ON DECK FOR FRIDAY, JUNE 16

KEY POINTS:

- Global markets digest ECB-speak, BoJ

- ECB officials lean toward multiple hikes

- BoJ stands pat...

- ...but here are the guideposts to watch for signs of a pivot going forward

Global asset classes are mixed to end the week amid light macro developments. N.A. equity futures are little changed, while European benchmarks are up by between ¼% and 1% perhaps in part lagging yesterday afternoon’s S&P gains. US Treasuries, gilts and Canadas are slightly cheaper in bear flattener terms, while EGBs are a tad richer albeit volatile around ECB-speak. The dollar is flat on a DXY basis, with the most notable move being yen depreciation post-BoJ. There is practically no data risk (UofM pending, Canadian wholesale trade miss) amid a need to consider ECB- and Fed-speak that offer modest risk. I’ll cover the BoJ decision below along with an empirical attempt at explaining the guideposts to monitor going forward.

A round of post-decision ECB-speak this morning generally leaned toward keeping hike options open beyond July with some of it keeping options open to possibly hike beyond September. That’s consistent with my reading of yesterday’s ECB communications and President Lagarde’s press conference in that a) she reinforced the consensus set up for a July hike, and b) she said there was no discussion of a future pause or skip in their deliberations which is perhaps a signal on its own, and c) they raised their inflation forecasts to be above target throughout the entire horizon. That all leans against there just being 1–2 more hikes and then done, but we’ll see. I can easily see a 4+-handled target rate.

Fed speakers start lining up today, but they offer low risk. Bullard already spoke earlier this morning, but I don’t detect any comments of relevance to markets as he presented on optimal macroeconomic policies at a joint IMF-Norges Bank conference in Norway. Governor Waller spoke after Bullard at the same conference and on a four-person, 90-minute panel discussing ‘challenges facing macroeconomy policy’ of which there are a few! Waller sounded skeptical toward the argument that developments in US banking could add to credit tightening beyond the natural transmission mechanism of tighter monetary policy. Then Richmond Fed President Barkin (voting 2024) will speak on inflation shortly (9amET).

Data risk is very low with nothing out overnight and only US UofM consumer sentiment on tap this morning (10amET). UofM might get more attention than normal given nothing else to focus upon and if it sharply surprises.

BoJ DECISION AND WHAT TO WATCH FROM HERE

The BoJ left policy measures unchanged while offering cryptic clues that keep uncertainty at elevated levels toward policy actions over the second half of 2023. Each of the policy balance rate of -0.1% and the 10-year yield target of 0% +/- 50bps were left intact. Governor Ueda said that a “big shift” in the inflation view could merit a tighter stance which sets a high bar for the coming forecast changes at the July meeting to matter. He also made it clear that they don’t feel compelled to set up any such moves in advance in favour of saying “It’s inevitable that sometimes there’s a certain element of surprise.” The moves were widely expected, but there was clearly a tail in the market that was positioned for less dovishness. The yen weakened by about ½% to the USD and rose toward 141. The 10-year yield slipped just beneath 40bps. The Nikkei rallied by about 0.7%.

Is Ueda right? That’s a tough call that time and data will inform along with the BoJ’s future posture, but the arguments are more balanced than some of the diametrically opposing commentaries I’ve seen.

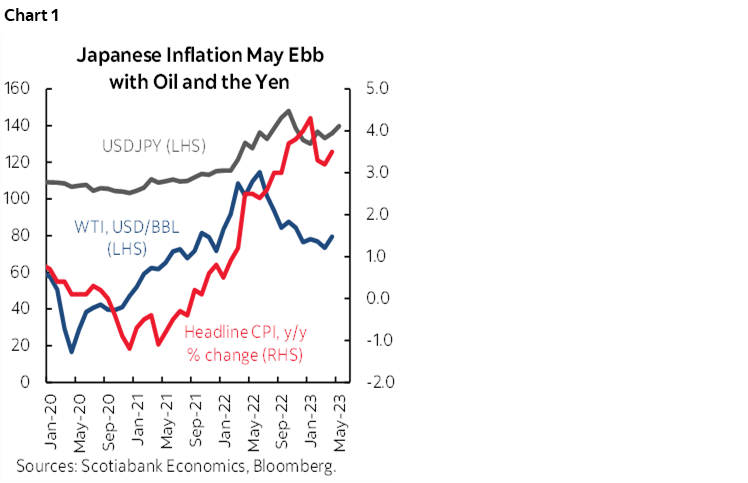

On the dovish side, the standard narrative is that Japan has seen many false starts to inflation since its property and market bubbles burst 3+ decades ago and been burned by premature actions from the BoJ in the past. Japanese inflation is also buoyed by some transitory drivers such as the ongoing lagging effects of last year’s yen weakness and higher oil prices (chart 1). Japanese real wages also remain weak at least according to the hard data to date, and so this missing link is waiting for clearer evidence. Add to this uncertainty over the external environment.

BoJ Guideposts Drawn From Empirical Evidence

So, what’s the evidence and when would we expect to see the air being cleared on the transitory versus longer-lived drivers of inflation? How could things turn out to be more dovish or more hawkish? I’m certainly distant from the BoJ but feel that there is still value to offering a framework of thinking that considers the evidence on the drivers of inflation.

BoJ research (example here) has estimated that a one standard deviation movement in the yen (roughly 4%) adds 0.1–0.2% to inflation over 2–8 quarters before subsiding. Over the March 2022 to October 2022 period, the yen depreciated by about 30% to the dollar. If the effects are linear then this would translate into between a ¾% to 1½% lift to headline inflation with the effects gradually working through the system in 2023 into 2024. The effects may not be linear (ie: each standard deviation move in the yen could carry different, possibly greater, effects upon inflation than the prior standard deviation move). The effects may also depend upon what was expected, the duration of the adjustment, and whether it’s fair to take the adjustment over that six-month period in isolation of moves before and after.

