ON DECK FOR WEDNESDAY, JANUARY 25

KEY POINTS:

- Tech earnings drag on risk appetite

- BoC: Why not hiking and/or a firm pause would be a setback to fighting inflation

- Four BoC scenarios

- RBA hike bets intensify after inflation surprises higher

- BoT hikes with hawkish guidance as tourism recovers

- US mortgage purchase applications continue to climb as 30-year rate drops

- Fed could lose a senior, politicized dove…

- …throwing the Fed’s #2 spot into turmoil once again

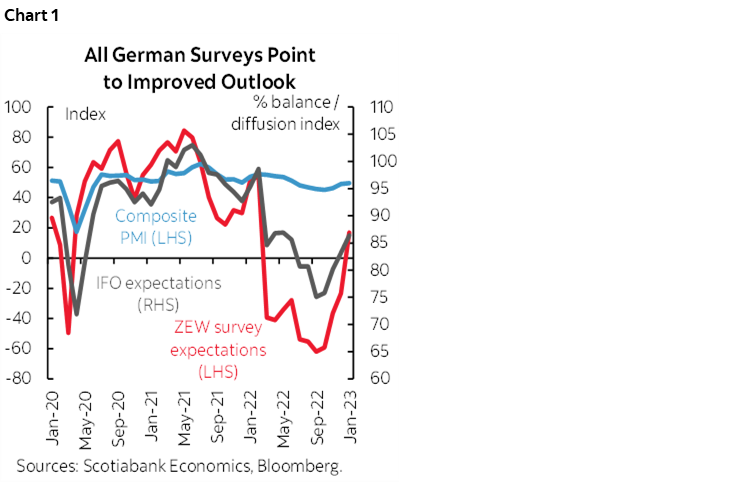

- IFO completes the sweep as all 4 German surveys improved

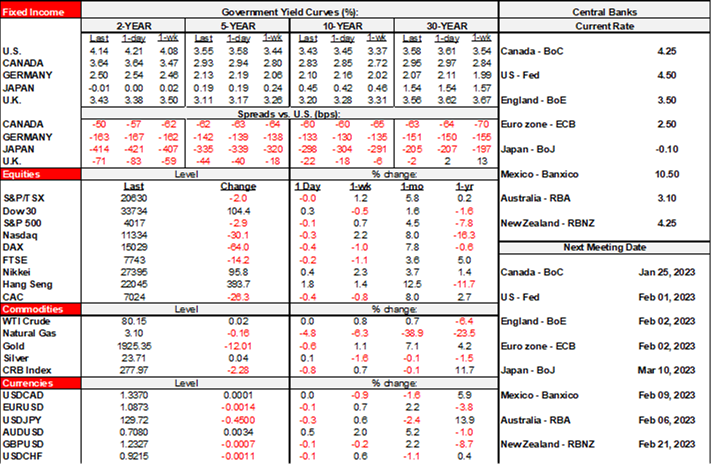

US tech earnings and three central banks are the focal points this morning with the BoC being nearest-and-dearest to many of us. Microsoft’s release last evening is contributing toward a drop in US equity futures with the S&P off ¾%. TSX futures are almost ½% lower and European cash markets are down by up to ½%. Sovereign bonds are generally picking up some safe haven flows as curves richen especially in Europe but with Australia’s curve getting hit by CPI (see below). The USD is little changed as strength in the A$ (CPI again) and yen, little change in CAD and some softness across European crosses are offsetting one another.

The RBA got an inflation jolt that reset rate hike pricing higher and the BoT hiked with a hawkish bias. Germany’s final soft data release completed a suite of four improvements across consumer confidence, ZEW investor expectations, PMIs and now IFO business confidence as all sources of opinions across different classes of respondents point toward less downside risk in Germany’s economy (chart 1).

