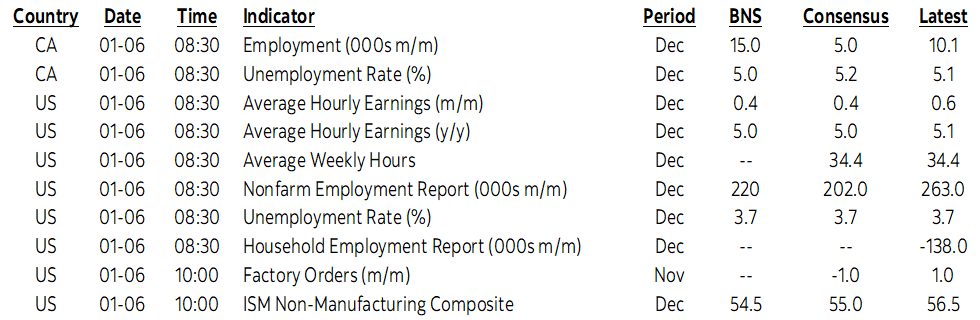

ON DECK FOR FRIDAY, JANUARY 6

KEY POINTS:

- Markets await jobs readings

- In markets vs. Lagarde…

- …choose Lagarde, as markets are misinterpreting Eurozone inflation

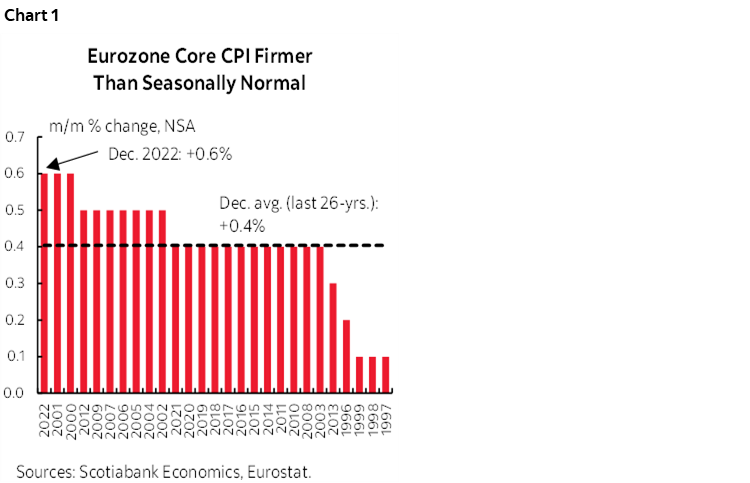

- Eurozone core CPI just posted the hottest December reading in 21 years

- Nonfarm payrolls preview

- Canadian jobs preview

When it comes to markets versus Lagarde, I’d still pick Lagarde and stand by advice I gave earlier in the week about how markets have been sloppily misreading the Eurozone inflation figures. How to properly read Eurozone inflationary pressures explains why (below). Otherwise, it’s obviously jobs Friday with nonfarm the fixation for global markets and with a side order of Canadian jobs for local markets that are key to our footprint.

N.A. equity futures are little changed and European cash markets have a slight positive bias. Sovereign curves have a small cheapening bias on balance. The dollar is stronger against major currencies. Oil is up another few dimes. All of which may soon be irrelevant pending payrolls but first we have the full tally of Eurozone inflation to consider.

Eurozone core inflation posted a hot gain of 0.6% m/m NSA which is a larger than seasonally normal gain. In fact, it’s the largest seasonally unadjusted (as provided) gain for a month of December in twenty-one years! See chart 1. The result lifted the less consequential year-over-year rate (because it’s also influenced by year-ago base effects) by two-tenths to 5.2% which is a new record high.

Headline inflation eased to -0.3% m/m NSA and 9.2% y/y (10.1% prior). That was mainly driven by weaker energy prices including market drivers and subsidy changes and may reverse higher in the next print given, for instance, higher caps rolled out into the new year. For now, the -0.3% m/m NSA reading is abnormally weak and there has only been one other negative December reading since the Euro Area figures began and that was in 2014, but again, it’s an energy-driven phenomenon.

The ECB will focus upon the core gauge. That was my point at the start of the week in advising that markets were misreading the suite of figures across individual countries by just looking at the headline figures which was a totally wrong-footed bias. Even headline inflation is likely to bounce higher in the next report once energy price subsidies adjust.

