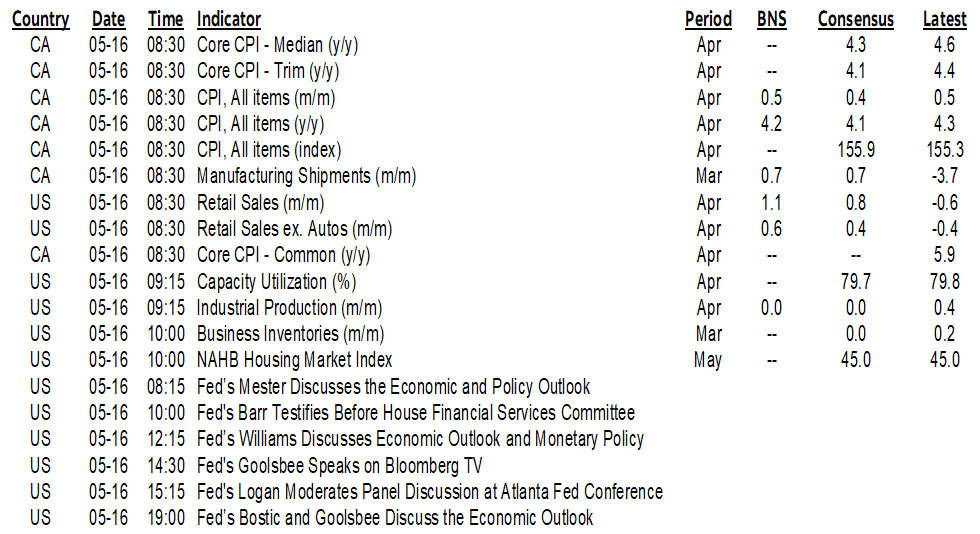

ON DECK FOR TUESDAY, MAY 16

KEY POINTS:

- Markets cautious amid a global data dump, ahead of another debt ceiling meeting

- Is CDN core CPI still hot as housing rips higher?

- US retail sales to spring back to life

- NZ rates curve jumps on RBNZ expectations…

- …that offer a parallel to the BoC

- Chinese retail sales post the second weakest April on record...

- ...but that followed one of the strongest months of March on record

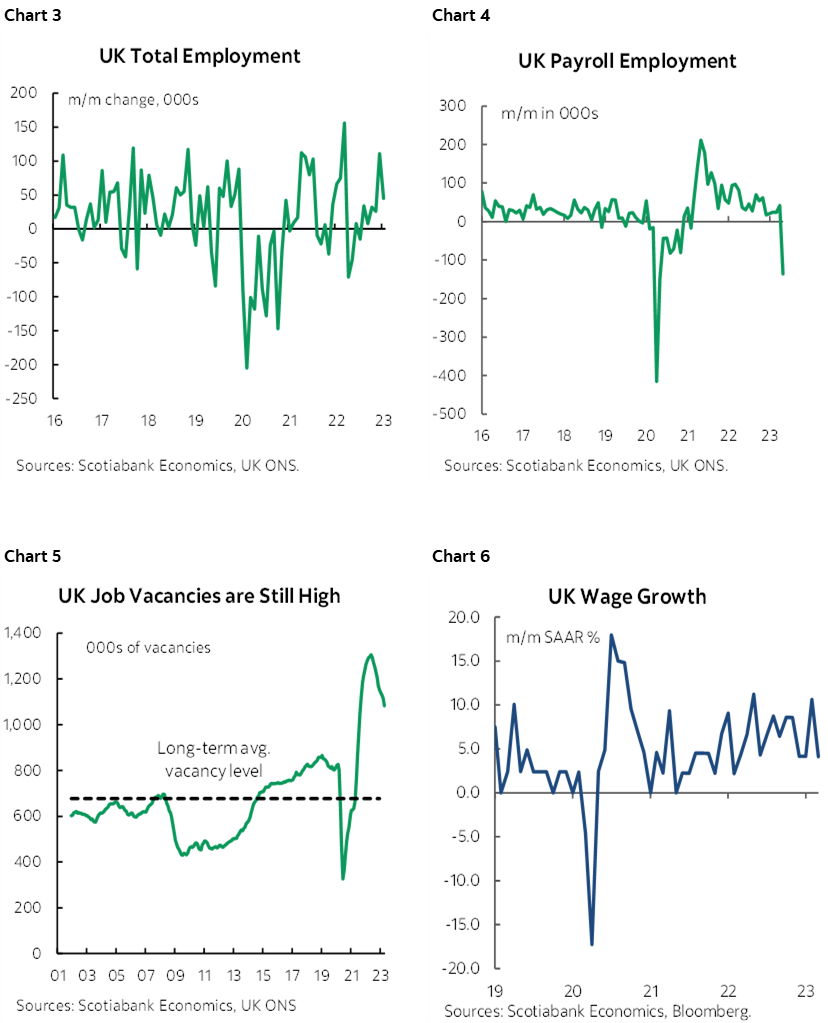

- Gilts react to UK payrolls, ignoring other job readings

- Another fruitless US debt ceiling meeting?

