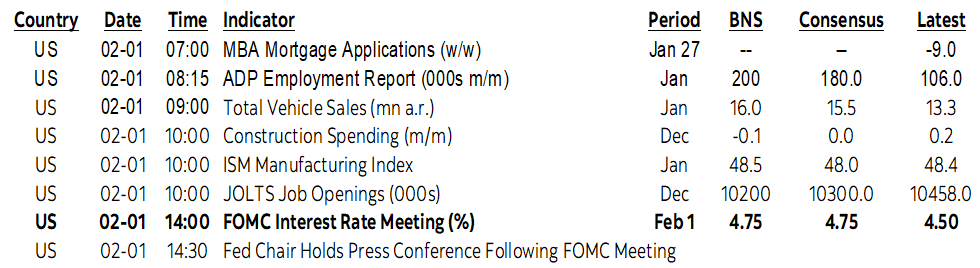

ON DECK FOR WEDNESDAY, FEBRUARY 1

KEY POINTS:

- Global markets await the Fed

- The Fed’s Great PivNot Redux

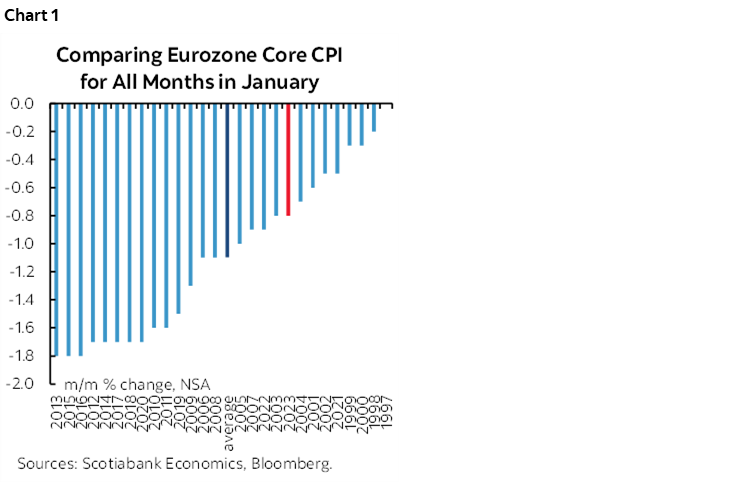

- Eurozone core CPI was hot…

- …but data quality issues fade its relevance

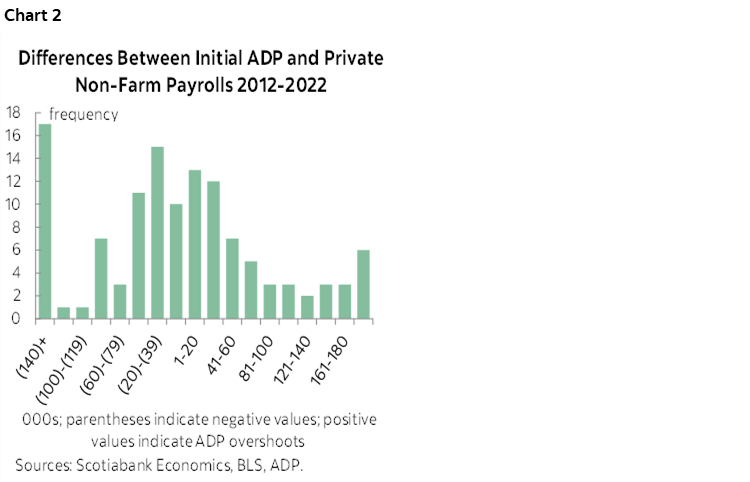

- ...as ADP offers improbable but not impossible guidance toward a soft nonfarm reading...

