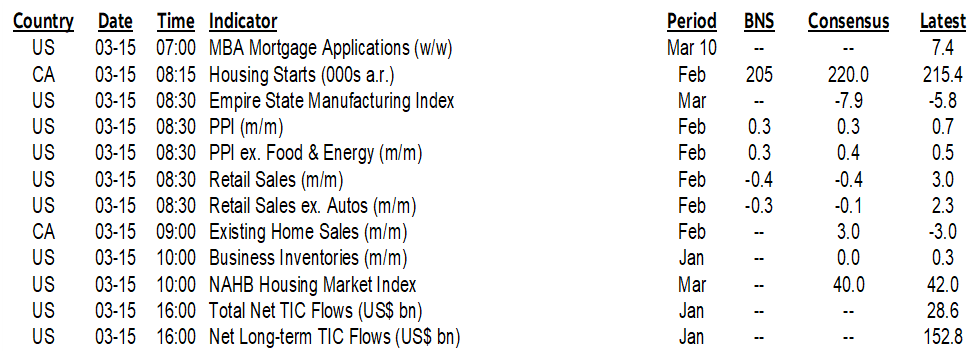

ON DECK FOR WEDNESDAY, MARCH 15

KEY POINTS:

- Credit Suisse slams global markets...

- ...as idiosyncratic risk versus driven by monetary policy...

- ...but key will be how the ECB plays it tomorrow

- Swedish inflation surprises higher, pushes yields up

- US retail sales will probably soften

- Core US producer price inflation probably held firm

- Canada updates housing indicators

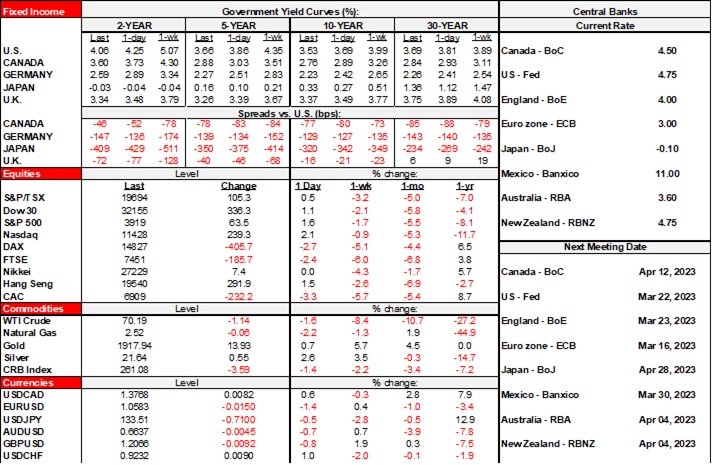

Oh what’s a day without more bank-induced volatility across global markets this time sent over with love from Europe. Risk-off sentiment is pushing equities lower as US and Canadian futures drop by about 1¾% – 2% and European cash markets declined by 2–3½%. A higher US 2-year yield earlier in the session rapidly gave way to a 21bps decline as the US curve slightly bull steepens. Canada’s yields are also down by double digits. Movements in yields on bunds and French bonds are roughly following declines in US Ts. The dollar is firmer along with the yen.

Credit Suisse remains a never-ending focal point as headlines about the company abruptly impacted world financial markets this morning. Its share price is falling again as its biggest shareholder stated that it refuses to invest further in the beleaguered bank due to regulatory issues and after “material weakness” was disclosed in its reporting yesterday. Record percentage changes sound more alarming to quote in splashy media headlines than citing the ~50 cents per share decline this morning from an already low starting point.

What else is new. From US$12 in early 2021, CS has steadily fallen to under $2 now as investors remain skeptical toward its turnaround plans and following one scandal after another last year from Archegos to Greensill to money laundering charges to unflattering leaks about the composition of some of its clients and the types of people the bank deals with. For that matter, its share price has been falling ever since the GFC as one of the few that couldn’t seem to benefit from record low rates and from central banks buying up every bond, kitchen sink and fruit stand on the planet and through one turnaround plan after another.

