ON DECK FOR MONDAY, JUNE 5

KEY POINTS:

- Bonds cheapen, USD strengthens on debt supply and oil prices

- The futility of Saudi oil cuts

- US bank capital proposals miss the target

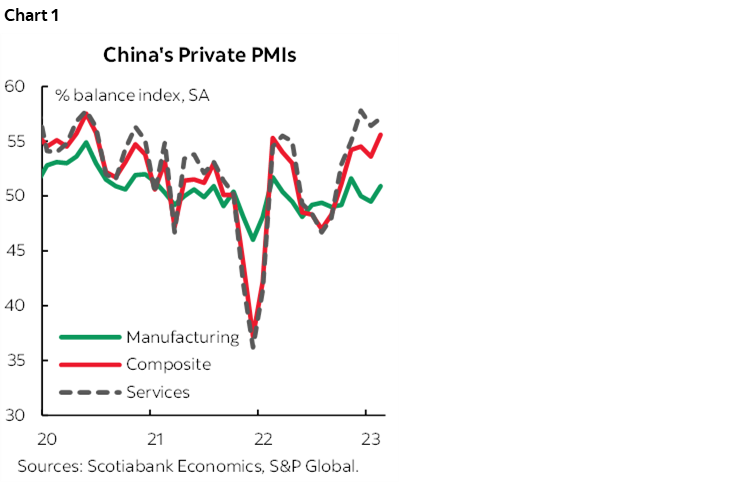

- China’s private PMIs beat the SOE-dominated state PMIs

- Markets see this week’s BoC decision as a coin toss

- US ISM-services, factory orders on tap

- German exports surprise higher, markets ignore

- BI’s extended hold vindicated by softer inflation

- Global Week Ahead

As a reminder, please see the Global Week Ahead—Macklem’s Chance to Prove He’s Serious here in full publication format and for clients the slide deck is here.

Key topics:

- June FOMC is still ‘live’

- The BoC needs to hike…

- …as its conditions have been violated

- Canadian jobs, wages and productivity

- Treasury to replenish cash account

- RBA decision resembles the BoC’s

- RBI to hold, forward guidance key

- BCRP likely to extend hold

- Global inflation updates

- China’s nonexistent inflation

- Other global indicators

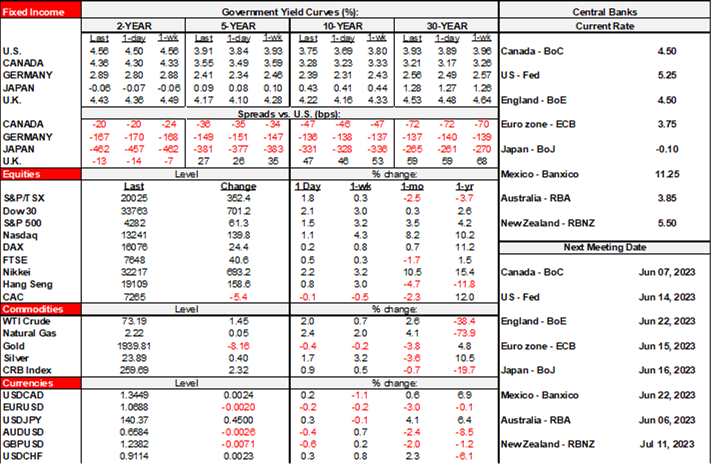

After some Asian equity benchmarks played catch-up to nonfarm payrolls, their enthusiasm is not carrying forward into the western benchmarks so far this morning. US and Canadian equity futures are flat and so are most of the main European indicates. Sovereign bond yields are under upward pressures and the dollar is broadly stronger probably as an ongoing effect of the payrolls surprise plus coming—but transitory—supply pressures in US debt issuance as the US Treasury seeks to replenish its cash balances that were depleted due to the debt ceiling’s freeze.

Truly fresh developments that are likely to be durable as opposed to fleeting are pretty light to start off a new trading week. The Saudis took another probably futile swing as the oil market. Few should be surprised by a report out in the WSJ on tighter US large bank capital requirements. Even fewer should be surprised that smaller non-SOE producers are beating the SOEs in China. Modest US data is on tap this morning.

Saudi Arabia’s pledge to cut 1 million barrels of production per day starting July and the extension of cuts by others to the end of 2024 is contributing to a modest gain in oil prices of under 2%. These cuts were accompanied by a Mario Draghi-style ‘whatever is necessary’ pledge by the Saudi oil minister that indicates a bias to possibly do more. One reason these cuts have modest and usually fleeting effects is that OPEC+ isn’t what it used to be; it accounts for just 40% of world oil production. Another reason is that being a cartel invites cheating across members. A third reason is that there are many other supply and demand considerations and it’s the demand side particularly related to China’s challenges that have dominated of late.

Markets are taking in stride a WSJ piece that indicates large US banks may face an average 20% increase in capital requirements under proposed changes to regulations and depending upon the nature of the institution’s business. After piddly, accident-prone regional banks blow up, the response of US regulatory authorities is curiously to make the big banks pay the price even despite the role they played in propping up some of the regionals. Tying up even more capital after the post-GFC changes would be a further growth headwind. US bank share prices are so far shaking off the report this morning, perhaps because it has been anticipated over recent weeks and months.

China’s smaller non-SOE producers powered the Caixin composite PMI higher by two full points to 55.6 and hence further into above-50 growth territory. That stands in contrast to the state’s composite PMI that had previously fallen by 1.5 points to 52.9. After the state’s services PMI fell, the Caixin services PMI climbed. The upside to the private PMIs probably came as little surprise to markets given the understanding that the state PMIs are impacted by the more challenged SOEs.

Bank Indonesia’s hold at 5.75% last week was vindicated by slightly lower than expected core CPI during May that fell back a tenth to 2.7% y/y. In m/m seasonally unadjusted form, May posted an abnormally weak month compared to all prior months of May.

German exports surprised higher, but the release was shaken off by rates and the euro. Exports were up 1.2% m/m in April (-2.5% m/m consensus) but the prior month was revised to be a little worse contraction of 6% m/m (from -5.2%).

On tap into the N.A. session is pretty light US data and nothing out of Canada. Most expect US ISM-services for May (10amET) to rise a touch and thus indicate slightly firmer growth. Factory orders for April (10amET) will also get a boost from the already known jump in durable goods orders, to which they’ll add whatever happened to nondurables.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.