ON DECK FOR TUESDAY, JUNE 27

KEY POINTS:

- Light overnight developments shift focus to Canadian, US releases

- Canadian CPI to further inform BoC pricing for the July decision

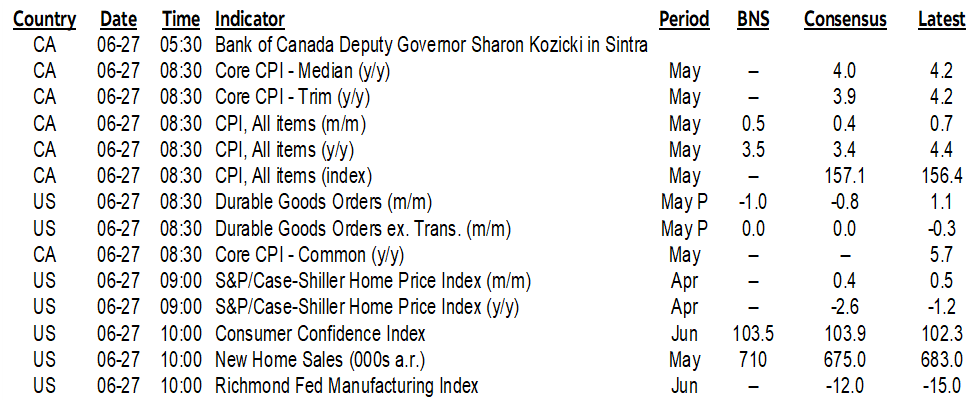

- China’s managed yuan depreciation

- ECB’s Lagarde tells us what markets already knew

- Tire kickers are supporting US new home sales

- US consumer confidence will probably follow UofM higher

- Can US house prices make it two-in-a-row?

- US durable goods orders probably fell

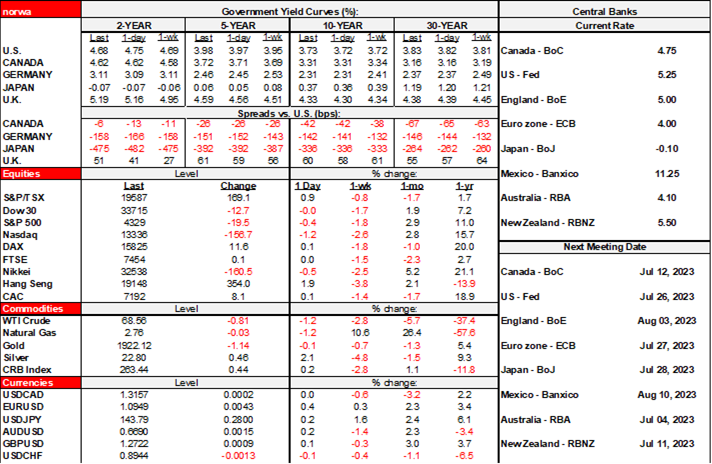

The main focal points will be Canadian CPI and several US releases around the same time. Overnight developments were light, as China continues to fight yuan depreciation in largely futile fashion and the ECB’s Lagarde fell flat in her key opening address at the Sintra boondoggle. Equities are mixed but generally little changed across N.A. futures and European cash markets. Gilts are underperforming other curves that are little changed on balance thus far. The dollar is broadly softer. CAD and the Canadian front-end may be vulnerable to CPI this morning.

China continues to attempt to drive a strong yuan, or at least stem the pace of depreciation (chart 1). The PBoC set a lower reference rate of 7.2098 and while it appreciated on an intraday basis a) it did so on a day of broad dollar softness, and b) the yuan is already shaking it off at just shy of 7.22 which extends the pattern of persistent deprecation against the fixings. The yuan has been depreciating all year and is about 8% weaker than in January. Such intervention is largely futile against the pattern of mild Chinese policy easing amid growth downsides, versus a continued Fed-tightening bias.

I suppose ECB President Lagarde thought she was saying something meaningful in her opening comments at the ECB’s Sintra forum. A closer look at her exact quote should result in a shrug of one’s shoulders relative to what was already priced and therefore for an opening address she fell flat in terms of offering something incrementally insightful. She said:

“It is unlikely that in the near future the central bank wil be able to state with full confidence that the peak rates have been reached. Barring a material change to the outlook, we will continue to increase rates in July.”

Markets were already pricing most of a quarter point hike on July 27th and she already said she was leaning toward a July hike at the last meeting. Furthermore, markets were already leaning toward another hike in September.

