ON DECK FOR TUESDAY, JANUARY 24

KEY POINTS:

- Markets uneasy as US tech earnings start tonight

- Global PMIs: 3 out of 4 ain’t bad

- Stopping BoC rate hikes because it might damage jobs…

- …entirely misses the point…

- …and might be ignoring today’s more complex drivers of job markets

A mild risk-off tone is being applied across asset classes this morning. I think a significant driver is nervousness into US tech earnings given uncertainty behind the degree to which layoff notices portend earnings gloom. Microsoft kicks it off in the after-market today and it accounts for around 5% of the S&P, second only behind Apple that arrives next week along with Meta, Alphabet etc.

Otherwise, the flow of macro information is incrementally positive. A batch of global PMIs generally improved in 3 out of four countries’ cases with the UK being the sole exception perhaps as that country continues to grapple with the negative terms of trade shock arising from its Brexit and failure to achieve freer trade agreements. Two of the countries climbed back above 50 readings for their composite PMIs that divide expansion (above) from contraction (below), but only barely so.

In general, the readings tentatively support the narrative that favours less downside risk to the global economy than thought a short time ago. There is a lot of new information to inform fresh forecasts into the new year including a better starting point for the US economy that appears to have blown away expectations for Q4 GDP, developments in China that pivot from near-term downside toward better prospects as the year unfolds, less of a European energy shock than feared and easier financial conditions on balance. We should all be looking at forecast upgrades for major regions of the world economy by way of incremental changes toward less negativity.

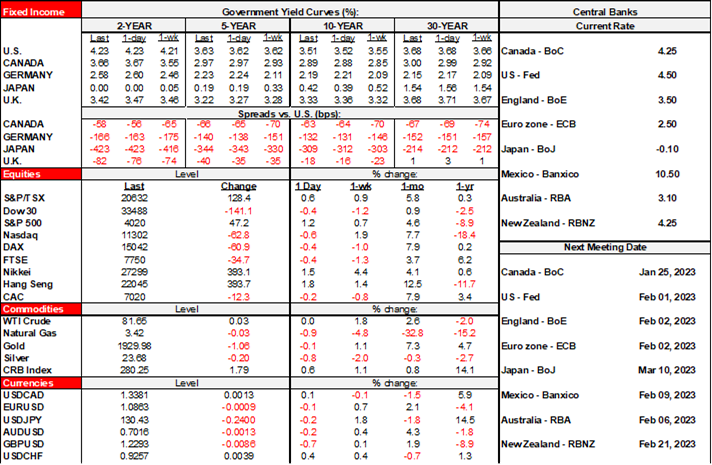

Still, with some modest exceptions, that generally wasn’t enough to impress markets that may have already digested at least some of the main takeaways from the PMIs. N.A. equity futures and European cash markets are all slightly in the red, and while most of Asia is shut, Tokyo was up by about 1½% partly on stronger PMIs. Sovereign bonds range from flat US Treasuries to slightly richer European benchmarks. The USD is little changed as yen strength (again, PMIs) and a firm CAD ahead of the BoC tomorrow offset weaker sterling (weak PMIs) and other European crosses plus MXN.

