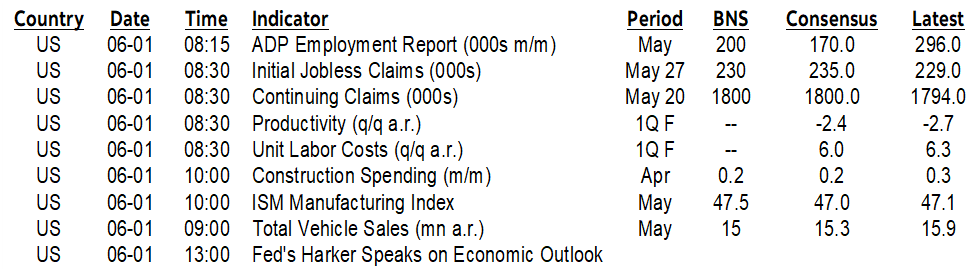

ON DECK FOR THURSDAY, JUNE 1

KEY POINTS:

- Global markets in a cautious mood

- Recent Fed-speak is being misinterpreted as a June pause

- Eurozone core CPI cools for once!

- US debt ceiling anxiety is gone ahead of June central bank decisions

- US unit labour cost revisions drive a dearer US front-end

- US ADP payrolls beat expectations, but offer little by way of a guide to nonfarm

- US job cuts remain low

- US weekly jobless claims remain stable

- US ISM-manufacturing: will transportation add upside risk?

- US vehicle sales are expected to soften along a volatile, improving trend

- Peru’s inflation on tap after Brazil Q1 GDP beats, Chilean data misses

Market sentiment was more favourable earlier this morning but has since turned more cautious. At the time of publication, S&P and TSX futures are flat while gains in European cash equities have diminished to between nothing and 1% in Italy. Sovereign curves have gone from a mild cheapening bias earlier this morning toward being slightly dearer on balance. The dollar is a touch weaker except against the Scandies.

Why? That’s not entirely clear at least to me. US job market readings were generally constructive as explained below. So were European and US inflation readings at the margin. The Hollywood actors who run Congress did the predictable thing by standing down on both sides of their all-too-routine school yard skirmish within a ridiculously dysfunctional political system. Eurozone inflation had little incremental effect when it landed largely because it was already priced in as individual countries released over the prior couple of days.

Sanity eventually prevailed in the US House of Representatives as the debt ceiling vote passed by a 314–117 margin. Now it’s onto the Senate with Senate GOP Leader McConnell suggesting this could happen as soon as today. It should be a rubber stamp sort of affair and then they’ll all have to do something meaningful to earn their pay. This sweeps aside a source of uncertainty ahead of the round of major global central bank meetings over June.

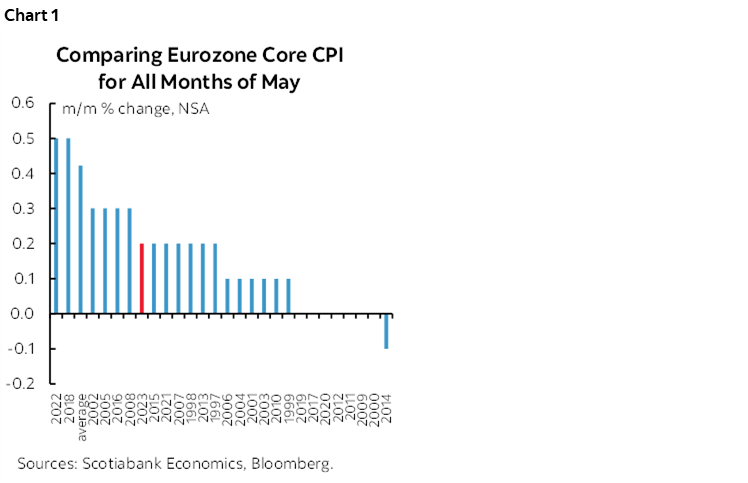

Eurozone core CPI put in an average performance for all months of May (chart 1). It was up by just 0.2% m/m NSA which matches the average seasonally unadjusted gain for all past months of May. That’s significant because even though it’s just one number, it’s the first time this year that this measure has not been above average for all past like months especially readings in April and February that were the strongest readings on record compared to like months. The rest of the figures are less significant as we largely already knew from the individual country releases that headline CPI would be softer than the stale consensus (0% m/m NSA, 0.2% consensus) and that energy was a significant driver.