- …ahead of ISM-mfrg, JOLTS, construction and vehicle sales

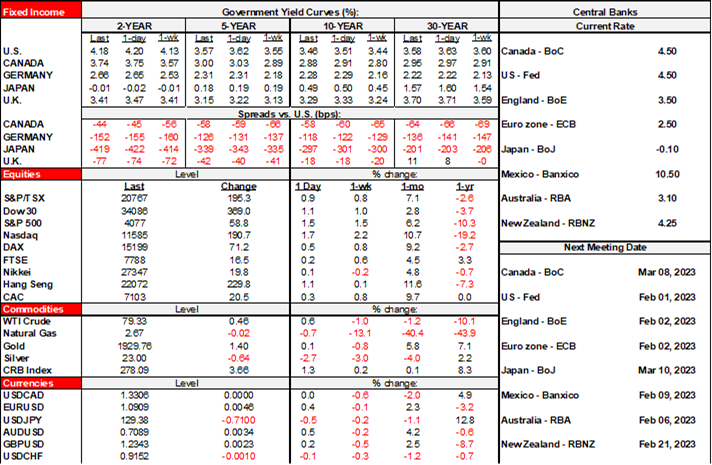

Markets are behaving about as one would expect on Fed day by playing it relatively safe. Eurozone core inflation was a lot firmer than I think is being appreciated (see below) which may embolden the hawks, but with strong caveats around the reliability of the estimate. N.A. equity futures are slightly in the red with European cash markets slightly higher. Sovereign bonds yields are a touch lower across Treasuries, Canadas, gilts wand EGBs. The USD is broadly softer except for a flat CAD. All markets will be primarily driven by the Fed today.

Eurozone core CPI inflation landed at -0.8% m/m NSA and 5.2% y/y which is the same as the prior month. So why do I say it was hot? Because the m/m drop in core was much less than is seasonally normal. Even though we don’t get SA figures with the flash estimates, we can deduce that core inflation was much stickier than most prior months of January given an average decline in months of January over the past couple of decades of about 1.3% m/m NSA (chart 1).

Why is it poor quality data? Because Germany delayed its estimates until sometime next week due to technical problems (hence the ‘NA’ entries for Germany). Because basket weight and methodological changes raise uncertainty. Because it’s always just a flash estimate based upon incomplete information until we get the revisions on February 23rd.

US macro reports will dominate the calendar ahead of the Fed but merely pass the time ahead of the big show.

- ADP: January’s private payrolls release disappointed expectations with just 106k jobs created in January. It’s ADP and so given its tendency to throw off a lot of false signals we should treat it very carefully as a guide to Friday’s nonfarm private payrolls. Still, based upon the historical spread between initial ADP changes and initial private nonfarm payrolls, then is around a one-in-ten chance that nonfarm would land on consensus at 180k or higher which implies an ADP undershoot of 74k or more which is among the rare occasions (chart 2). That makes for slim odds that are slimmer yet if we take out that fat left bar on the chart that is skewed to experiences toward the start of the pandemic when jobs numbers were all over the map.

- Construction spending (10amET): This is expected to be little changed during December.

- ISM-manufacturing (10amET): Little change with a continued contractionary reading is expected. Watch prices paid and employment, but only as very loose guides.

- JOLTS job openings (10amET): They are expected to soften somewhat but remain over 10 million to end 2022.

- Vehicle sales (e.o.d.): January’s estimate is expected to soar from 13.3 million at a SAAR rate in December toward 15.5 million (consensus) and 16 million (Scotia). I’ve based my estimate off of JD Power’s industry guidance that usually performs well. This would be a massive 20% m/m SA rise that could singlehandedly lift retail sales for January when we get that tally on February 15th.

LatAm developments will focus upon Peru’s inflation update (10amET) and an expected hold by Brazil’s central bank with the emphasis upon guidance (4:30pmET). Canada’s calendar is almost empty except for a little watched manufacturing PMI for January (9:30amET) in a country that still has pretty lousy PMIs (no services estimate, and the Ivey gauge mashes all public and private sectors together). Earnings will include Meta Platforms (formerly Facebook) in the after-market but it’s tomorrow’s after-market earnings that will light things up when Apple, Amazon, Alphabet, Ford etc etc release.

