ON DECK FOR WEDNESDAY, JUNE 7

KEY POINTS:

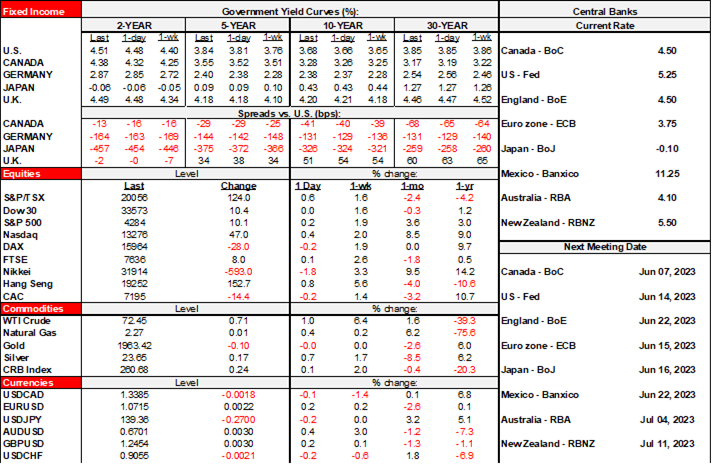

- Sovereign yields continue to grind higher

- If the BoC whiffs, then it could unwisely engineer cut pricing all over again

- The BoC hold-for-longer alternative…

- …would mean having learned absolutely nothing about limits to forward guidance

- The case for a BoC hike has strengthened since they considered one in April

- Preserving optionality throughout Summer merits a BoC hike today

- Other overnight developments

The BoC will be the main focal point in a statement-only affair at 10amET. Other overnight developments were mild in nature with brief comments offered at the end of the note so we can quickly get to the BoC. Sovereign debt yields are under mild upward pressure across the world’s main benchmarks again while the USD is broadly weaker, stocks are flat to a touch lower across N.A. and European benchmarks and volatile oil prices are up by under 1%.

The Bank of Canada is a statement-only affair (10amET) sans presser or forecasts. The BoC surprised markets in 3 out of 8 decisions last year and surprised the median consensus call on two of those occasions. Right now, markets are pricing about 50–50 odds of a rate hike today and fully pricing a 25bps hike in July and then much of another one thereafter. A minority of economists expect a hike today; who knows what many of them think about July but one thing I do know is that there are not 37 folks who suddenly know Canada in the consensus polls. That said, several Canadian banks are hedging their bets with competing calls. The goal of forecasting higher shorter-term market yields off of the March lows has been achieved and now we’re into the finer strokes on the call.

What if they don’t hike? The case for hiking is solid and laid out in multiple notes (like here) and calls but it’s the alternative scenario of what would happen if they didn’t hike that perversely provides additional logic for hiking.

If the BoC doesn’t hike or provide very explicit guidance toward hiking more than once, then they’ll have to explain why they chose to ease financial conditions relative to what’s priced because that’s likely what would occur. Markets would view Governor Macklem as having said all along that he was leaning toward hiking if the conditions got violated as laid out below and then falling short when they did. That would be taken as a clear signal that the next move is more likely to be lower and it would probably resurrect a swing in positioning toward a pile-on into the rallying front-end that the BoC cannot or shouldn’t want to court at this point. Hike today and you preserve greater optionality over Summer.

This is also one reason why the alternative scenario of signalling a longer hold instead of hiking makes no sense and there are three other reasons to add to this:

- Markets don’t believe central banks’ longer-term forecasts at the best of times (or anyone else’s…). Say all you want about next year and beyond and all markets will hear is that you’re not hiking now, so buy, buy, buy away and we’re back to March with Macklem scratching his head over how that happened.

- Markets extra don’t believe Macklem’s longer-term forward guidance. Listen to the guy who reeled in leveraged suckers when he said he wouldn’t hike for years and years in the depths of the pandemic?? Oh that’s rich…. Surely we’ve learned something from the pandemic. Fool me once, shame on you, fool me twice, shame on me if folks believe the longer hold fairy tale again. The lesson is that longer-dated forward guidance doesn’t work because central bankers can’t forecast and shouldn’t promise that they can.

- Time is of the essence here. With each passing month that households and businesses see persistent core inflation at well above target rates and surging housing markets it gets more and more difficult for the BoC to convince folks that it is serious about doing whatever is necessary to bring down inflation and preserve financial stability. Keeping rates at current levels for longer in future doesn’t achieve the goal of intervening against such forces now.

- So what has tipped the balance now versus when Macklem said they discussed a hike in April but held off to evaluate further evidence?

- GDP is materially beating the BoC’s H1 expectations. 3.1 in Q1 versus 2.3 forecast, nowcast tracking 2 ½% in Q2 versus the BoC’s 1% forecast.

- this means more excess demand than they had judged in April which is going in the opposite direction to what they deem to be necessary to ease inflationary pressures back to 2% in the medium term.

