ON DECK FOR WEDNESDAY, JANUARY 18

KEY POINTS:

- Global yields pushed lower by BoJ inaction

- BoJ douses tightening talk…

- …prompting JGBs to richen, yen to soften

- UK core CPI surprises a touch higher

- US macro reports drive further bond rally...

- ...as US retail sales disappoint, eyes on total spending including services...

- ...US core producer prices sticky, but total prices slipped more than expected...

- ...and US industrial output slips, Fed’s Beige Book on tap

- Excessive bearishness toward Canadian housing?

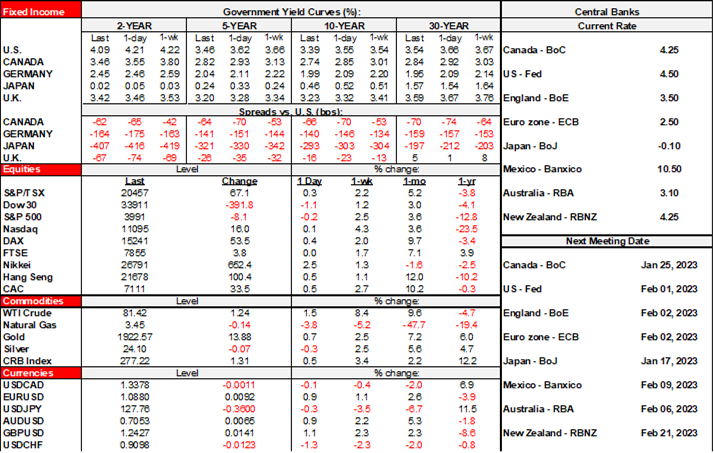

JGBs richened across the curve especially toward 10s with the yield undershooting the ceiling by about 10bps following the BoJ overnight (see below). That carried a bit of a ripple effect across other Asian markets overnight and through carry spilled over into increased appetite for US Ts and Canadian govies this morning with US data amplifying the moves (see below). UK inflation had an otherwise relatively dampening effect on demand for gilts but not enough to fully thwart a mild richening bias (see below). Otherwise there is also a speech by China's Vice Premier Liu He to consider; he told Davos that China has returned to normal and is exiting Covid. That’s a bit punchy at this stage, but he’ll probably be proven right as the year unfolds.

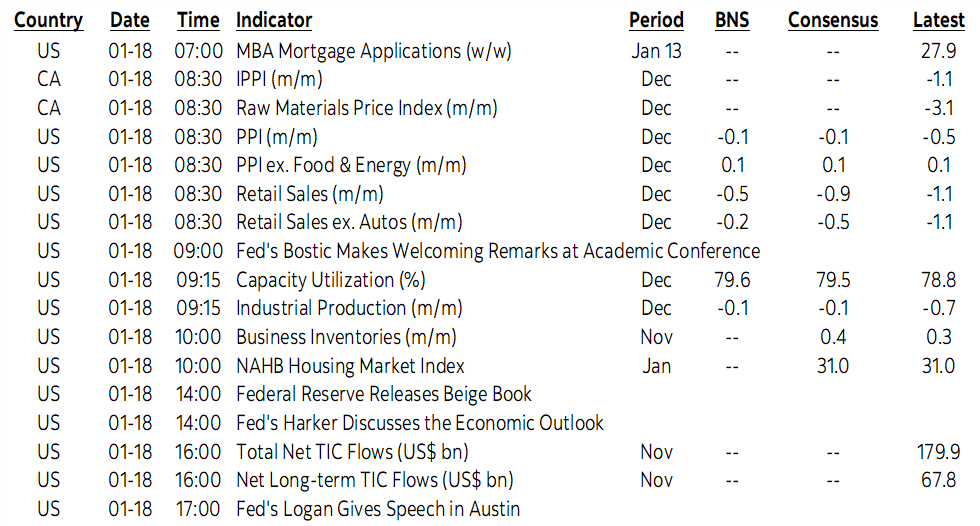

The Bank of Japan stood its ground and did nothing overnight. Kuroda told everyone to calm down, go home and walk the dog. The BoJ’s policy rate and yield curve control remained unchanged. There had been some wild speculation that December's widening of the 10-year yield target range to 0+/-50bps instead of 25 was a precursor to further changes. Not. Kuroda had emphasized in December that this was not an effort to reduce stimulus and was instead designed to improve JGB market functioning. He further emphasized this point in his press conference and went one step further. Revised forecasts show that the BoJ continues to look through transitory upsides to inflation via past oil and yen movements. The CPI forecast continues to show inflation resting below the 2% target in future (chart 1). If there is change afoot at the BoJ then it would likely have to come through Kuroda's successor in April and a potential policy review. That too seems unlikely given the 9–0 vote in support of the decisions just taken.