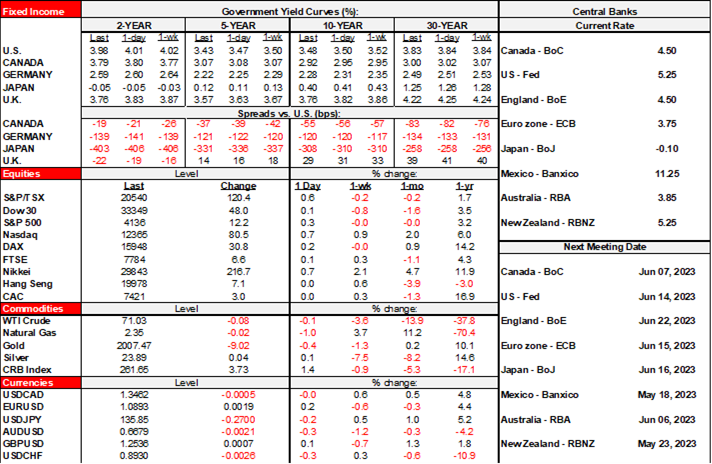

Global markets are playing a bit of defence this morning in between rounds of global macro data and earnings. Sovereign yields are lower across most markets except for NZ that offers a parallel to Canada (see below). Stocks are little changed across most markets. The currency winners are havens like the CHF and yen plus the NZ$ (same point, see below).

One culprit is that Chinese macro data was disappointing especially when looked at properly. Retail sales fell by 7.8% m/m NSA which makes this April the second worst month of April so far this century and second only to last April’s m/m reading when lockdowns were in place (chart 1). Bear in mind, however, that March’s seasonally unadjusted decline was the softest in years (chart 2); in other words, April weakened partly because this year’s reopening-driven surge in Q1 was so strong. Year-over-year changes are more commonly cited and they were up by less than consensus expected at 18.4% (21.9% consensus), although that doesn’t give us a proper sense of the lost momentum. Industrial output was up by only 5.6% y/y (3.9% prior, 10.9% consensus) despite the weak comparator of a year-ago during lockdowns. The jobless rate fell a tenth to 5.2%. Calls for stimulus face the same hurdle—the risk of destabilizing the yuan, Chinese equities and the banking system given the wall of savings that would face a decline in purchasing power. To that effect, the onshore and offshore yuan exchange rates are inching toward the 7 mark to the buck.

UK yields are outperforming this morning after a bunch of job market readings. The UK created 45k jobs in March (chart 3) but lost 136k payroll jobs in April (chart 4) for the first drop in that part of the job market since April 2021. Whether this is the start of a trend or just a temporary reaction to developments across global banks requires more data. Nevertheless there is still a lot of pent-up hiring appetite operating in the background as job vacancies remain high at just over 1 million but fell by 31k in April and are 223k below the peak back in May of last year (chart 5). Wage growth was 4.1% m/m SAAR which returns the figures to the still-hot pace over the two months prior to February’s gain of over 10% (chart 6). Overall, it’s premature to react to the payroll number as the start of something bad in the context of the full suite of evidence and the need for further evidence.

The first of the monthly European sentiment gauges fell. Germany’s ZEW measure declined to -10.7 from 4.1 in terms of the expectations component while the current situation reading slipped to -34.8 from -32.5. The Eurozone’s ZEW fell to -9.1 from +6.4. PMIs and IFO are due next week.

The kiwi curve is the underperforming outlier as 2s cheapened by 11bps overnight and the whole curve cheapened. As near as I can tell, a culprit was a local shop’s forecast for a 6% RBNZ cash rate (presently 5.25%) partly due to a surge of demand driven by higher immigration. I mention this because it offers a parallel to Canada where immigration is exploding. I strongly disagree with the BoC’s spin that this adds to demand driven inflation but subtracts through supply-driven effects on the labour market.