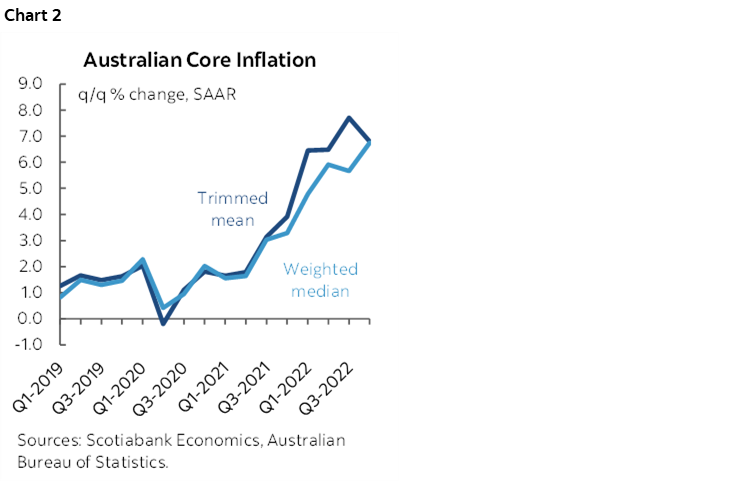

As we await the BoC, Australian inflation serves as a warning to central banks counting on inflation just rapidly going away. RBA bets heated up and drove sharp underperformance across the Australian rates curve while driving the A$ to the top of the class. The culprit was hotter than expected inflation readings. December’s CPI jumped 8.4% y/y (7.7% consensus, 7.3% prior) with core up 8.1% y/y(6.7% prior) and was up 0.9% m/m SA or over 11% m/m SAAR. A major driver of the m/m surge was holiday travel and accommodation (+27% m/m SA). The ABS has suspended publication of the monthly trimmed mean CPI measure out of concern it does not adequately line-up with quarterly trimmed mean CPI. The somewhat narrowly driven surge in m/m CPI might suggest that had there been a trimmed mean measure then it might have weeded out the hotter components. Still, inflation for Q4 overall was up 8.4% y/y (7.7% consensus) and 1.9% q/q SA non-annualized (1.6% consensus). Trimmed mean CPI was up 6.8% q/q SAAR and weighted median CPI was up 6.7% q/q SAAR and hence far above the RBA’s headline CPI target range of 2–3%. See chart 2 for the trend.

And so, markets reacted by upping pricing for the February 7th meeting to closer to a full quarter point hike and raised terminal rate pricing by about 17bps to 3¾% from a current policy target rate of 3.1%.

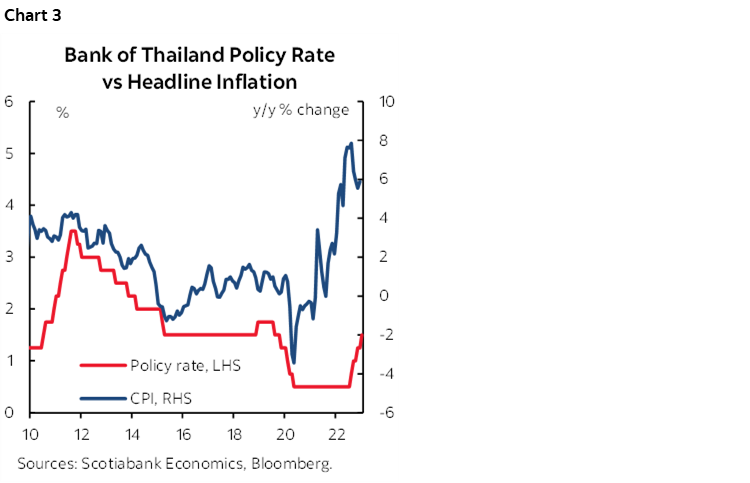

The Bank of Thailand is another hiking central bank and added 25bps overnight to raise its benchmark rate to 1.5% in a unanimous decision while saying “it’s still appropriate to raise the rate for while.” The BoT was a lagging central bank held back by the collapse of its tourism sector that is now rapidly recovering while inflation has picked up. Chart 3.

The US posted its second weekly gain in the mortgage purchase index, up 3.4% w/w after the prior week's 24.7% w/w rise. Refis are also still rising (+14.6% w/w after 34.2% w/w rise the prior week). The purchase index is back up to August levels which isn't great but this winds the clock back several months as Americans take advantage of declining 30 year mortgage rates following the start of the rally in US 10s last October with the buyback trial balloon that's now dead but replaced by the debt ceiling ruckus.