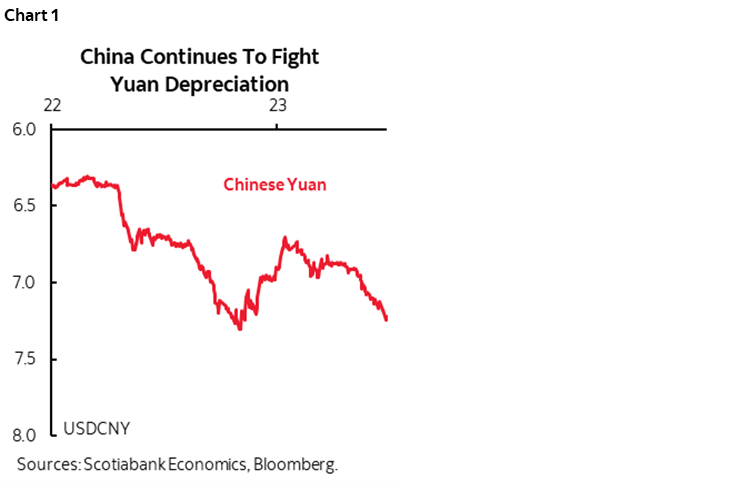

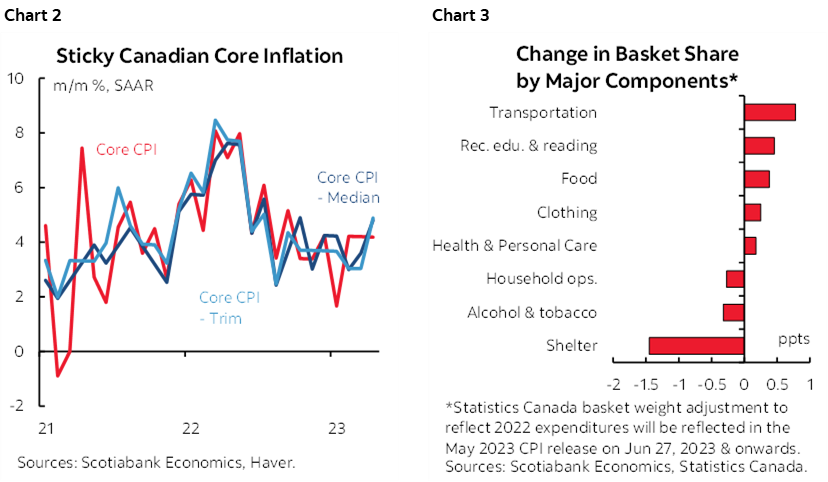

Canadian CPI today (8:30amET), Friday’s GDP for April and May, Friday’s Bank of Canada surveys including measures of inflation expectations and then the following Friday’s jobs reports should firm up market pricing for the July 12th decision that is appropriately set at about a fair coin toss at the moment. Most expect Canadian CPI to rise by 0.4–0.5% m/m NSA and 3.4–3.5% y/y (Scotia 0.5% / 3.5%). Seasonally adjusted headline would therefore land at 0.1–0.2% m/m with seasonally adjusted traditional core CPI at 0.4% m/m. Key will nevertheless be the trimmed mean and weighted median gauges with no credible consensus given how sensitive these readings are to modest variations in the composition of the price changes and the limited tracking evidence of the 55 price series that go into calculating them. These ‘core’ readings have been remarkably sticky ever since the only period of improvement over 2022H1 (chart 2). Basket weight changes shown in chart 3 shouldn’t materially affect the year-over-year rate, but the month-over-month pace may be slightly vulnerable to the 1.5 ppt lowered weight on shelter—primarily due to lower weights on real estate commissions that were likely higher and legal fees and new house prices that edged up for the first time since late last summer—and raised weights on other components given that Statcan never adjusts prior months for the basket changes that take effect in today’s May readings. That’s easily controlled for but will take a bit of time post release in order to see if the weighting changes affected the month-over-month reading.

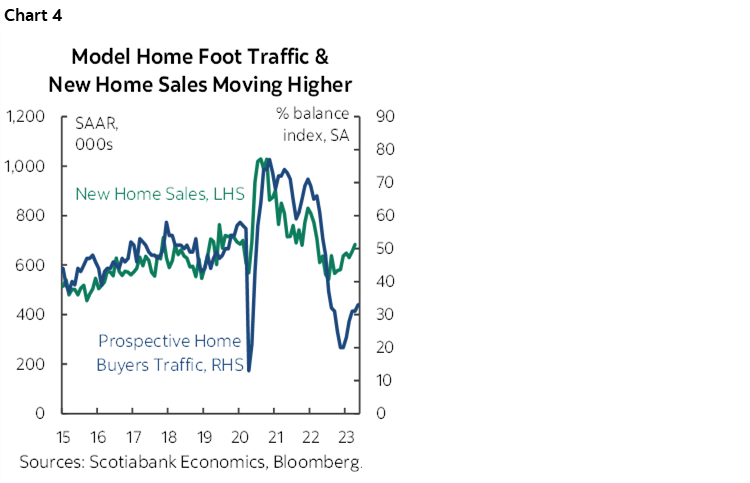

US releases are expected to reveal a drop in durable goods orders during May (8:30amET), a second consecutive rise in repeat-sales home prices (9amET), possibly higher new home sales given signals from model home foot traffic (chart 4), continued softness in the Richmond Fed’s regional manufacturing survey (10amET) while consumer confidence will probably follow the UofM gauge higher (10amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.