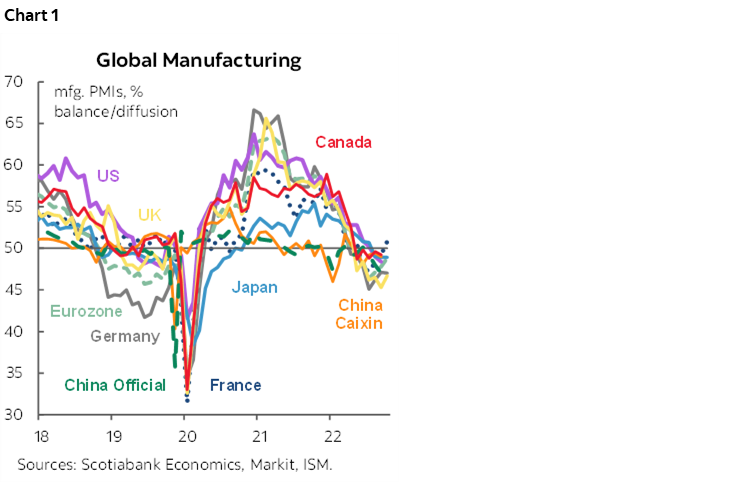

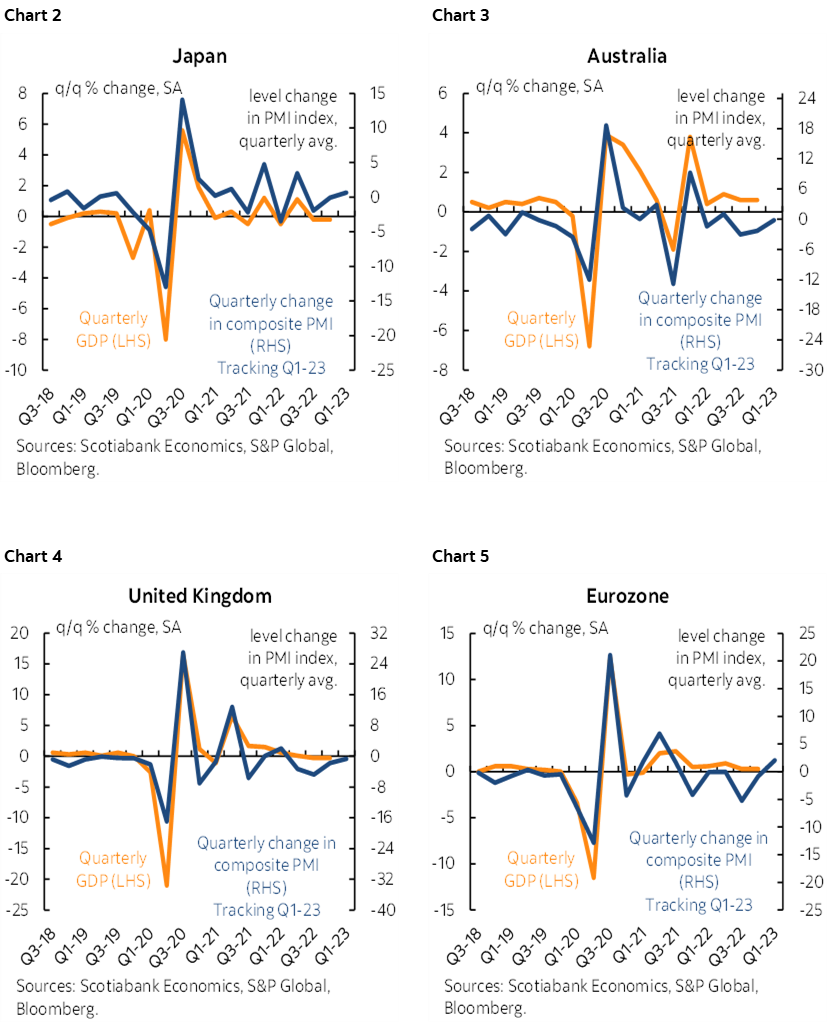

Here’s the PMI round-up and also check out charts 1–5.

- The UK composite PMI (here) fell 1.2 points to 47.8 entirely due to weaker services (48 from 49.9) as manufacturing’s contraction ebbed a touch (46.7, 45.3 prior). All were sub-50 readings and so they contracted. Weaker current output mostly in services drove the deterioration but business expectations for the year ahead improved. Input cost inflation eased for a second month as lower fuel prices offset higher wages. Output prices nevertheless increased but at its softest pace since August 2021. Employment softened a touch.

- The Eurozone composite PMI (here) climbed to 50.2 from 49.3 as both services (50.7, 49.8 prior) and manufacturing (48.8, 47.8 prior) improved. We only get the breakdown for Germany and France at first, and it was Germany that drove the gain. Across the eurozone, output increased after four monthly decreases and business expectations for the year ahead improved by the largest amount since June 2020 in the initial stages of the recovery. New orders and backlogs fell for a seventh month but at a slowing pace for both. Input costs climbed but at the slowest pace since April 2021. Output prices rose at a quicker pace than the prior month. Employment growth picked up to the fastest rate in three months.

- Japan’s PMIs (here) also improved to 50.8 from 49.7 entirely due to services (52.4 from 51.1) as manufacturing held unchanged at 48.9.

- The Australian composite PMI (here) climbed 0.7 pts to 48.2 as services PMI jumped a full point but manufacturing slipped 0.4 points. The overall composite gauge contracted at the slowest pace in three months. Output slipped, but new orders returned to growth. Hiring was up. Input and output prices increased.

The US releases S&P PMIs at 9:45amET and we’ll see if they follow the general global pattern while nevertheless being the Fed’s least preferred measures (versus ISM) because today’s batch covers global operations of US firms and not just domestic operations. The Richmond Fed’s manufacturing index for January will also be released 15 minutes later.

CANADIAN JOBS AND THE BANK OF CANADA

The same old narrative has resurfaced on the eve of the Bank of Canada’s decision that posits they shouldn’t be hiking because it will weaken the job market. I think this narrative is extreme and worth pushing back against. Some of the points offered below will draw upon points I’ve previously made such as here.

Ya Missed the Memo!

First, the logic that you shouldn’t hike because it might slow, or reverse job gains is an entirely false starting point to begin with. It either reflects a poor understanding of macroeconomics and monetary policy or it seeks to opportunistically politicize opposition to what the Bank of Canada is trying to do in bringing inflation under control and either way is unflattering.

