ON DECK FOR THURSDAY, JUNE 8

KEY POINTS:

- Global bond markets rethink the BoC’s ripple effect...

- ...as Canada’s situation is influenced by idiosyncratic drivers

- BoC’s Beaudry, Macklem could further inform expectations

- The BoC’s balance sheet option

- US 2s richen as jobless claims edge up

- RBI adds another more hawkish than expected central bank

After the BoC's hike (recap here) blew a foul stench over world bond markets yesterday, a consolidation trade is part of what is richening curves somewhat into the N.A. open alongside US data. That could be because it’s unclear—at least to me—that the idiosyncratic drivers of the Canadian picture that are motivating further BoC tightening should be treated as fully portable across multiple bond markets.

For instance, the US debt ceiling deal will crimp some US government spending, but Canadian governments (plural, all stripes) can’t stop themselves while wondering why the central bank is neutralizing some of the fiscal pump-priming’s effects upon inflation. Further, the US doesn’t have Canada’s immigration surge with nearly 3% y/y population growth into a market with no housing supply, versus basically no population growth in the US. Or consider the terms of trade lift via commodities in Canada versus the net importer status of many other countries.

The RBI surprised markets with a hawkish hold to add its voice to hawkish moves from the BoC and RBA. No change in the RBI's policy rate was expected or delivered, but instead of shifting guidance toward something more neutral/dovish as some expected, it largely retained its concerns about inflation risk and a bias toward withdrawing accommodation. A trio of LatAm inflation prints generally came in a bit lower than expected in Colombia, Chile and Mexico starting last evening through to this morning.

The BoC will follow up on yesterday's hike with DepGov Beaudry’s explanations this afternoon and largely after the close. Speech highlights will appear at 3:10pmET and Beaudry hosts a press conference at 4:45pmET. Key will be anything that potentially informs forward guidance. Watch for anything more explicit around whether this is one-and-done or the start of a few hikes and the intermeeting timing of such possible moves. I suspect he'll say it depends on the data with a hawkish sounding bias.

Still, a key question will be whether the past tense reference to how Governing Council judged that “monetary policy was not sufficiently restrictive” also applies in a future tense.

The concluding paragraph’s guidance that the BoC “will be evaluating whether the evolution of excess demand, inflation expectations, wage growth and corporate pricing behaviour are consistent with achieving the inflation target” suggests openness to doing more but watch for any further interpretation of what this meant.

Any intimation around whether possible further tightening is likely to be along a straight line or with serial pauses for reflection along the way could also inform meeting-by-meeting pricing for policy rate moves. A risk is if serial pauses are signaled then perhaps July hike pricing is too high, or it may be reinforced by Beaudry’s possible remarks.