There is nothing else due out today in the US and with the Fed in blackout. Vice Chair Brainard may depart the Fed to head up the National Economic Council (here). She has had an embarrassment of riches foisted upon her through options presented by the Biden administration ranging from potential Treasury Secretary before choosing Yellen, the Fed’s #2 spot she now holds, and now this. Brainard is overtly political in her role as a staunch Democrat who supported Hillary Clinton who donates to the Dems and has long been a favourite within the party. Her departure would open up yet another search for a top role and—depending upon her potential successor—would remove a moderate/dove and critic of the financial industry. Her successor would have to clear the Senate that the Dems barely control in deeply divided Washington and depending upon how Manchin and some others choose to align themselves.

Bank of Canada—Final Thoughts

The BoC is the full deal today with the statement and MPR including fresh forecasts due at 10amET, and an hour-long press conference spanning from about 11am until noon including an opening statement. They will start to publish minutes with this meeting as announced last year, but they won’t be available until February 8th and I have low expectations for them in any event. I’ll be amazed if the group culture at the BoC suddenly pivots toward being much more transparent.

+25bps is the house call. It’s mostly priced. All of the big 5 bank econ groups expect a hike. Of the rest, 5 out of 27 expect a hold. Full rationale is provided in multiple publications.

Risk-reward puts more risk on a surprise hold than reward to a hike. How they play the bias is also important with scenarios offered below.

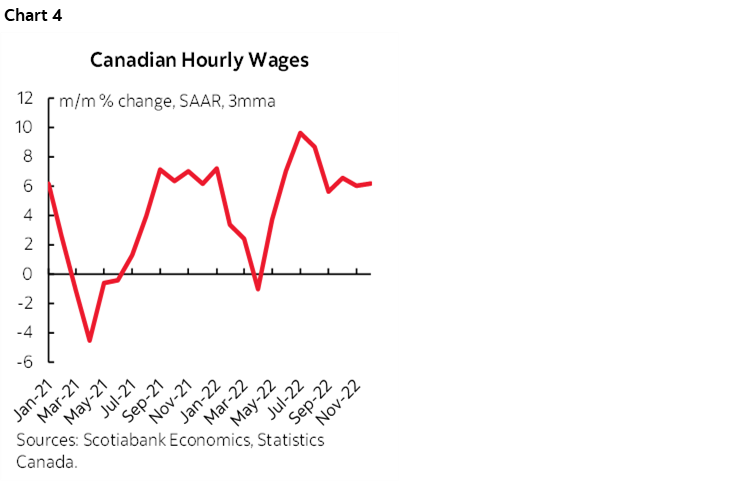

What plays to both the imminent decision and the bias is how to interpret the line in the December statement when they said they “will be considering whether the policy interest rate needs to rise further.” Some took that to mean they were done, but both Macklem and DepGov Kozicki said they meant they were fully data dependent. We’ve also since gotten a ripping jobs report, fairly resilient core inflation, Q4 GDP tracking a full point higher than they forecast and generally less pessimism toward the global outlook pointed at China and Europe and aided by easier financial conditions. Core inflation is still tracking above target and the next phase of inflation worries is partly focused upon the job market as trend wage gains and awful worker productivity trends reinforce one another in terms of the inflationary implications (chart 4).

I interpret that line to instead be a sign they would let this meeting be guided by data while teeing up a possible pause after this meeting when they have the opportunity to provide a full sales job, numbers and all. The line is likely to be replaced by something that more directly alludes to a pause at least for a time. I would prefer that they keep their bias data dependent.

Open to other thoughts but here’s my guess at scenarios.

- Hold and signal pause: get out the rally monkey! Heap on even more cut bets. I think this would be the most ill-advised scenario but the one that pays off the most. Markets would have their ‘gotcha’ moment with Macklem getting weak kneed. So, the reverse logic argument against a hold is that it’s highly premature to go out of your way to drive easier financial conditions. If they do, housing rips, inflation resurfaces, and they’re back at it all again later imo.

- Hike and signal a soft pause: Repeat that they remain prepared to be ‘forceful’ if they get surprised to the upside of developments. This might not be a bad compromise and largely priced in OIS but there would still be some uncertainty around whether they are done which might restrain any front-end pile-on.

- Hike and signal a hard pause: This could drive a modest front-end rally imo on the conviction the BoC would signal that it’s sure it doesn’t need any further tightening and this may be taken as a sign they’re worried if they have such a high degree of conviction.

- Hike and remain data dependent toward future moves: This would probably drive a sell off at the front-end with nothing priced by way of hikes after today. This is what I would do if I were them.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.