ON DECK FOR WEDNESDAY, MARCH 29

KEY POINTS:

- Risk-on bias perhaps aided by PBoC liquidity injections

- Macroeconomic costs and consequences to Canada’s divisive inclusive budget

- BoC speech on market liquidity measures today...

- ...may just be a history lesson...

- ...but watch for guidance as bond market supports fall while issuance soars

Risk-on sentiment is driving equities higher this morning amid uncertain catalysts. Liquidity injections by the PBoC don’t hurt I suppose but overall calendar-based developments are super light. US equity futures are up by almost 1% with TSX futures up by a little less and European cash markets roughly 1% higher. The dollar is a touch firmer along with MXN, CAD (expansionary budget, see below) and some European crosses. Sovereign yields are higher across the board.

Overnight markets only saw the Bank of Thailand hike by 25bps as expected and the PBoC inject another 133B yuan of liquidity with overnight repo falling by 25bps.

On tap for today will be light US data and a BoC speech that I’ll elaborate upon.

BoC Speech on Market Liquidity

One of the Bank of Canada’s Deputy Governors, Toni Gravelle, will deliver a speech with contents available at 12:30pmET today. His speech title is ‘market liquidity measures taken during COVID.’ There will be audience Q&A, but no press conference. It may just be a history lesson in which case what’s the point? If there is anything of use in a more forward-looking sense, then it might be if Gravelle speaks to future intentions around balance sheet management including QT and liquidity provisions. This is conjecture on my part since we have no indication of the actual content of the speech, but when the BoC was preparing to back away from QE in a shift to a short period of reinvestment followed by QT with no roll-off caps it was Gravelle who gave the initial speech ahead of the Governor.

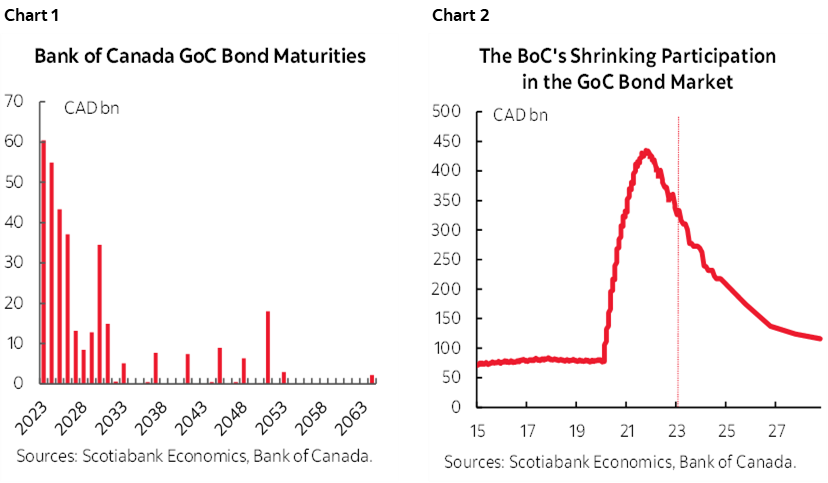

Chart 1 shows the profile of maturing Government of Canada bond holdings at the BoC by year. Chart 2 shows the projected path of BoC holdings of GoC bonds as these bonds mature with zero reinvestment under present BoC policy.

The BoC has about C$60B more of GoC bonds maturing off its balance sheet this year ($88.5B including ones that have already matured in 2023) and then another $55B next year, $43B in 2025 etc.

The holdings remain very elevated. GoC bond holdings peaked at about $435B in late 2021 and now stand at $333B versus the pre-pandemic norm of about $80B. In other words, the balance sheet is still bloated but as Ottawa delivers deficits to spend with reckless abandon, the BoC will be backing away with almost half of its holdings maturing in the next 3 years. With the kind of profligacy that permeates Ottawa’s fiscal bias I would prefer to see outright sales and for the BoC to get out of the bond holding racket even faster, but that’s wishful thinking amid present concerns about liquidity.

The flip side to falling GoC bond holdings is, in part, reflected by falling deposits of members of Payments Canada at the BoC. They have fallen from C$394B in March 2021 to about $183B now and from $0 pre-pandemic which indicates ongoing high levels.

This background leads to two main questions. First, for how long might the BoC continue to allow full roll-off? Or will it eventually taper roll-off plans and treat QT as malleable in the face of liquidity pressures that are significant but in the context of markets that are still functioning? Probably not, at least not for a while. Does the BoC have a target in mind for optimal Payments Canada member deposits in the system that is an analog to speculation toward the Fed’s ample reserves framework? I doubt very much that we will get answers to these questions notwithstanding their importance and have low expectations that the speech will be much more than a confidence boosting message that the BoC has been there to provide liquidity and keep markets operational and will be there as needed in current and future circumstances. But we’ll see. The absence of a press conference to explain anything that is said further diminishes expectations.