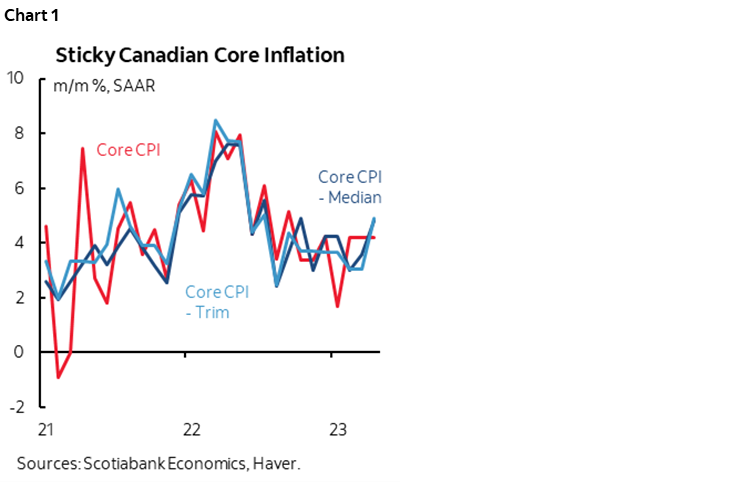

- April core inflation in May accelerated to 4%+ m/m SAAR using trimmed mean and weighted median and traditional core (chart 1). The only improvement was over 2022H1 and since then these readings have been remarkably sticky at rates well above the BoC’s target.

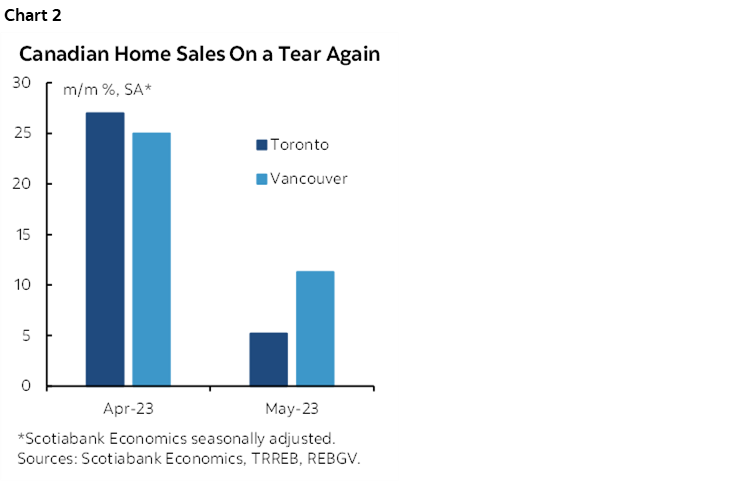

- Housing is back on a tear again with surging home sales and prices across major markets (chart 2).

- The debt ceiling is predictably donezo.

- Regional bank hiccups have stabilized

- Wage settlements in the public sector and spillover effects into airlines have become amplified.

Other overnight developments are summarized as follows:

- Chinese exports disappointed, with currency depreciation playing a significant role. In local currency terms, exports were down -0.8% y/y but in USD terms, exports fell by 7.5% y/y. Newswires only really reported the USD figure and missed the currency effect. The yuan fell by about 4% in y/y terms and has been depreciating since mid-April. Imports were up by 2.3% y/y in yuan-denominated terms but down 4.5% in USD terms.

- German industrial output beat expectations on revisions. April’s output was up by just 0.3% m/m (0.6% consensus) but the prior month’s previously reported 3.4% drop was revised up to -2.1%. That’s still clearly not great.

- Australian GDP was a wash relative to expectations. Q1 missed a touch (0.2% q/q nonannualized, 0.3% consensus) but the prior quarter was revised up a tenth to 0.6%.

- The OECD updates its projections this morning. They now see the world economy growing by 2.7% in 2023 and 2.9% in 2024. The US is projected to grow 1.6% and 1% in 2023 and 2024 respectively. Canada is forecast to grow by 1.4% in each year. In no major region is a full year contraction being forecast.

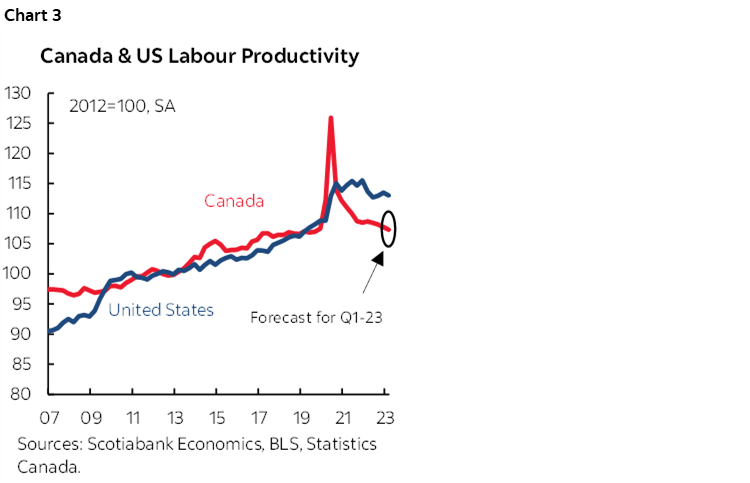

On tap into the N.A. session are a few distractions with the primary focus being the Bank of Canada’s statement (10amET). Canadian labour productivity arrives just before that (8:30amET) and I’m expecting another dip of around -0.4% q/q nonannualized that would extend the miserable trend (chart 3). Canada also updates trade figures for April at the same time. The US updates trade figures as well but they only tack the services surplus onto the already known deterioration in the goods balance due to higher oil prices in April that then reversed in May.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.