BoJ research also says that a one standard deviation in oil prices of roughly 15% would add 0.1–0.3% to inflation inside of a year before subsiding. Over roughly the first half of 2022, WTI oil jumped by about 70% in USD terms (we can’t double count the yen effects). Ergo, that could imply that inflation would be expected to rise by between ½% and 1½% due to oil prices and that this effect should be peaking about now, given that the oil surge has since abated.

If the effects are purely additive (another big if…perhaps they feed on each other…) then the total effects of yen depreciation and oil price increases in 2022 on inflation should be between 1¼% to 3% and spread over a 1–2 year period. The oil price effect should be dropping out first starting over 2023H2 and so whether Japanese inflation eases or not over this period may be critically important to the BoJ.

Ok, so what has happened to Japanese inflation so far? The freshest Tokyo measure is running at 3.2% y/y, up from around 1% toward the start of last year and -1% in 2021. That’s a 2–3% lift depending upon starting points. Much of the inflation that Japan is getting to date has been driven by prior movements in oil and the yen, but all of it? Not if we go with the added lower bound estimates of both the oil and yen effects on inflation, but maybe if we go with the upper bound effects and only if we’re talking over the full 2-year period for both effects to work through. Not if we go with the shorter end of the estimated intertemporal effects (2-quarters for yen effects, inside a year for oil’s effects).

Given that it has only been around a year since these movements at best, given the caveats to this analysis that were noted above and given that the full effects are supposed to be spread out over a longer period than what has happened to date, it is perhaps difficult to pin all of the movement in Japanese inflation that we have seen upon just the yen and oil. Other factors like global supply chain influences may also be factors. Still, I’ll repeat the prior point that at least one of these effects (oil) should be expected to begin dropping out soon; if it does not, then this would suggest something grander is driving Japanese inflation and that may be what Ueda is waiting to observe.

Serial shocks?

But what if Japan is faced with serial shocks to these drivers with each successive wave running the risk of unmooring price expectations? That gets a bit more complicated and is why we need to monitor financial conditions. So far, the evidence for this is pretty muted. Breakevens are all around 1% across varying terms so clearly markets are saying this is all just transitory, yet markets don’t necessarily have the upper hand on forecasting inflation compared to anyone else as we’ve seen in spades throughout the experiences of the past few years.

To assess serial shocks to the drivers of inflation means, in part, looking at the evidence of what is happening to broad financial conditions. One reason for acting now could be to counter an easing of monetary policy conditions based upon the following evidence:

- Some point to the fact that the real policy rate has turned more negative as inflation has risen.

- I think you could make the same point about the fact that the nominal 10-year JGB yield has dropped to under 40bps and hence is no longer testing the upper end of the +50bps band as it was until trouble hit global banking markets in March. So, they could counter such shorter- and longer-term real rate developments.

- Ditto for the currency that has been depreciating throughout this year from about 128 to the dollar toward about 141 now. This risks a new round of serial upward lagging pressures upon inflation. The more such shocks you get, the more you risk seeing expectations rise.

- and the same applies to stocks. The Nikkei has sharply rallied by 25% since about mid-March. Yes, 25%. Ueda had a comment overnight that pinned this on growth expectations. Growth? Where?? Perhaps it’s a Ueda put.

The BoJ could well come to view this easing of financial conditions as inappropriate over time especially if second half inflation persists despite the estimates that point to oil’s effects dissipating over this period.

Further, the annual Shunto Spring wage negotiations established the fastest wage gains in about 30 years. Now the problem here is that it isn’t showing up in the data. Yet. Labour cash earnings are up by only 1% y/y in nominal terms and falling in real terms, but the data only does until April. The shunto wage agreements are estimated to work through wage data over several ensuing months. Hence, whether hard wage growth data accelerates over coming months or not could also be impactful to the BoJ especially if they think it may be more than just a one-off.

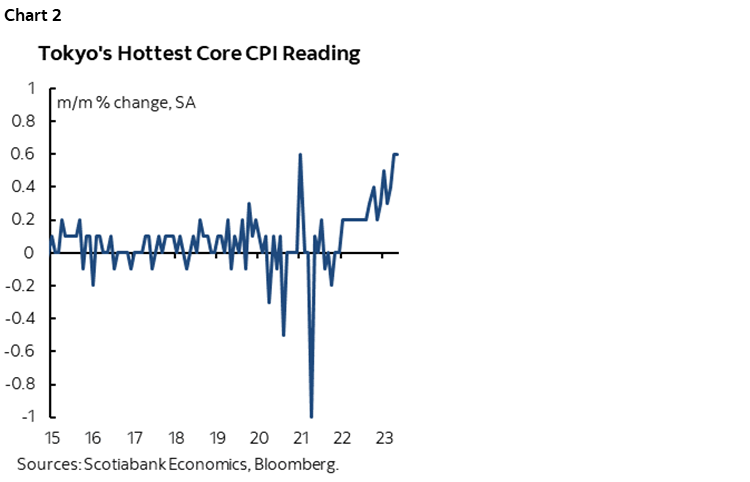

For now, it’s important to acknowledge that Tokyo core cpi recently accelerated to 0.6% m/m SA nonannualized for the hottest gain since January 2021 except this time it’s not a flash in the pan as it was back then (chart 2). This time it’s part of an ongoing upward trend. If month-over-month inflation data persists at such levels and especially if it continues to accelerate while transitory drivers drop out and wage data improves, then this would be of rising consequence to the BoJ over coming meetings and we can’t rule out the possibility that they factor all of this into their forecasts for inflation and discussion of the risks to this forecast when they update projections at next month’s meeting.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.