As for the Fed, I won’t repeat the posting from yesterday afternoon here, but you can scroll back to see it and check the global week ahead for more. In general, I think markets are still underpricing rate hikes especially given new information that should put a hawkish spin on expected communications today. It’s the Great PivNot redux!

This FOMC meeting is a statement-only outcome (2pmET) with an ensuing press conference (2:30pmET), all sans forecasts and dots. Basically everyone in the markets and consensus expects +25bps. Powell went silent since the last FOMC meeting in December and only partly because he caught the plague earlier this month. Still, if Powell et al were uncomfortable toward positioning into the meeting they would have weighed in through covert channels again in order to put markets on side given how loathe they are to surprise markets with administered rate changes on game day. Several top Fed officials intimated the opposite by favouring 25.

Further, Powell hinted at a 25bps downshifting at the December meeting when asked about it:

“I can’t tell you that today. We’re into restrictive territory and it’s not so important how fast we go. It’s far more important to determine how high we go and how long we should stay there.”

In other words, I can’t tell you I’m going to hike by 25bps but I’m going to hike by 25bps.

I think we’ll get a reinforced hawkish bias along the lines of the December meeting when he said they were intent on raising to 5¼% and that the dots could shift higher again in March. Why? Because if anything the new information since that meeting has put them further behind achieving their inflation goal.

The US economy beat overly bearish forecasts for Q3 and Q4 GDP compared to how expectations evolved going in. After 3.2% and 2.9% q/q SAAR growth in Q3 and Q4 respectively the US economy remains in excess aggregate demand with an output gap estimated by us at around +1% and rising which is going the wrong way for the Fed’s liking.

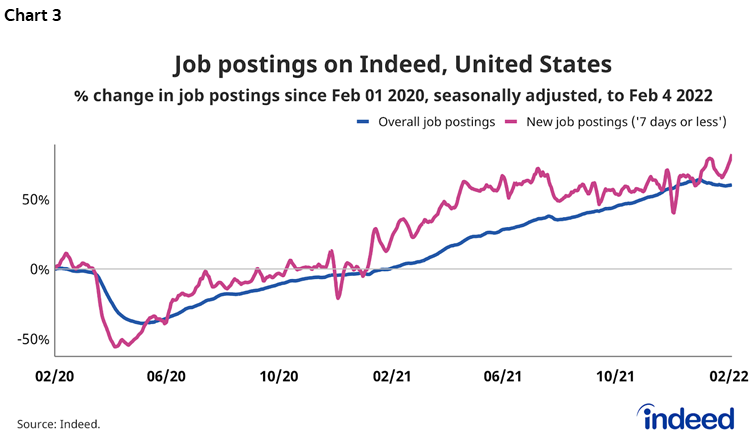

- on jobs, I think he’ll emphasize the rotation argument. There is enough hiring going on while mass layoffs are only reverting back to pre-pandemic norms and claims continue to fall which suggests that lay offs are being reabsorbed so far. Hiring announcements and vacancies remain high. Indeed’s measure of new job postings is shown by replicating their own chart 3.

- on inflation, he’ll just reinforce the same points about how it’s PCE, not CPI they focus upon. PCE is much less affected by housing/shelter. Services inflation still a concern. Core PCE was 0.3% m/m SA that when annualized is still above their comfort zone and the US is not making progress toward opening up disinflationary slack in the economy or job market.

- fin conditions are still reasonably accommodative with the 10-year T yield well off highs and trending roughly sideways over the past couple of weeks as stocks have rallied so far this year.

- The int’l backdrop is less worrisome. He can point to IMF forecast upgrades and less downside risk to Europe while upside risk in China has increased.

- he’ll dodge questioning on the debt ceiling at this point. It’s still early with the potential crunch arriving into mid-to-late Spring, perhaps early summer.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.