On tap into the N.A. session will be the following:

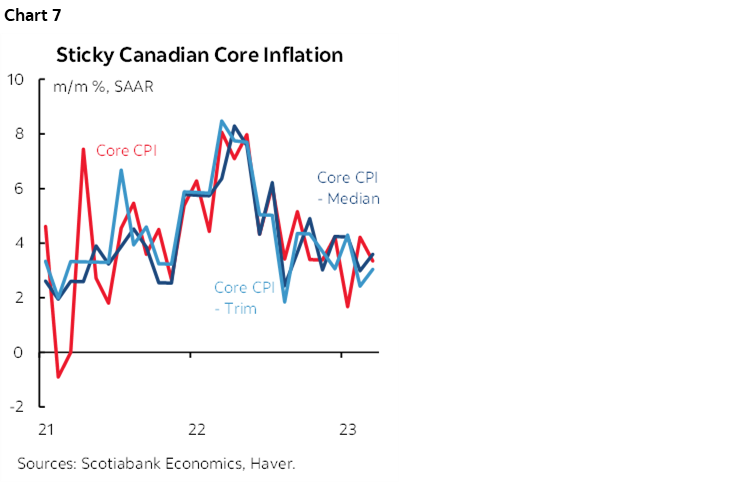

1. Canadian CPI (8:30amET): Estimates range from 0.3–0.7% m/m NSA for headline CPI. Without knowing consensus in advance, my 0.5% NSA estimate matches the median and would translate into a similar SA gain given no real seasonality in April. For traditional core CPI ex-f&e I’m at 0.2–0.3% m/m SA. Key will be trimmed mean and weighted median in m/m SAAR terms. All three measures of core have been sticky at 3-handled m/m % SAAR rates of increase for a while now (chart 7).

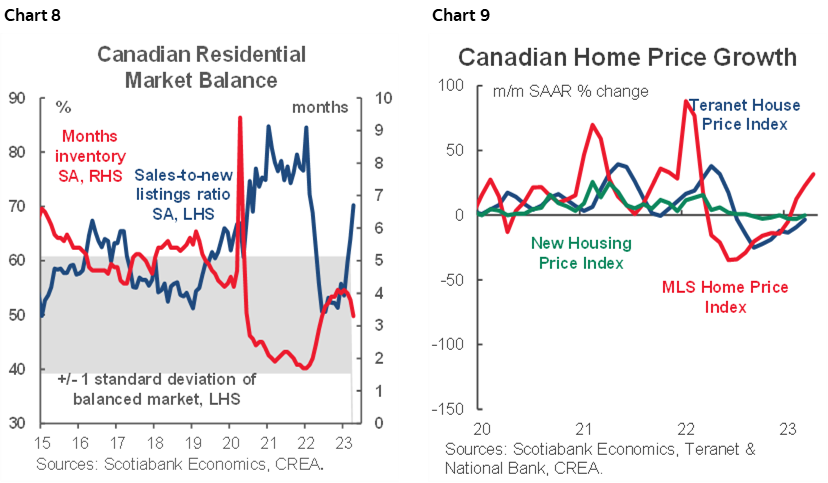

Does this CPI reading matter to the BoC? Yes and no. If the core m/m SAAR gauges are hot, then it fans the possibility of additional near-term hikes. If they are not, then it’s just one month and we still face what I have argued to be an inflection point toward higher forward-looking inflation risk that the BoC should respond to. An important point is that we’re now seeing the housing data that I’ve been warning about since last year as a strong rebound is underway and fed by multiple drivers (charts 8, 9). Housing has been pushed deeply into net sellers’ territory again and this is reigniting price pressures that will spillover into CPI both directly and indirectly through the lift effect on other components.

2. US retail sales (8:30amET): Remember the gloom the last time around? How US consumer wilting? Yeah, not so much. Headline should be quite strong this time given what we already know about autos and gas plus the more retail-oriented parts of CPI. 26 of us out of 67 in consensus expect a gain of 1%+ m/m. Key will be core sales. What may also add upside is that retail sales were revised up from the initial reading for March that showed a 1% m/m drop that is now a smaller 0.6% decline. The US also updates industrial production during April that is expected to be little changed (9:15amET) and another wave of Fed-speak lies ahead today.

3. Debt ceiling: Another fruitless meeting? Perhaps. More like probably. Biden and McCarthy and the whole supporting cast meet this afternoon at 3pmET. McCarthy douse Biden’s weekend optimism yesterday afternoon when he said there wasn’t any progress.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.