ON DECK FOR THURSDAY, MAY 11

KEY POINTS:

- Cautious markets drive stronger USD, lower sovereign yields

- BoE hikes 25bps, guides more to come, as markets offered little reaction

- Chinese credit expansion slows

- Chinese inflation strays further beneath the PBoC’s target

- Trump is a reckless downgrade threat

- US producer prices may rebound

- US initial claims still rangebound?

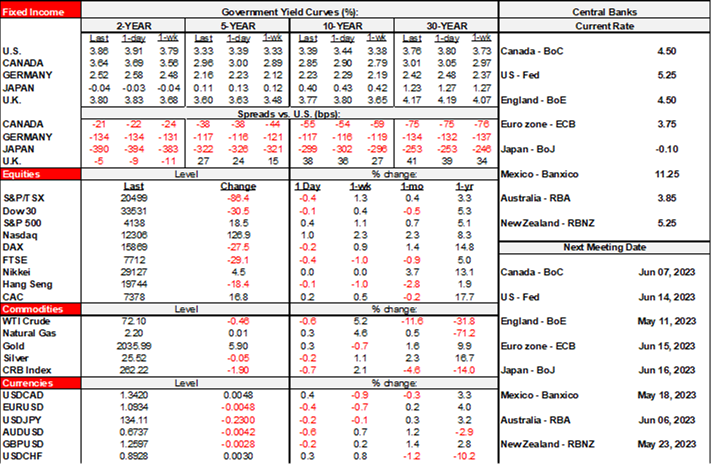

Global risk appetite is mixed across asset classes. Equities are mixed with US and Canadian futures little changed along with the average across European cash markets. The USD is gaining against all major crosses. Sovereign yields are mildly rallying across major markets including the UK where the gilts front-end only gave up a mild amount of its rally post-BoE. Chinese data for April added to weakening concerns after a robust start to the year. Another US inflation gauge is on tap and Trump proved for the millionth time that he’s thoroughly unfit to run anything more than an ice cream truck.

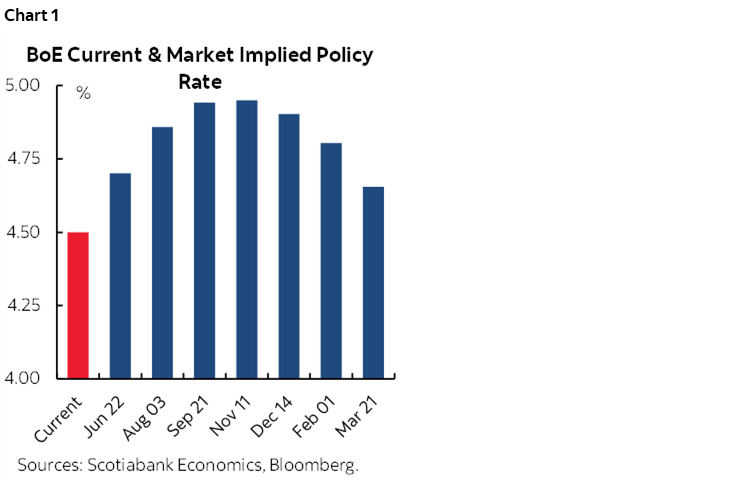

The Bank of England delivered a mildly hawkish surprise this morning as this note is being published through Governor Bailey’s ongoing press conference. The expected +25bps hike to a new policy rate of 4.5% was delivered. There was no change to QT guidance. Growth was upgraded by removing the previously forecast recession and eliminating any negative quarters for GDP growth and the inflation forecast was also raised. That monetary policy is fighting fiscal policy’s influences upon inflation was made clearer by upgrading the fiscal policy contribution to growth to 0.5% this year from 0.3% after Sunak’s earlier budget. There were two dovish dissenters who preferred no change today. Markets continue to price a higher terminal rate (chart 1).

Chinese inflation ebbed by a little more than expected and is practically nonexistent. CPI was up 0.1% y/y in April (0.3% consensus) which takes the reading back toward the lows that were being registered in early 2021. Core CPI was unchanged at 0.7% y/y. Producer prices fell 3.6% y/y largely due to already known oil price and other generally soft prices.