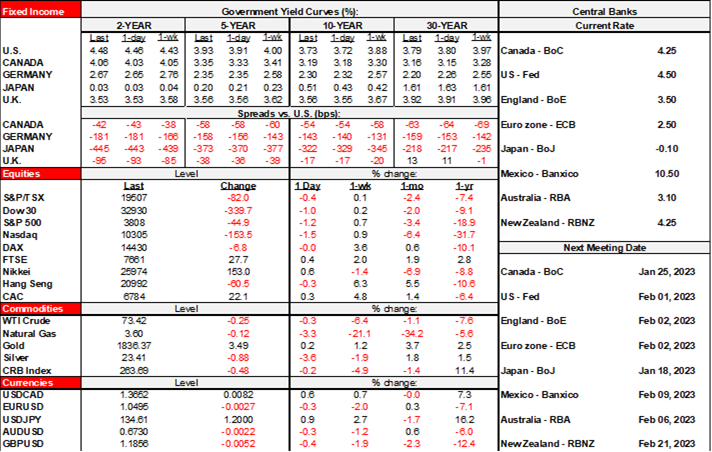

The mild curve cheapening across EGBs that we are seeing this morning is partial recognition of this point. OIS is pricing most of a pair of 50bps moves at the next two ECB meetings on February 2nd and March 16th and a terminal rate approaching 3 ½%. That’s a little higher after this morning’s eurozone tally, but still lower than before markets began misreading the CPI readings out of Spain, Germany and France starting last Friday.

Nonfarm Preview

I think the market reaction to yesterday’s ADP has taken out much of the potential for further reaction to upside risk to today’s payrolls (8:30amET) and may slant the market risk more toward any downside miss whether statistically significant or not. The second look could focus upon wages following the prior month’s 0.6% m/m SA non-annualized gain that was the fastest since January.

Nonfarm payrolls, m/m 000s, SA, December expectations:

Scotia: 220

Consensus: 203

Range: 70k – 350k, clustered within about 170–240k. Approx normal distribution.

Median/average: 203 / 206 (so no clear skewness)

Shadow estimate: 237

Std dev: 39.4k

90% C.I.: +/- 120k

UR: 3.7%

Wages: 0.4% m/m

Most of the readings that I look at in the suite of evidence suggest that job markets remained pretty solid in December. That’s never a guarantee in that nonfarm has a fair amount of statistical noise around it and relatively underrepresents small businesses that don’t necessarily have formal payrolls and that are more likely to be capture by the household survey figures. Here’s the run down of the conventional measures.

- Initial jobless claims were little changed between reference periods (slightly lower).

- ADP suggests statistically insignificant upside risk to nonfarm, but shaky (see morning note).

- JOLTS job openings are holding firm at around 10.5 million vacancies. Key issue is how many are zombie postings (ie: no intention to fill, or backburnered).

- NFIB small biz hiring plans fell to the lowest since January. This is more likely to possibly affect the household survey that includes more small biz than nonfarm payrolls. NFIB job openings hard-to-fill also fell and in this case to the lowest level since February 2021. That could be because mobility picked up a bit with the same JOLTS readings pointing toward a slightly higher quit rate that is holding at elevated levels.

- consumers signalled that jobs were easier to get in December as the consumer confidence gauge for ‘jobs plentiful’ increased following a general downward trend since March to still elevated levels. Watch seasonal hiring.

- ISM-mfrg employment returned to positive growth (51.4 from 48.4 and hence above 50) but manufacturing is a small part of the jobs picture versus services and we don’t get the ISM-services reading until after payrolls tomorrow.

- On layoffs, I’ve tallied about 43,500 across all sectors between nonfarm reference periods. That could dent payrolls since they fall into the unemployed bucket, but among the uncertainties are that it’s difficult to tell the difference between announcement and implementation effects. It’s also difficult to tell the split between temp and permanent layoffs before we see the payroll figures.

Canadian Jobs Preview

As for Canada’s jobs report (8:30amET), there is even less to go by in terms of advance readings than the US figures.

Canadian jobs, m/m 000s, SA, December expectations:

Scotia: 15k

Consensus: 5k

Range: 0–15k, spread evenly

Median/average: 5/7 (ie: no skewness)

Whisper: n/a for Canada

Std dev: 5

95% CI: +/-57k

UR: tick higher to 5.2 / but Scotia 5.0 (I’ve gone with a reversal of the prior month’s decline in the labour force)

Wages: No consensus.

In terms of BoC implications, this is part of the hat trick of reports to watch over the next dozen days including the BoC surveys on the 16th and CPI the next day. Governor Macklem and DepGov Kozicki made it very clear that the next move would be informed by data and their discussions and forecasts into the January decision and so this batch of readings will determine whether another hike is on offer this month.

Canada’s job market remains extremely tight. Tighter than the US on multiple measures. Canada has been posting slight real wage gains since May as the SA level of nominal wages has been trending a bit faster on an indexed level than headline CPI over this period. Wages in m/m SAAR terms have averaged 8% growth on an average monthly basis from May to November this year. Major wage settlements data lags behind a bit but the October figures were registering 1st year wage hikes of 4.3% and full contract period average gains of 3.9%. That average annual wage gain over the full contract period of 3 years on average is trending to its fastest since pre-GFC times. Public sector wage settlements including Ontario’s appeal in progress could drive this higher and retroactively so as well.

Going forward, we expect real wage growth to accelerate this year as nominal wage gains remain strong and headline inflation moderates. Toss in tumbling Canadian labour productivity over the pandemic and the combined effects are inflationary on both counts.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.