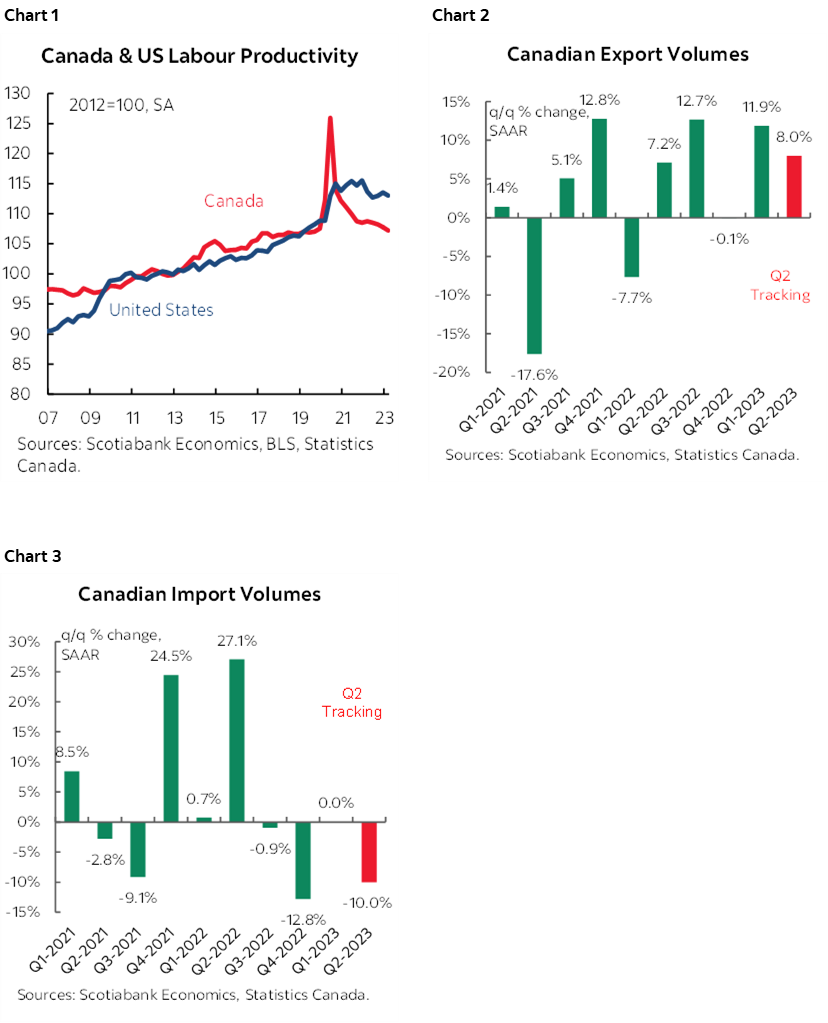

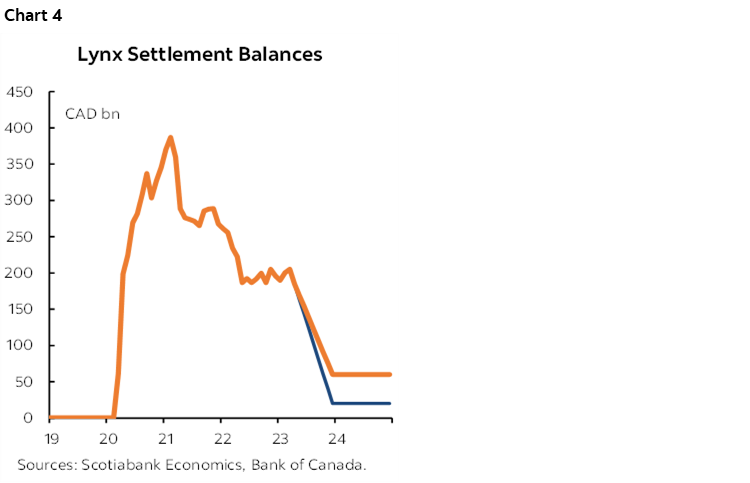

Furthermore, we’ve already seen some fresh data since the statement was crafted in advance and perhaps Beaudry will offer some reaction to it. For one thing, before the statement landed yesterday morning, Q1 labour productivity fell by -0.6% q/q SA nonannualized versus my estimate of -0.4% and hence continued the poor trend (chart 1), and Statcan also released ripping net trade figures. Charts 2 and 3 showcase what kind of trade growth Canada seems to be registering in Q2 based on the Q1 hand-off and April figures before we get complete Q2 data. A combination of export strength and less of an import leakage effect could sharply raise our 2 ½% nowcast tracking for Q2 growth and put it further ahead of the BoC’s 1% forecast in the prior April MPR that they have to revise upward. The good news here would be continued economic resilience, but the bad news would be greater rate pressure as the economy just keeps pushing further into excess demand conditions.

I guess it’s also feasible that Beaudry will be asked about balance sheet plans, but doubt he’ll offer much. That would be more likely to come from DepGov Gravelle or Macklem, and not now. Nevertheless, a former Deputy Governor Murray remarked yesterday that the BoC may have to entertain active QT versus its passive 100% roll-off approach toward maturing holdings of GoC bonds thus far. I still have a lot of sympathy for that view from when I put out a piece on the topic at the end of March.

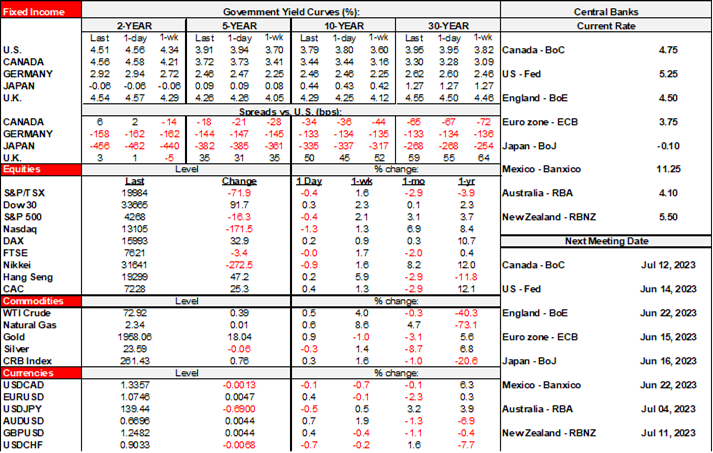

Recall guidance from Deputy Governor Gravelle’s earlier speech on this topic. They are targeting vastly leaner Lynx settlement balances at 1–2% of NGDP versus the Fed's targeted 10–13% reserves as a share of US NGDP (chart 4). That implies somewhere around $20B–$60B from $172B now and that amount has been fairly range-bound since about mid-2022. That's a much leaner framework being targeted by the BoC, perhaps partly reflecting a sounder and more stable banking system. It could be that to jolt sticky reserves lower the BoC has to act more decisively around QT plans.

They've guided an end to QT roll-off plans between the end of 2024 and 2025H1 which is later than we have assumed for the Fed. That would imply GoC holdings bottom between about $230–270B by that time frame if they only allow roll-off. That's still way above pre-pandemic levels that were around $80B. On its own that may not be enough to get reserves down toward their target, or their reserves target is too low. To speed it up they could invite active asset sales as one option and that would have to mean GoCs to be meaningful. It’s a curiosity as to why the BoC still holds over $4B of real return bonds with no issuance relative to persistent demand but shedding those would only serve a signaling role absent a material effect. Shedding provincial bonds at $10.7B could add to this but would still be relatively small potatoes. The case for more active QT would be to tighten monetary policy through quicker reduction of reserves and by impacting the term structure of interest rates.

In Gravelle's speech, they did guide that timing the end of QT and the amounts of reserves and GoC holdings could be adjusted relative to market conditions with the main metric being policy rate spreads and other potential dysfunction in short-term money markets that we're not seeing thus far.

Also watch for anything that may come out of Governor Macklem’s private off-the-record appearance at the C.D. Howe Institute in Toronto this evening (here). I doubt that he will offer materially further remarks compared to yesterday’s statement, today’s comments from Beaudry and prior remarks from Macklem.

The US calendar is pretty light with just a mild uptick in initial jobless claims to 261k last week with no states estimated this time, while continuing claims fell to 1.757 million from 1.794 million. Still, it’s just one week and we’re in between nonfarm reference periods. The Fed will also release the quarterly US financial accounts (12pmET) that include various measures of household and business finances that may motivate headlines on the state of finances.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.