ON DECK FOR FRIDAY, JUNE 9

KEY POINTS:

- Canada week continues amid few other developments

- Canadian jobs to start the data dependent march to the July BoC decision

- Recapping what BoC’s Beaudry said…

- …on near-term and longer-term policy rate guidance

- China’s core inflation rate slips again

- Peru’s central bank holds, leans against easing

Canada week continues this morning with updated readings on the job market following BoC guidance late yesterday. Global markets face little by way of useful new information. Sovereign curves are mostly under cheapening pressure across US Ts, Canadas, EGBs and gilts. Equities are little changed across N.A. futures and European cash markets with a slight cheapening bias.

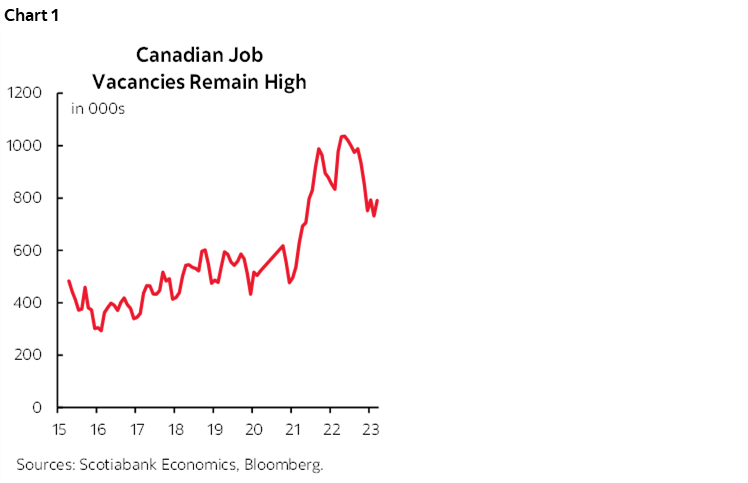

Canada’s jobs report for May (8:30amET) is expected to post another gain with a reasonably stable unemployment rate. It will inform the data dependent march to the July meeting along with the June jobs report before then. Most estimates range from flat to +50k with a median of about 21k. The 95% confidence interval for the Labour Force Survey’s estimated jobs changed is +/-57k and so the whole range of estimates is captured within the noise factor. One driver of the call is the fact that there remain 800,000 job vacancies which is hundreds higher than pre-pandemic levels and so even amid uncertainty toward how many are truly live this points toward ongoing excess demand for labour (chart 1). More drivers and expectations are in the Global Week Ahead (here). Key may also be wage growth that in m/m SAAR terms has slowed over recent months but may begin to accelerate partly as collective bargaining agreements start to filter through. Also watch the continued evolution of hours worked as a guide to GDP growth in Q2 following over 5% q/q SAAR growth in hours during Q1.

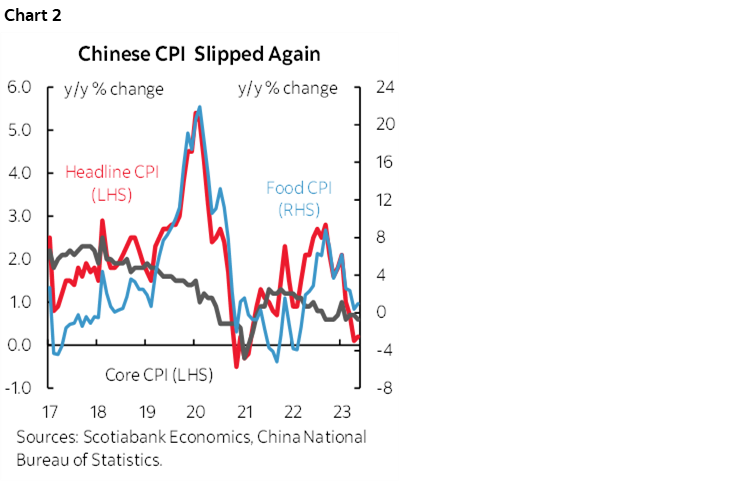

Overnight developments were light. China’s core CPI inflation slipped another tenth to 0.6% y/y with headline inflation matching expectations at 0.2% y/y (chart 2). That’s far below the state’s 3% target that they never hit while holding back on more material stimulus. Producer prices followed commodity prices lower and fell by 4.6% y/y.