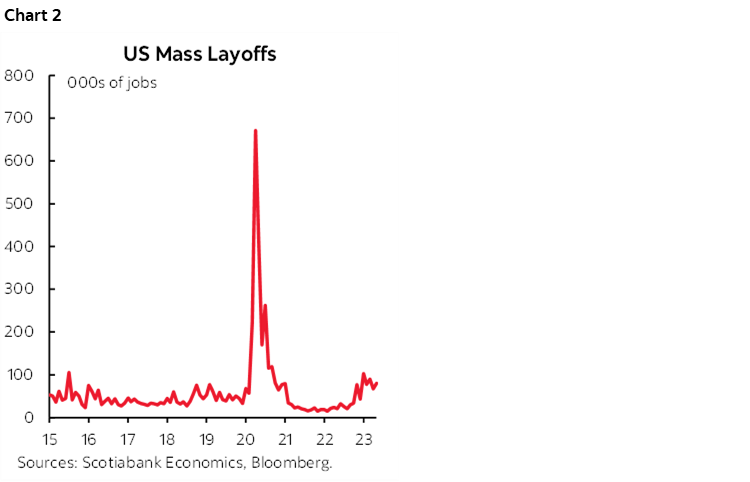

US Challenger & Gray job cuts tallied 80k positions in May. The figure that gets reported is the percentage change in year-over-year terms that might have popped out some eyeballs (+287%) but last May there were only 20k layoffs which is essentially nothing and so it’s a lesson on how sometimes percentage changes carry little meaning. I think what matters is that monthly layoffs remain in the roughly 70–90k zone over the past four months which is not at all incompatible with continued job growth on net (chart 2).

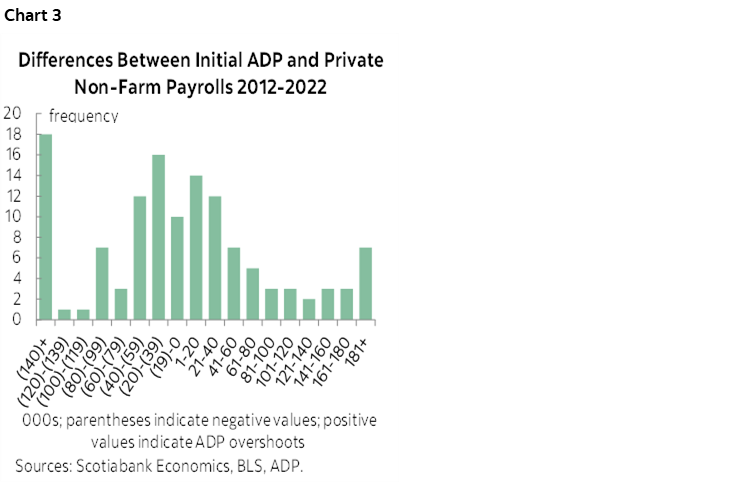

To that effect, US ADP payrolls landed at 278k in May (consensus 170k, Scotia 200k). There is about a 14% chance that ADP would exceed consensus expectations for private nonfarm payrolls that are set at 164k by 114k or more as indicated by this 278k ADP print. This is based upon the distribution of all past spreads between the initial (ie: pre-revision) ADP prints and initial private nonfarm payrolls prints (chart 3). In other words, it is improbable that nonfarm will undershoot ADP by this margin, but certainly not impossible given that ADP throws off a lot of head fakes. In terms of the composition fwiw, leisure/hospitality led the way at +208k, with resources (+94k) and construction (+64k) among other notable assists. Manufacturing fell 48k, finance down 35k, tech down 15k, education/health down 29k etc. This indicates that the rotation continues as some sectors shed jobs while others add jobs. The wage comments are also interesting. They flag slower pay growth for job changers, but still, "job changers saw a gain of 12.1 per cent, down a full percentage point from April." All I saw was 12.1%!! Job stayers saw an increase of 6.5% versus 6.7% the prior month. Both readings are hot, but still, it continues to pay to switch jobs and probably employers. That is either an indication that upon switching, workers' skills are utilized more effectively, or it's a form of market inefficiency at the firms losing these folks and instead incurring hiring training and hiring costs.

US weekly jobless claims landed at 232k and were therefore unchanged from the prior week’s 230k. Data quality was soft, however, as California, Virginia and Kansas all submitted estimates instead of hard data. Initial claims have been moderating since it was revealed that the earlier modest surge was mainly due to fraud in Massachusetts. At 239k, claims are not indicating a notable deterioration of conditions in the US labour market.

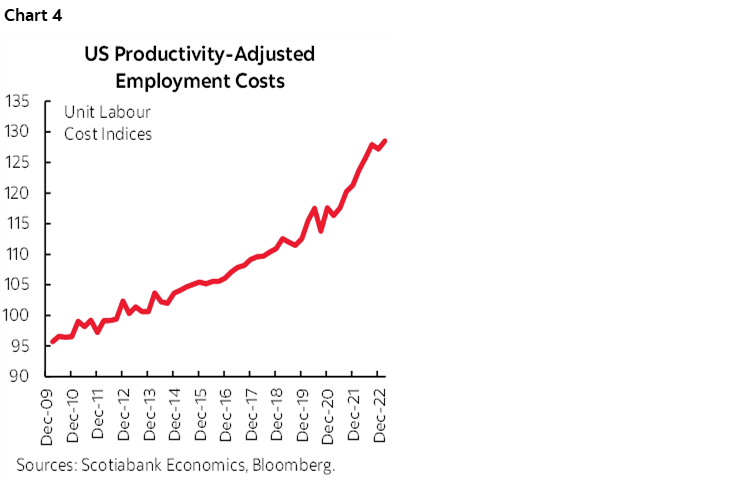

Despite the strong job market signals, it was revisions to US productivity and unit labour costs that drove a dearer front-end in the US Treasury curve post-release. Unit labour costs grew by 4.2% q/q instead of the 6% consensus as the initial estimate was revised down partly via upward revisions to productivity that at –2.1% q/q is still bad. This is not to say that unit labour costs are light; the 4.2% rebound in Q1 from –2.2% in Q4 and the prior 3 quarters that were in the 6.6–8.5% range all point to wiggles along a sharper upward trend in ULCs that emerged in the pandemic (chart 4).

