ON DECK FOR THURSDAY, MARCH 16

KEY POINTS:

- With banks calmer, will the ECB be the spoiler?

- ECB pricing is on the fence between 25 and 50bps; there is a case for both

- The long and the short on bond liquidity

- A$ rallies on jobs, rates had a different take

- NZ$ dips on GDP miss

- BI held as expected

- US jobless claims still low, Philly Fed and housing starts also on tap

Risk appetite is tentatively improving but with the ECB looming ahead this morning. European cash equities are up by ½% to 1% and with bank stocks leading, but US and Canadian equity futures are slightly lower. Sovereign yields are pushing higher with US 2s up 13bps, gilts cheaper by 8–10bps across maturities and EGBs higher by double digits across countries and maturities. The USD is slightly weaker as the yen, CHF, euro and A$ (jobs, see below) lead the way. Fed funds futures are back to pricing about a two-thirds chance at a 25bps hike next week which is what I continue to think they will deliver barring any further calamities between now and then.

Credit Suisse is back up above CHF2 but has slipped a little from the opening. The Finma and SNB statement yesterday about providing supporting liquidity if needed is helping and so are CS’s CHF50 billion borrowing from the SNB and its buyback of CHF3B of its bonds. Perhaps a Saudi investor also learned a lesson here on choosing his words more carefully next time so as to avoid torpedoing his own investment!

Pair this with headlines on how First Republic Bank in the US is considering a sale among other strategic options, yet its share price is lower in the pre-market.

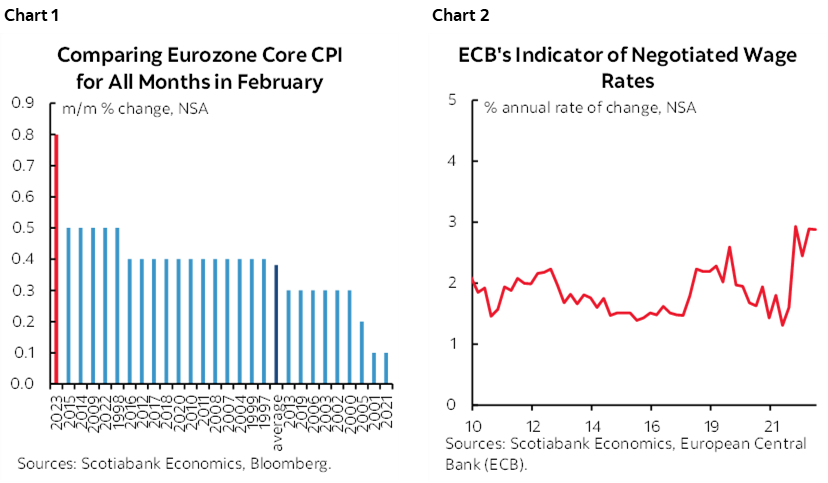

Market pricing for the ECB’s decisions (statement 9:15amET, press conference 9:45amET) has adjusted this morning in response to the stabilization in the banking sector. OIS pricing is on the fence between a 25bps and 50bps hike compared to pricing 25bps yesterday. Terminal rate pricing is capped at about a cumulative 75bps hike from here. To do nothing would signal panic in my view and risk backfiring while easing up on inflationary pressures. 50bps especially if accompanied by continued guidance for aggressive further hikes from before this recent round of banking sector developments would be a risky gamble under present circumstances but if accompanied by more cautious forward guidance then it could work. To this point there is no clear evidence of a looming major bank failure as opposed to a tightening of financial conditions that may make the ECB a little more cautious on the forward bias in a meeting-by-meeting sense. Still, we’re coming off the hottest core CPI gain for a month of February on record (chart 1) and accelerating wage gains (chart 2) in a system where more reliance upon collective bargaining can lead to lagging wage gains that continue to fan inflation risk. The ECB is further behind the Fed relative to neutral rates and is not yet materially restrictive.

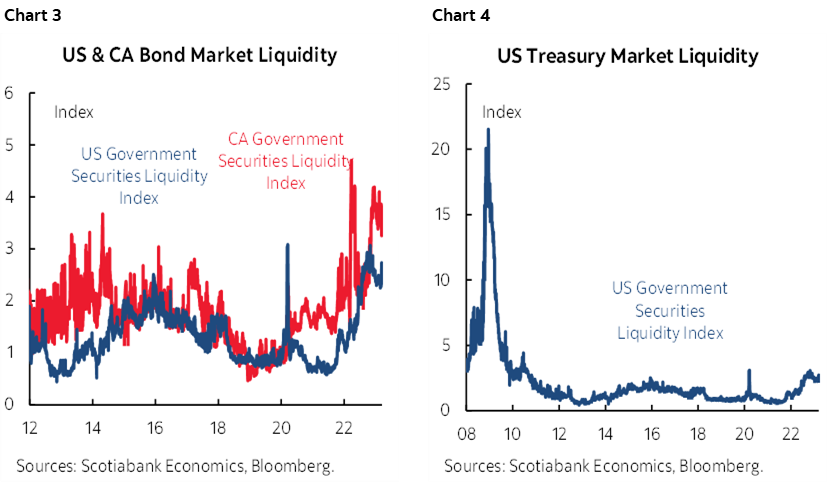

Bond market functioning is an added consideration for central banks and I don’t think they will view it as impaired enough to halt in their tracks. Yes liquidity has deteriorated, but depending upon one’s frame of reference. Chart 3 shows measures that are the worst in years after being spoiled. Extend it back in time and of course the GFC makes everything that followed pale by comparison (chart 4).

Australia beat expectations by posting 65k new jobs created in January (50k consensus) as the economy sprang back from two prior months of mild losses. All of the gain was in full-time jobs (75k) as part-time jobs fell by 10k. The participation rate ticked up to 66.6% and the UR fell by two-tenths to 3.5%. That was good enough to drive a gain in the A$, but the curve had other things in mind as a strong bull flattener unfolded on the argument that the RBA’s hike cycle is over and cuts may lie ahead.

New Zealand’s economy shrank by more than expected in Q4 (-0.6% q/q SA non-annualized) with a downward revision to the prior quarter (1.7% q/q SA non-annualized instead of 2%). That drove the NZ$ to be among the weakest crosses overnight and a rally in kiwi rates.

Bank Indonesia held its 7-day reverse repo rate at 5.75% as expected.

The ECB will clearly dominate an otherwise light N.A. line-up this morning including US weekly claims (8:30amET) and the Philly Fed’s regional gauge (8:30amET) as input to ISM-mfrg expectations. US housing starts during February (8:30amET) and Canadian wholesale trade (8:30amET) are also due.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.