Budget Aftermath

The speech’s timing is nevertheless a bit awkward. Enter the Budget’s aftermath. Greater than expected deficits and issuance of bills and bonds as the BoC foists its holdings of GoC bonds back onto the market will make for more challenging issuance conditions going forward. That may not be apparent at present as safehaven seeking amid recent turmoil and the pending US debt ceiling fight are influencing sovereign yields around the world. At some point over the Budget’s projection horizon we are nevertheless likely to see the return of less favourable issuance conditions for all of the debt that Ottawa and the provinces will be heaping onto markets.

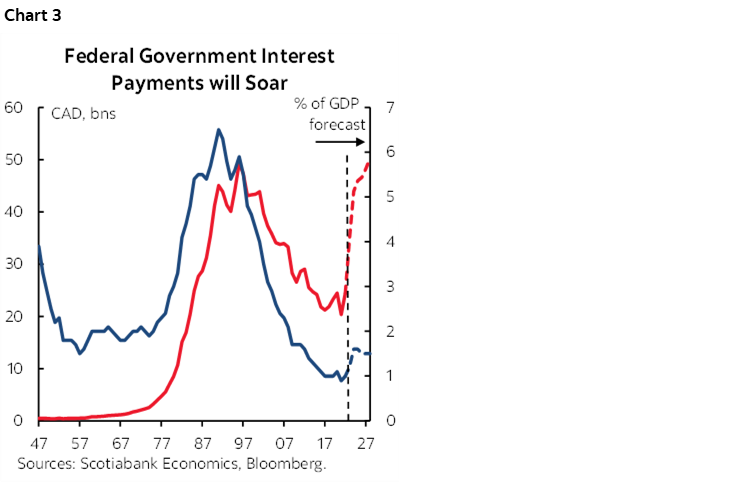

Chart 3 shows one of the consequences to all of this debt. Interest payments on the debt may continue to be low and much lower than the past as a share of nominal GDP projections that assume away a downturn. Nevertheless, the absolute level of interest payments on the debt is projected to rise to 1990s levels at about $50B per year. That equates to about 10% of program spending and 9% of revenues. That is not something to ignore. It is not spending you can suddenly reverse if/when the needs arises; you’re stuck with it and it feeds upon itself. $50B per year and a quarter trillion every five years just to pay interest on debt is a cost to years of the Trudeau government’s deficit-financed pump priming during good times in the economy, let alone what may happen if things skid off into the ditch. It means less money to give back to taxpayers or to apply toward debt reduction in an alternative state of the universe versus present realities, or that much less money to spend on more impactful things. It makes the country increasingly vulnerable to future bond market conditions.

And make no mistake that Ottawa is very much about big government getting bigger. More invasive. More intrusive in all facets of our lives. Cumulative deficits over the next five years amount to $161 billion which blew away the PBO’s estimate of $140B going into the budget for a 15% forecast miss. There is no longer even a useless future placeholder showing a return to balance as years and years of deficits are being piled on. The risk is toward even bigger deficits if GDP performs worse than expected versus the Budget’s use of stale forecasts from February (before recent turmoil) and that project no contraction. Ever. Hallelujah, it’s a miracle! If targeted cost savings fail to materialize, then that too could add to the deficit and I’ll believe Ottawa’s promise to spend less on consultants when I see it. And if the NDP’s ongoing demands for a national pharmacare program resurface in future as another condition of support for the Libs then deficits will explode by even more.

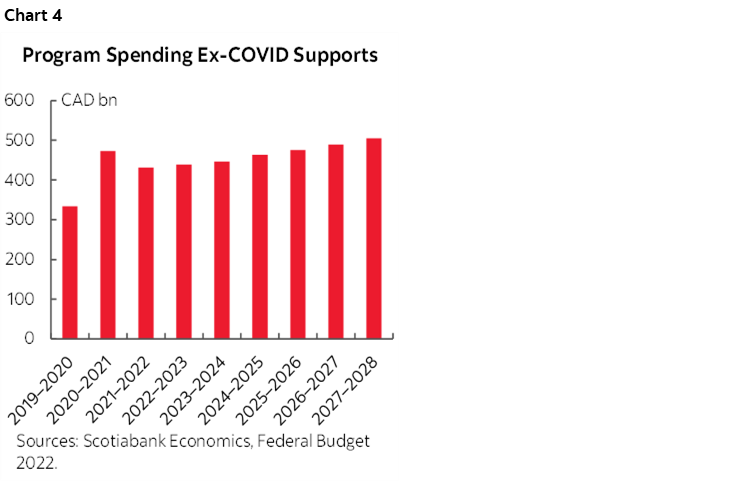

Key is program spending excluding temporary COVID-19 income supports and CEWS and hence excluding the myriad of job, income and rent assistance programs that combined legitimate spending with billions of wasted money. That measure of program spending will be 51% bigger by FY27–28 than it was in FY19–20 (chart 4). It is already about one-third bigger than before the pandemic and the spending plans will take it higher yet. There will be $171B more spending per year than they were spending in FY19–20 by the end of the projection horizon. At present it is 32% higher in FY22–23 than FY19–20. Minister Freeland calls that prudent; I beg to differ as she is the most free spending Minister of Finance this country has seen in a long time. This government will have increased its spending by one-half in a very short period of time as some Canadians love their handouts. Gone is the memory of 1990s deficits that made voters more careful as today voters seem to think returning to the Trudeau Sr era will be costless. Canada has departed from its post-1990s and pre-pandemic voter caution toward big spending promises and has entered a new era driven by massive spenders at Federal and provincial levels of government.