It will be fascinating to see how the ECB plays this tomorrow. There is a strong case to be made for how this is not being driven by monetary policy decisions versus viewing it as a never-ending idiosyncratic mess at a long deeply challenged bank. But can the ECB ignore it entirely? Not if systemic risk is present, but perhaps if the ECB has faith in management guidance on strength in core metrics and its turnaround plan and if the ECB thinks the worst case scenario is a ringfencing solution that keeps the emphasis upon conducting monetary policy toward combating inflation. We’ll see, but for now, markets are on the fence between a 25 and 50bps move tomorrow and more uncertain toward forward rate guidance.

Overnight calendar-based risk was fairly light. The PBoC left its main policy rate unchanged at 2.75% as expected. Retail sales and industrial production grew in line with expectations for the combined months of January and February as reported due to the Lunar New Year’s effects on the two months. The jobless rate climbed by a tick to 5.6%.

Riksbank watchers saw inflation surpass expectations for the month of February which drove massive relative underperformance across its curve this morning. Inflation was 1.1% m/m (0.9% consensus) with underlying inflation at 0.9% (0.7% consensus) and ex-energy at 1.5% m/m (1.0% consensus).

On tap will be three things that probably matter less to markets now than they might have had CS not abruptly impacted multiple asset classes.

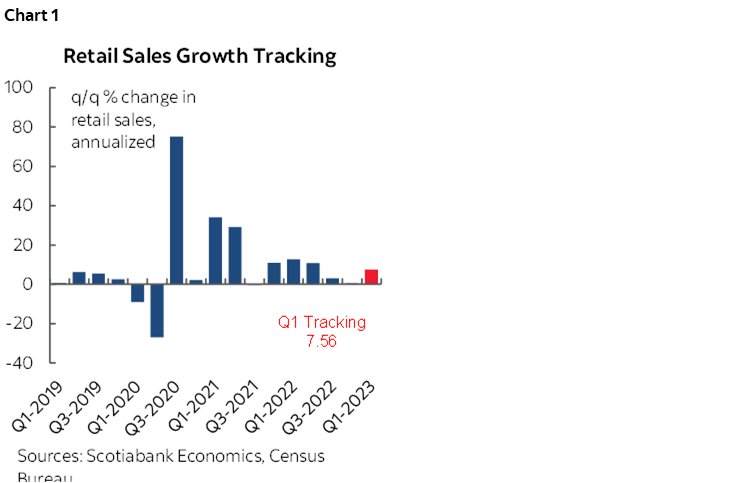

1. US retail sales are expected to soften with what we know in terms of autos and gas and following the prior month’s massive gain (8:30amET). Core is a bigger risk. That could dent the quarterly sales gain that is being tracked so far in chart 1.

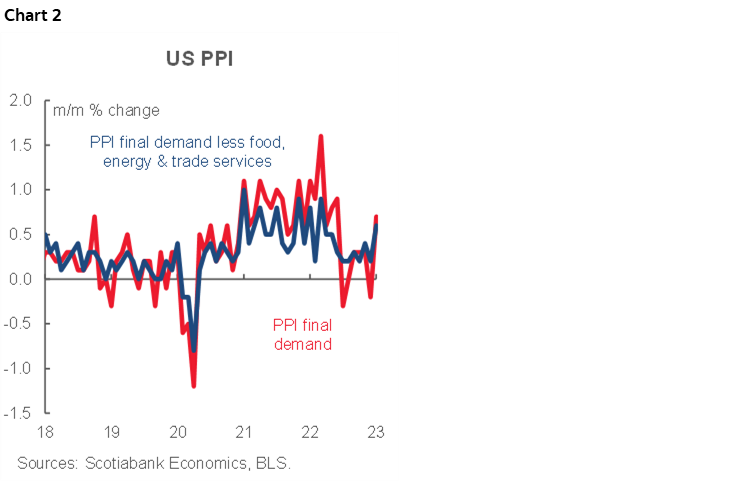

2. US producer prices for February and hence more inflation risk arrive at 8:30amET. Core prices ex-food and energy are the key here with another firm gain of 0.4% m/m expected which would indicate ongoing pressures to pass on higher prices to end consumers (chart 2).

3. Canadian housing data. It’s not usually market moving but housing starts (8:15amET) and resales (9amET) are on tap.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.