ON DECK FOR FRIDAY, JUNE 2

KEY POINTS:

- Global markets are in risk-on mode ahead of nonfarm

- Nonfarm and wages still matter to the Fed

- Canada’s real estate market is on fire again, inviting policy responses

- China mulls property market supports

What markets are doing right now probably matters little ahead of nonfarm, but they’re in risk-on mode at the moment. N.A. stocks are pointing toward a ½% rise with European cash markets up by around 1% across all benchmarks after 1%+ rallies across Asian led by a 4% jump in the Hang Seng. Sovereign yields are up by single digit basis points across most benchmarks in Europe but little changed in N.A.. The USD is little changed. Oil is up by over a buck. There were few overnight catalysts. China is reportedly working toward new measures to support property markets according to unconfirmed reports from anonymous folks.

After the Senate passed the debt ceiling deal it’s now time to clear the floor for nonfarm payrolls as pretty much the lone release of significance. I don’t buy the line that it doesn’t matter to the Fed and for that argument rely upon the points I made in yesterday morning’s note (here) about the literary licence being applied to distorted impressions of Fed-speak. The FOMC will be data dependent into the June decision in my view and today’s data plus the next CPI report will matter to them.

Here’s the preview:

- consensus median: 195k

- consensus average: 192k, so no material skewness

- Whisper number: 225k

- Scotia: 225k (not meaningfully different given the 120k 90% confidence interval)

- High/Low: 252k / 100k. None of these estimates are outside of the noise bands.

- Std dev: 25.6k

- Wages: 0.3% m/m (range 0.2–0.4)

- UR: 3.5% (3.4% prior)

Most drivers indicate continued resilience:

- JOLTS job openings picked up by 358k to back above 10.1 million. Even if some are zombie posting, the tally is still about 3 million above pre-pandemic norms indicating hiring appetite.

- initial jobless claims were fairly stable between nonfarm reference periods

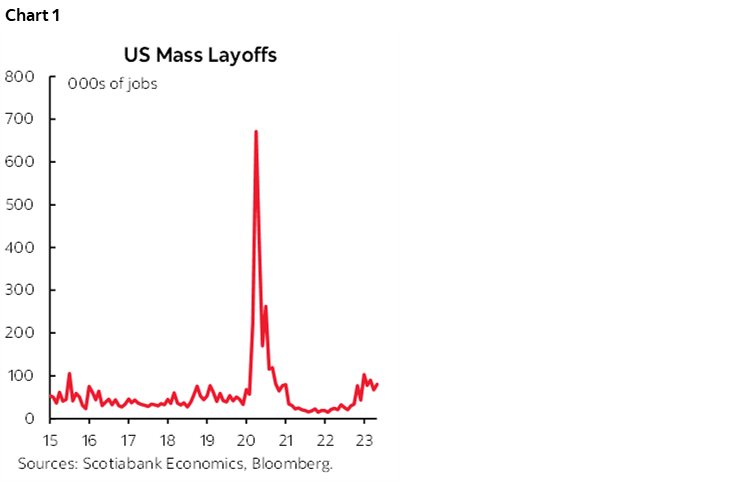

- Challenger job cuts equalled 80k in May which is still not enough to derail job growth. All that job cuts have done is come off the practically non-existent levels from the initial stages of the pandemic recovery back toward something that is more normal at slightly above pre-pandemic levels thus far (chart 1).

- ADP at 278k suggests possible upside but with a heavy head fake factor

- ISM-mfrg employment picked up. We get ISM-services employment next week.

- conference board’s consumer confidence ‘jobs plentiful’ gauge slipped to 43.5 from 47.5

Canada’s housing market continues to be on a tear as a combination of very little supply, surging immigration, a return of first-time home buyers, strong job markets, a premature halt to BoC rate hikes and returning FOMO sentiment drive renewed imbalances. I’ve argued since last year that consensus was far too negative toward Canadian housing as it over-emphasized the pressures facing a minority of super-stretched mortgage holders in a classic case of the tail wagging the dog. The broad fundamentals of Canada’s housing market remain highly constructive and will carry ongoing positive spillover effects for consumption as we saw in the Q1 GDP accounts. Recall that home sales were up by 11% m/m SA in April for the biggest monthly gain since the initial stages of the pandemic recovery in mid-2020 and have risen for three straight months. The city-level data for the month of May looks like momentum will continue. Toronto’s home sales figures for May (here and here) were up by 5.2% m/m SA in May and about 25% y/y as listings fell by about 19% y/y but new listings were up by 10% m/m. Prices were up by over 3% m/m SA with the average now at C$1.2 million. Months supply is practically non-existent at 1.3 months.

With Vancouver pending, Toronto adds to evidence of strength in Calgary that posted a record high for all months of May along with a sales-to-new-listings ratio of 85% and months’ supply of just 1 month on tap. One month folks, in both Toronto and Calgary. This country’s policymakers get an ‘F’ for mismanaging housing supply and for serially over-stimulating housing demand and here we go again.

The BoC would hike if it felt that its conditional pause was being violated with renewed upside risk to inflation. This risk is reality in my view, but the reintroduction of sharp housing imbalances should add to the case for tightening that is primarily based upon inflation.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.