Banco Central de Reserva del Peru held its policy reference rate unchanged at 7.75% again as widely expected. Guidance leaned against easing prematurely while sounding data dependent on the slim possibility of further tightening.

KEY TAKEAWAYS FROM BoC DEPUTY GOVERNOR BEAUDRY'S SPEECH AND PRESS CONFERENCE

BoC Deputy Governor Beaudry’s speech is available here and what follows are key takeaways drawn from the speech itself plus having watched his short 20 minute press conference after yesterday’s market close. It’s frankly more useful listening to what the BoC is saying than listening to loud cry babies who blew their calls and are throwing temper tantrums instead of committing to doing better next time.

1. Near-term guidance was data dependent and left the door wide open to doing more.

In response to a question during the press conference, Beaudry said they will be data dependent and that nothing is determined going forward but they have set out what variables they are looking at.

His speech text said "We’ll have more to say about all of this in our July forecast."

When pressed further during the press conference about what could tip the BoC in favour of a hike in July, Beaudry deflected once more and said they'll be looking at the data.

He was given another opportunity to comment on near-term policy rate expectations by commenting on market pricing for July and whether markets are behaving incorrectly and merely said that markets are looking at the same data they are and they don't have a predetermined decision and will be data dependent.

2. Neutral rate guidance came across as wishy washy.

Beaudry argued that they still thought the neutral rate range was 2–3% with a 2.5% midpoint as updated in the April MPR and the preceding staff research paper, but he also said they now view there to be upside risk to this estimate which matches my long held bias.

The speech elaborated on this upside risk including the following remark:

"Those ranges are our base case for where we think short-term rates will settle once inflation returns to normal. However, the risks around that base case are tilted to the upside. Looking across the four forces I just listed, there are good reasons to believe that some may be reaching a plateau or even changing course. That makes it unlikely the real neutral rate will fall below pre-pandemic estimates and creates a meaningful risk that it could go up."

He also emphasized that the policy rate might return to pre-pandemic lows, but it was more likely that the policy rate would be higher for longer. One could argue that by corollary, a 4.75% policy rate when neutral faces upside risk to their estimates indicates that they are less certain that policy is as restrictive as they may have previously thought.

Beaudry was asked why they didn't flag the upside risk to neutral in April as usual and why they are only choosing to do so now, and he largely ducked it. All that he said was that they still think those estimates for neutral are valid but now they think the risks are higher rather than lower. That’s unsatisfying and gave the appearance of acting on the fly.

Personally, while it’s clear they are attempting to manage market expectations over time, I'd massively haircut what they are saying by way of implications for longer dated forward guidance with the neutral rate discussion. Guiding 'higher for longer' may prove to be correct, but it was accompanied by guidance that maybe they will wind up returning to pre-pandemic lows for the policy rate and in any event, this is the same central bank that promised rates wouldn't go up until 2023+ and reeled in a lot of leveraged home buyers. Its forward guidance tool has been seriously damaged.

3. Immigration’s impact sounded more political than evidence-based to me.

When asked during the press conference about the impact of surging immigration and higher targets for years to come, Beaudry repeated the party line that it impacts both supply and demand and that the first approximation is that it's a neutral effect. He argued that what matters is at the level of individual households. My view remains that immigration affects demand more than supply from an inflation standpoint because it adds further demand stimulus to the household sector amid no evidence that it carries wage disinflationary effects. The US literature on the immigrant wage elasticity effect across numerous studies estimates that it is a neutral influence after controlling for other influences upon wage growth over time. If the BoC has credible research to the contrary then it should share it.

4. Nothing whatsoever was said on balance sheet plans even when Beaudry was asked about whether the BoC has other policy tools it can use beyond the policy rate.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.