UK core CPI inflation was a little stickier than consensus expected. It held firm at 6.3% y/y against the median call for 6.2%. Headline CPI also surprised a touch higher at least in m/m NSA terms at 0.4% versus consensus that was a tick lower.

December’s US retail sales (8:30amET) fell by 1.1% m/m in nominal terms. Softness had been expected as auto sales volumes and gasoline prices fell, but there was more to the weakness than just that and a caveat to consider. Sales ex-autos and gas also fell by 0.7% m/m with a negative revision to the prior month that is now at -0.5% m/m instead of -0.2%. The key retail sales control group that excludes autos, food, building materials and gas and serves as a guide to what drives total consumption in GDP accounts also fell by -0.7%. The caveat lies in the fact that retail sales are under half of total consumption with the other half represented by various types of services spending. It seemed to me that restaurants, bars, airlines and hotels were pretty busy over the holiday season and so perhaps there was a substitution toward that kind of spending that we will learn more about with hard figures toward month-end.

US producer prices eased by more than expected for headline but core was sticky. Total producer prices fell 0.5% m/m in December with PPI ex-food and energy on consensus at 0.1% m/m albeit with a negative revision to November (+0.2% m/m instead of 0.4%).

US industrial production also fell, by –0.7% m/m (consensus –0.1%). Capacity utilization fell by six-tenths to 78.8%. The drop was driven by manufacturing that fell 1.3% m/m.

There is nothing out in Canada today of any real consequence after yesterday’s CPI and the prior day’s BoC surveys (recap here). There remains a consensus pile-on of Canadian housing haters. I still think they are too bearish toward the path forward beyond just now and this bias is infecting debates on whether the BoC should hike further. Consider the following points as reminders of a narrative that cautions against just following all of the shorter-run bearishness and that favours a future rebound.

