ON DECK FOR FRIDAY, MARCH 17

KEY POINTS:

- Risk appetite wavers to end the week as key bank equities lose some momentum

- Fed figures show preference toward discount window over new facility so far

- China cuts reserve ratio requirements

- BoE inflation expectations decline

- US UofM, industrial production on tap

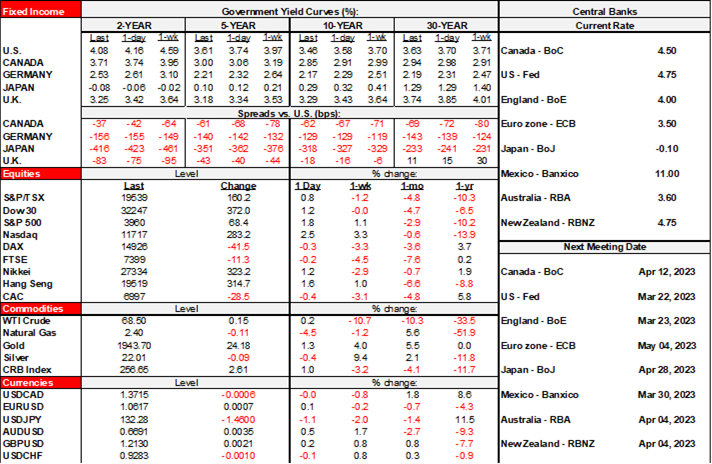

A wild week appears to be ending with wavering risk appetite amid relatively light incremental developments. The USD is retreating against all major crosses. US and Canadian equity futures as well as European cash markets are slightly weaker. Asian exchanges followed yesterday’s moves across western exchanges. US Treasuries are bid in a mild bull flattener move while gilts outperform rallying EGBs.

Bank stocks are under pressure again. First Republic is declining in the pre-market this morning in the wake of last evening’s deposit infusions and suspension of its dividend which go hand in hand. Credit Suisse is back below CHF2 again and perhaps partly on last evening’s headlines that rejected a combination of Swiss banks as an option. Still, the magnitude of the funding supports for US banks and CS allays funding pressures even as shareholder sentiment sours.

Late yesterday’s release of changes in reserve balances at the Federal Reserve (here) revealed a strong initial preference for utilizing the discount window following improved margin requirements over the Bank Term Funding Program. Discount window borrowing surged to US$153B. Take up in the Bank Term Funding Program was only $11.9 billion. ‘Other credit extensions’—a category that reflects lending by the FDIC to bridge banks—was up $142.8B. This mixture could well change going forward depending upon developments and as the new facility’s acceptance and understanding may improve after only three days of availability.

Fed funds futures are now pricing about 80% odds of a 25bps hike next week.

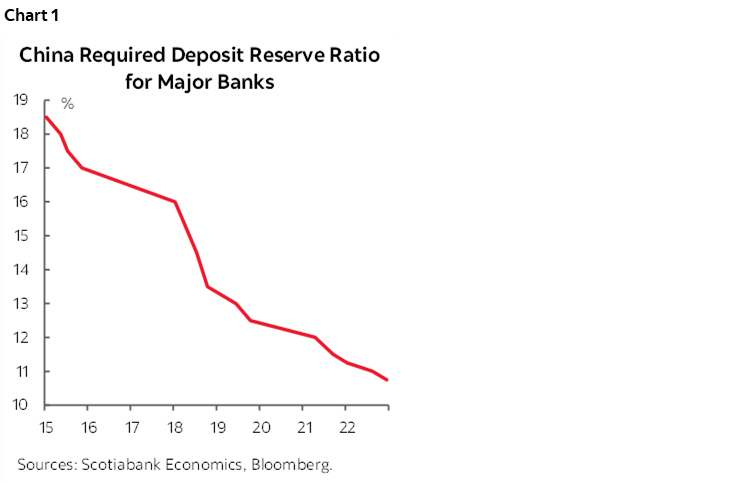

China cut its reserve requirement ratios again. The 25bps reduction kicks in on March 27th and it lowered the ratio to 10.75%. China had previously cut the rrr back in November and has reduced it by a cumulative 225bps since the pandemic started. Obviously, China is worried about the durability of economic growth given recent developments (chart 1).

The BoE’s latest inflation survey showed one-year ahead inflation expectations pulling back to 3.9%. Gilts were already rallying this morning but the headline prompted a slight further richening in 2s.

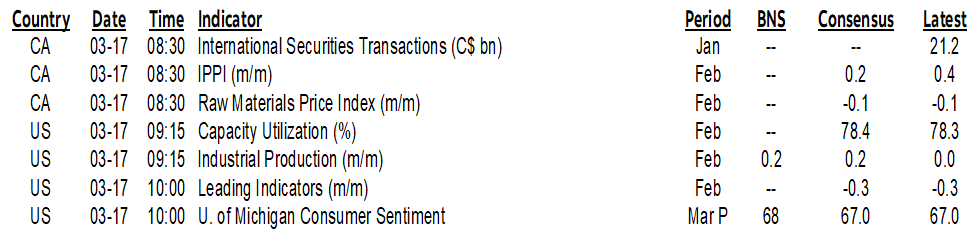

There is very little due out by way of calendar-based risk over the rest of the day as highlighted below. Inflation expectations in UofM sentiment (10amET) may be worth a peak as Powell has pointed to it in the past, but I would think it’s now well down the list of considerations into next week. Otherwise we have Russia’s central bank hold (who cares), the OECD’s fresh forecasts (ditto, as a long forecast process lags developments) and US industrial output (9:15amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.