The Budget contained a net total of $43B more spending over six years. That includes $67B of new spending over the next 5 years offset only partly by about $22B of internal savings and higher taxes to feed the beast. Half of the $22B is comprised of tax hikes in an ongoing assault on traditional Liberal targets (successful folks, big corporations).

One driver is the upward revision to the cost of the dental plan for lower/middle income youths that is now estimated to cost $13B over 5 years which is double the $6B initially estimated amount.

Amid such pressures we have the most divisive inclusive budget I think I’ve ever seen. How so? It picks winners and losers by heaping $21 billion of annual subsidies on ‘clean’ stuff. You know, clean. Opposite of dirty. Politically saleable things that the Biden administration is subsidizing by even more and so Canada has to sheepishly follow. Sectors that loosely claim to be good for the environment over time. Funding them is an overt example of tilting the playing field and making every other taxpayer pay for it either at present or in future. And get this, in order to realize those subsidies, a condition is to pay union-level wages in an obviously pro-union policy stance and so the incidence effects will partly flow to organized labour.

The Budget assaulted banks and insurers with a $3.2 billion hit over 5 years by treating dividends received by financial institutions from holding domestic shares as business income. That’s rather curious at a time of turmoil across global banks! It’s a pure tax grab and coincides with funding pressures globally and as the BoC tightens the screws through rate hikes and QT’s effects.

The Budget was an assault on relatively wealthy folks with $3B more from changes to the Alternative Minimum Tax. There is a new “Grocery Rebate” of $467 for couples with 2 kids, $234 for singles no kids and $225 for seniors that will go to 11 million folks. Targeted they say. At $2.5B it’s another no-strings-attached handout that can be put toward anything just like extended GST rebates and other hand-outs that were announced last Fall. This is about the serial application of hand-out upon hand-out. Curiously it has absolutely nothing whatsoever to do with groceries and the name is just pure spin. The Budget also goes after card issuers and seeks to regulate prices that it calls ‘junk’ fees. That’s a nod to the left’s bias to control inflation through price controls. Good heavens the 1970s are calling us folks.

Overall, as a macroeconomist, it is my belief that efforts to downplay the magnitude of spending and debt are misplaced as Ottawa’s and the provinces’ spending are driving costly macroeconomic distortions. Net debt comparisons at an international level make Canada look good compared to basket cases but are meaningness. You can’t access the financial assets at a time of crisis that get netted out against debt in this figure. The assets are there to fund actuarial liabilities and across other governments are tied up in sinking funds and sovereign wealth funds. Quit comparing Canada on this measure. On gross debt to GDP Canada doesn’t look so favourable. General government (all levels combined) gross debt to GDP situates Canada well above the OECD average and climbing and just shy of the US where Trump and Biden tag teamed as co-authors of the book on how to run up debt albeit with the abused benefit of reserve currency status that Canada does not enjoy.

Furthermore, there are macroeconomic distortions stemming from all of this spending that include but are not limited to the following and that follow from yesterday morning’s note:

- it has contributed to some of the inflationary pressures that represent a highly regressive tax on lower and middle income Canadians while nevertheless transferring seigniorage revenues. They are being helped with one hand and hit with the other.

- it has contributed to a higher BoC policy rate than would otherwise be the case.

- it has contributed to worker shortages as public sector jobs are up 420k since just before the pandemic and account for 51% of all jobs created in Canada over that time. No wonder businesses are struggling to find workers!!

- it has contributed toward higher wage pressures and imo some of the productivity problem in this country where public policy has emphasized the body count in job markets over what is produced by whom.

- it has worsened competitiveness problems through spending that is primarily focused upon redistributive social transfers.

- In a broader public policy sense, Ottawa’s housing strategy remains confusing. The BoC is trying to contain inflationary pressures and soften previously raging house prices. The Feds have thrown open the immigration doors into a market with no supply while another tax subsidy to housing starts up on Saturday in the form of the 1st time homebuyers tax-free home savings account that allows one to shelter up to $40k tax free with annual contributions of $8k. Housing is going to rip after a temporary retrenchment and there goes the BoC’s efforts.

In all, I’m not impressed. This budget adds to macroeconomic imbalances and divides folks at a time when unity is needed to address the country’s challenges. Governments did a fantastic job in the early days of the pandemic. The problem is that they are now addicted to high spending and delivering divisive jabs at certain interests. Nothing is being done about productivity and competitiveness pressures that are mounting year by year. Big spending, big deficits, big debt, high taxes, high inflation and bond market challenges are not the path to prosperity.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.