On tap into the N.A. session will be a few additional releases:

1. US ISM-mfrg (10amET): consensus is calling for little change (47 from 47.1 prior, Scotia 47.5). Regional surveys were mixed for the month of May. Transportation sector orders are underrepresented in those regional surveys and may pose upside risk. One caveat to that latter view is that ISM tracks domestic activity versus the S&P mfrg PMI that track global activity by US manufacturers. Since many of the planes ordered from Boeing were from int’l airlines they may not show up as readily in ISM. Supply chain pressures may be informed by orders, backlogs, prices and industry anecdotes, although manufacturing is a modest weight in the US economy versus services.

3. US vehicle sales (e.o.d.) are expected to slip again with industry guidance pointing toward a print of about 15 million at a SAAR pace from 15.91 million in April. The monthly pattern has been volatile, but sales have been trending upward since about mid-2022.

4. Peru’s inflation rate is set for an update (11amET). Chile’s monthly economic activity index slightly disappointed at 0% m/m in April (consensus 0.1%). Brazil’s economy beat expectations a short time ago with Q1 growth of 1.9% q/q (1.2% consensus) and 4% y/y (3.1% consensus).

INTERPRETING FED-SPEAK

The camp that wants to believe that Fed rate hikes are over and done with is distorting impressions about what is contained in recent Fed-speak and in a way that may be destabilizing to markets ahead of significant data risk. The only voting FOMC official that I’ve heard clearly spell out support for a June pause has been Philly’s Harker. What follows is a review of recent Fed-speak.

For starters, did Chair Powell’s comments on May 19th really set up a pause as some are suggesting? Recall that he said “Having come this far, we can afford to look at the data and the evolving outlook to make careful assessments.” When Powell said he’s going to “look at the data” I heard that he’s going to, well, “look at the data” and then decide what to do on a meeting-by-meeting basis rather than having hard set guidance in advance of future decisions. That’s not necessarily a pause signal. Recall that Powell also said in that same event that they haven’t made any decisions about future moves and emphasized they will follow the data at the margin from here forward. Powell’s point is that since they are in restrictive territory now and facing lagging effects of their decisions they can afford to step back from explicit hike guidance and take the decisions one at a time depending upon the evolution of data and events like the debt ceiling agreement’s passage.

Jefferson’s comments yesterday are also being exaggerated by markets and are not necessarily representative of the full range of opinions as noted below in a recap of positions taken by FOMC officials who vote this year. On balance, I think it will come down to the debt ceiling vote, nonfarm, wages, and the next CPI on day 1 of the FOMC meeting.

- Governor Waller: depends on data.

- Governor Jefferson: He said “A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle.” Emphasize “at a coming meeting” and not necessarily June. That’s much more ambiguous on timing a potential pause than the coverage I’ve seen that read what some folks wanted to read as a clear June signal which it was not.

- Governor Bowman: Pointed to rebounding house prices as a challenge to their inflation goals. No comment on next decisions.

- Governor Barr: No recent comments.

- Governor Cook: No recent comments.

- Philly’s Harker: “I am definitely in the camp of thinking about skipping any increase at this meeting, barring what we see in the next few days.”

- Dallas’s Logan: Data dependent. “The data in coming weeks could yet show that it is appropriate to skip a meeting. As of today, though, we aren’t there yet.”

- Chicago’s Goolsbee: Said he doesn’t wish to pre-judge June decision and hasn’t made a decision.

- Minneapolis Prez Kashkari: “We may have to go higher from here, but we may not raise rates quite as aggressively and as quickly as we have over the course of the past year.” Ambiguous on timing and amounts if any. May pause, may not, rates may have to go higher.

As an add-on point, I don’t like the view that is creeping into markets that the Fed can halt and start and halt and start rate hikes in jerky fashion. First, I don’t have much trust for such guidance from a minority of Fed officials since it may just be about trying to manage markets by halting but holding out the threat of hikes they have no intention of delivering. Second, such an erratic path could damage market confidence and confidence in the economy through its effects upon the ability to plan. Third, I still think there is more merit to front-loading as long as the data supports it rather than a fits and starts path forward. If you’re going to pause, then signal a lengthy one as opposed to this nonsense of how well, maybe we don’t go in June, but July could be a live meeting. That’s just muddled thinking imo.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.