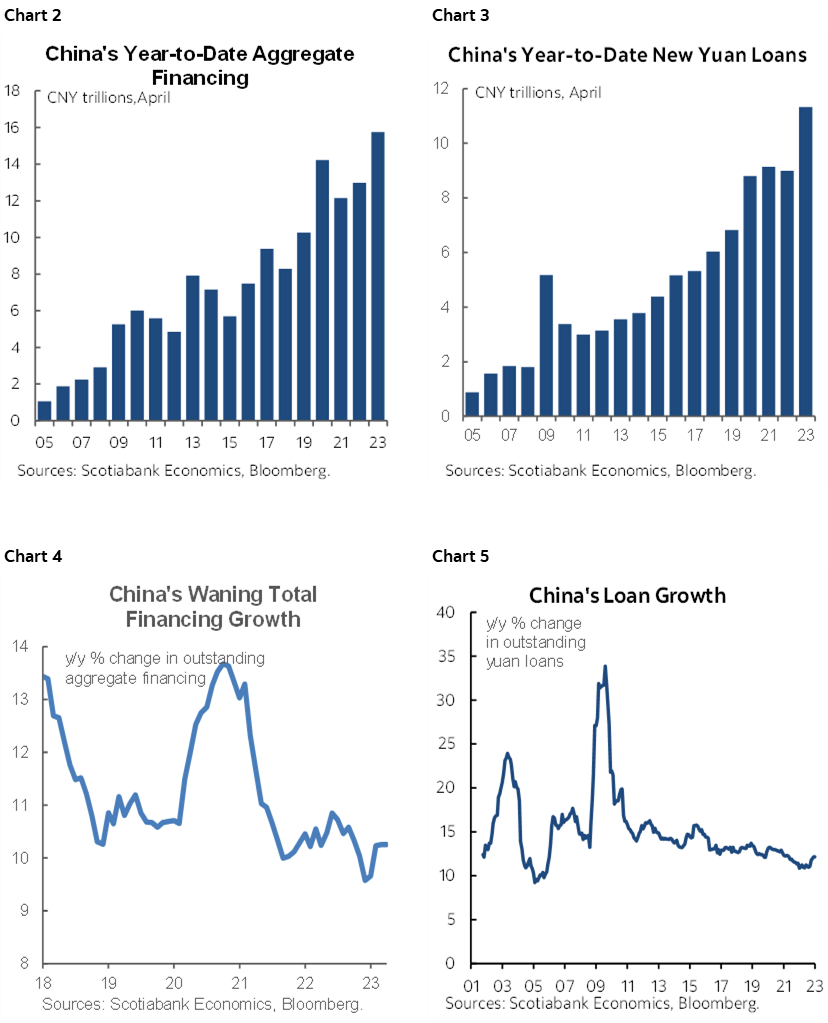

China also updated monthly financing figures for April that fell well shy of expectations. Aggregate financing was up 1.2 trillion yuan (2T consensus) and new yuan loans grew by 719B (1.4T consensus). This follows rapid Q1 growth as China pursued credit easing over monetary easing given yuan stability concerns. Year-to-date financing figures remain very strong because of the Q1 start (charts 2 and 3), but this is having relatively little effect on the year-over-year growth in outstandings (charts 4, 5).

As a result, while the gilts front-end is still slightly dearer on the day, the post-statement reaction saw the 2s yield rise by a modest 5bps and sterling is still weaker to the dollar on the day but by less than before the statement.

US core producer prices are forecast to rebound from the prior month’s -0.1% dip. I’m a little higher than consensus at +0.3% m/m SA nonannualized. Initial jobless claims have been stuck in a 230–250k range since early March as they slightly picked up from the prior 200–220k pace. They have not materially changed between April & May nonfarm reference periods.

And icymi, Trump did indeed say in last evening’s CNN town hall with a grossly outmatched and inexperienced “moderator” that the US should default if the GOP cannot secure major spending cuts in the debt ceiling dispute. He said it would only result in “a bad week, or a bad day” and that the issue is just “psychological.” That will egg on the minority in the House who set a lower recall bar on Speaker McCarthy’s performance. Granted, Trump’s just a bag of wind on any given issue. Still, he’s an instant downgrade threat if elected in 2024 due to the threat that he poses to debt markets and the entire institutional framework. So, add default risk to a list that includes protectionist, seditionist, sore loser, fiscally liberal, science-bashing, Putin-loving, lying, Constitution-hating, misogynist among many other flaws.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.