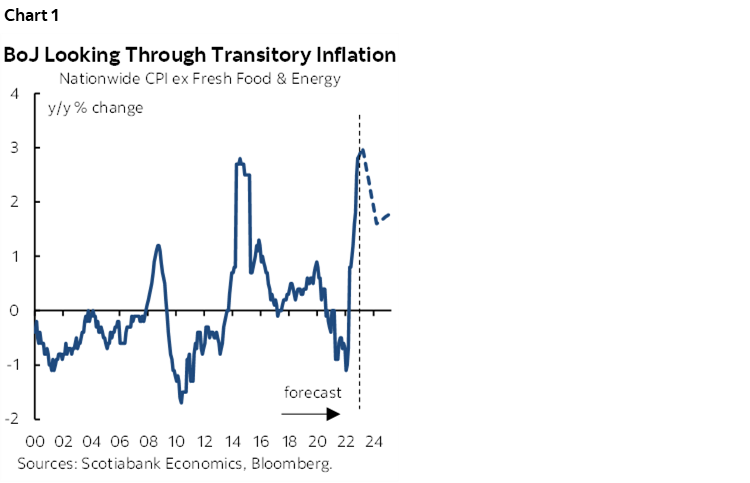

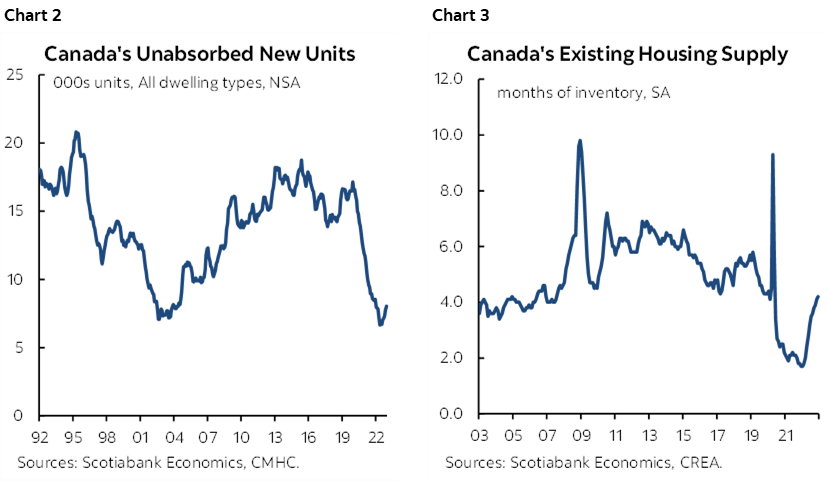

1. There remains no product to buy. Unsold new home inventories are at rock bottom levels (chart 2). Existing home inventories have been rising but so far remain below the historical average as a listing strike serves to counter softening sales (chart 3). Canada needs to expand the housing stock, but homebuilders can’t keep up now, let alone with what lies ahead.

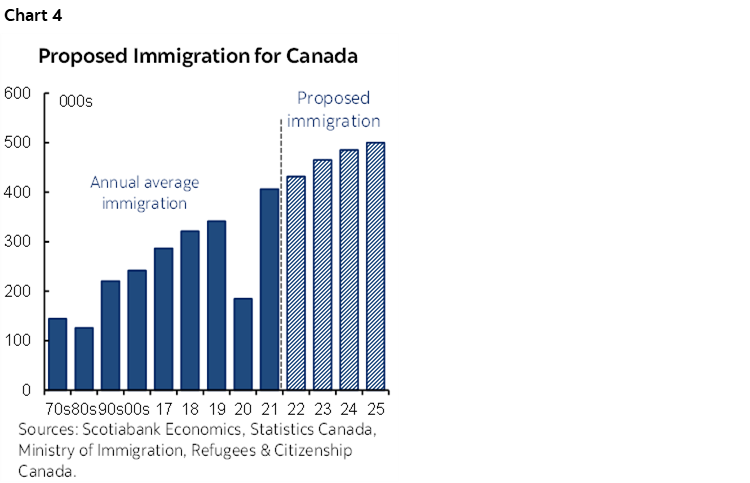

2. Higher immigration might help on both the labour and homebuilding fronts. The surge is basically adding the equivalent of a new City of Ottawa or City of Edmonton roughly every couple of years. Chart 4. The challenge lies in the fact that they tend to overwhelmingly go to the biggest cities. Canada has the fastest growing population of any peer group economy out there. I’m also a fan of shocking the system and then letting the players adapt, rather than waiting for everyone to be fully prepared with plans for infrastructure and housing supply which would be highly unlikely to ever happen. There’s work to be done and little to be gained from fighting it as the rewards to pulling it off will go to the builders and regions that successfully adapt.

3. A key driver of mortgage borrowing costs is already plummeting and if the BoC chickens out next week with a pause then it will rally further and perhaps back to yields unseen since early Spring of last year. The 5-year Government of Canada bond yield has fallen by about a full percentage point since the peak last October. It feeds into the important 5-year fixed mortgage rate. The folks who are constantly harping on about higher Canadian debt and rate sensitivity are talking like it’s last October with the peak in yields; as bond markets rally, perhaps the reverse argument begins to hold with Canada faces relatively greater upside on the heels of such market movements.

4. There are not enough folks in consensus who are acknowledging how wrong we’ve all been on Canadian jobs to date. You can’t just ignore or talk through the data when it’s blowing the confidence bands around estimates. The common narrative was that the lagging effects of higher market-driven borrowing costs (like 2s and 5s) would drive a deceleration of job growth and perhaps outright losses by now. That might eventually come true I suppose, but if it does then it’s coming off higher and higher peaks and in any event, the opposite is happening so far. Job growth has accelerated with almost a quarter million jobs created in the final quarter of 2022. Incredibly tight job markets are fanning wage pressures.

5. First time home buyers have been saving up down payments as prices ease off of their peaks. This is a double whammy in favour of greater purchasing power in the housing market.

To sum up, if we’re not careful, then we’ll be back at 25% annual house price gains before you know it. The housing bears routinely fall into the trap of being too bearish toward the weakest soft patches only to wind up wondering gosh golly gee-whiz how did things recover so quickly?! The BoC should bear this in mind when it sets monetary policy because anything it does that allows financial conditions to ease further could complicate its inflation fight beyond the fixation on the latest month’s data and toward the fuller cycle ahead when there is already a strong case to be made for how the inflation regime has pivoted toward more upside than downside risk compared to the period between China’s WTO entry and the pandemic.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.