That’s because one reason for hiking as part of an effort to cool inflation is to open up some slack in the economy and in the job market. In an augmented Phillips curve framework, a contributing driver to softer inflation has to be some slack in the job market such as through a higher unemployment rate compared to multiple measures of historic tightness at present. That can mean either slower employment gains relative to growth in the workforce or outright employment declines.

We don’t know the degree to which this relationship holds among other drivers as the sensitivities can change over time and under different conditions and is hard to observe, yet there is a great deal of evidence to support the existence of some degree of inverse relationship between inflation and the UR over time.

Canada’s job market is on fire and if it isn’t cooled down then there will be less chance at successfully bringing inflation durably lower. Employment is at a record high. The unemployment rate is at a record low. Canadian labour productivity now versus 2019 is terrible and among the worst in the world. Trend wage pressures are rising. Job vacancies are still over 900k and hence nearly double pre-pandemic levels. All of that is hardly a recipe for getting inflation under control.

Higher Borrowing Costs Long Preceded BoC Hiking…

Second, the timing of higher borrowing costs is still wrongly depicted as having only started in March of last year when the Fed and BoC finally started to lift off. Market-driven borrowing costs were rising well in advance of this because markets were not believing central banks as they dragged their feet and took forever to wake up to inflation.

Canada’s 2-year yield began more aggressively pricing BoC hiking in October of 2021 and had risen 125bps off the ¼% trough before the BoC even launched its first rate hike. We’re now a cumulative 340bps higher on the two-year yield from the trough. Rates have been rising for about 15 months or so but are now pricing aggressive BoC policy easing. If such policy easing is delivered or further amplified by a pause tomorrow, then in my opinion, we risk landing back in heated housing markets within persistent inflation risk and tight job markets driving cost and inflation pressures.

…And We Should Have Seen Negative Effects on Jobs By Now

Because market rates were rising long before the BoC hikes, we arguably should already be seeing the lagging negative effects on employment growth at least in terms of decelerating gains by now. The opposite is happening as employment growth accelerated with nearly a quarter million jobs created in 2022Q4 and 104k of that in December. Accelerating employment growth requires us to think a little more carefully about what is going on which the rest of the points will attempt to do.

The ‘Noise’ Factor is Improbable

Some say meh, it’s the Labour Force Survey, get over it. It’s noisy. It’s unreliable. It has been wonky at times in the past with weird revisions sometimes due to errors. You wouldn’t want this approach to be your default in my view. Given that the Labour Force Survey’s monthly gains occur within a 95% confidence interval of about +/-57k you can’t just dismiss several months of strong gains as a statistical anomaly; it’s not impossible that it’s noise, but it is highly improbable. Therefore, when something like that Q4 pace of job growth happens you never want to over-react, but you should entertain possibly new ways of thinking in open-minded fashion.

Too Much Support?

So one possibility is that while public policy did many of the right things in supporting the economy, the job market and financial markets in 2020, perhaps Canada did too much of it with generous coverage of small business rent, employment costs and with hiring incentives. That might have prevented the labour market from adapting to changed drivers of the economy.

Hire More Slackers

The cost to not allowing some degree of adjustment in the labour market has arguably been productivity. Canada has had basically the worst productivity performance—defined as output per hour worked—of any peer group economy since the pandemic struck. If new hires are producing less per new hour worked now than in 2019, then maybe you need to hire more to achieve the same incremental output now that you would have gotten from new hires in 2019. That’s a plausible shorter-run explanation of job growth but hardly the road to riches over the longer haul in terms of competitiveness.

Improving Supply Chains

Another possibility is that despite concern toward the outlook, improving supply chains are making it possible to produce more and with that goes a need for more inputs like workers. ‘Normal’ downturns in the past are not accompanied by an improving supply side of the economy.

Variable Over Fixed Costs

To meet the needs of improving supply chains and more inputs, businesses today may have a preference toward hiring more workers (and hence adopting higher variable costs) than investing more in machinery and equipment (that would raise fixed costs) given the uncertain climate. It’s easier to adjust variable costs if the economy really nosedives and more painful to be stuck with fixed charges like financing and depreciation.

Can’t Let Them Go!

Another possibility is labour hording in a very different job market now than decades past. Domestic sources of growth in the supply of potential workers are weaker now than in the past when boomers and their kids were entering job markets. Today, absent such influences, letting go of workers might mean never getting them back in a structurally tight market.

Too Early to Tell with Immigration

I don’t find much evidence that immigration drove Q4 job growth or job growth over a longer period, but it might in future. Some of the surge last year was taking people already here and catching up to processing and the composition of employment gains did not line up with categories that often attract new arrivals like the professional/scientific/technical category of employment, or self-employment, or the trades among others.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.