ON DECK FOR FRIDAY, DECEMBER 8

KEY POINTS:

- US payrolls will be a segue into a massive week for global central banks

- Will nonfarm payrolls reaccelerate?

- US UofM consumer sentiment and inflation expectations on tap

- BoC’s Gravelle poured cold water on early cuts…

- …and markets ignored him perhaps because of poor coverage

It’s nonfarm Friday. Therefore, nothing else really matters and ignore all present market readings that may be vulnerable to post-data swings. The report starts the march to next week’s massive line up of global central bank decisions and key data like US CPI. Overnight developments were very light as the rumour mill on Chinese fiscal policy measures and the BoJ’s good cop, bad cop routine continued. The RBI held as expected. UMich consumer sentiment is also on tap after nonfarm with its measures of inflation expectations. Also see my review of the BoC speech and key passages that pushed back against near-term easing while retaining a hike bias.

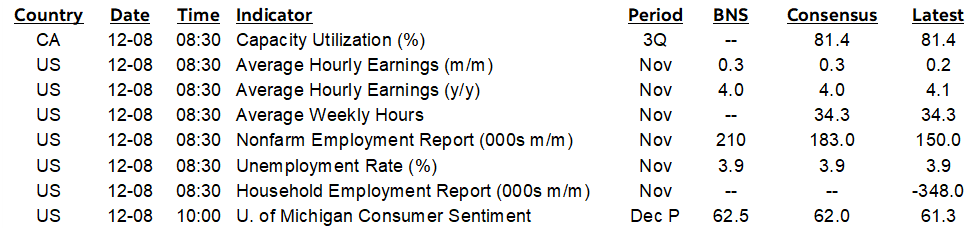

NONFARM PREVIEW

The US updates nonfarm payrolls, wages and other labour market readings for the month of November this morning (8:30amET). Highlights of expectations follow.

- Consensus median: 183k

- Consensus average: 181k (so, little skewness)

- Scotia: 210k

- Range: 130k–275k across most credible shops

- Std dev: 36k

- 90% confidence interval: +/- 130k

- Shadow estimate: 175k

- UR: 3.9% unchanged, range 3.8–4.0, Scotia 3.9

- Wages: 0.3% m/m SA from 0.2% prior, Scotia 0.3

Drivers:

Most of the signals drawn from other indicators suggest that the US labour market continues to be on strong footings. Add in a potential reversal of strike effects and the job gain could bounce higher.

- Challenge layoffs are still low at 45k in November

- initial claims were up a bit between nonfarm reference periods but only by around 10k which is negligible

- NFIB plans to hire increased a tick, but not much

- NFIB jobs hard to fill fell 3 points to the lowest since February 2021

- JOLTS job vacancies fell back to 8.73 million from 9.35 million last month

- Consumer confidence jobs plentiful increased by 1.6 points to 39.3 which conflicts with fewer openings in the JOLTS report in terms of what consumers say they observed.

- ISM-services-employment was little changed at 50.7 from 50.2, so it only registered a mild pick-up

- ISM-mfrg-employment fell a full point to 45.8 as mfrg employment fell at a quicker pace

- ADP was soft at 103k. Meh. Weak connection between initial ADP and initial private nonfarm estimates.

- There might be a positive effect from the end of strikes by the UAW and Hollywood (the Screen Actors Guild etc). BLS figures show 10,500 on strike in November, down from 48.1k in October. That said, despite what one might think, accounting for the impact of strikes on jobs data is anything but simple and the effect isn’t big enough that it would carry the day in any obvious way.

- On wages, part of what drove the market reaction the last time around was that wage growth at 0.2% m/m SA was the softest since February 2022. Most are betting on a mild pick-up partly due to a strong holiday shopping season and the need to fill openings.

BoC’s Gravelle Spoke, But Markets Failed to Listen

Bank of Canada Deputy Governor Toni Gravelle said fairly directly that the BoC is nowhere close to cutting rates and markets still didn’t listen. A possible reason is that his key comments were not picked by major newswires and perhaps the BoC should be calling around and asking why not.

So what did he say?

There were two keys in his press conference. The combined takeaway, to put a spin on a Fed quote, is that the BoC doesn't even appear to be thinking about thinking about when to cut. He said two things.

"What we are seeing in the data will be informative to see if we are on a path to 2%. We are not there yet. We've seen one month of good data that doesn't make a trend. Given the other indicators that we have seen it's pretty clear that we are not on a sustainable path yet."

"Once we have more confidence we are on a sustainable path to 2% then we might be in a position to even start thinking about cutting rates but we're not even there."

And so "pretty clear we are not on a sustainable path yet" and that only then will they "even start thinking about cutting rates but we're not even there" were hawkish signals to anyone who's listening to them. Clearly markets were not as they continue to price cuts beginning in Q1.

Gravelle also said:

"The economy is now roughly in balance, but we are closely watching inflation expectations, wage growth and corporate pricing behaviour. These indicators are helping us assess whether inflation is on a sustained path to 2%. Given the risks to the inflation outlook, we remain prepared to increase the policy rate further if needed."

And on recent inflation, this part was just repeating earlier guidance:

"Our preferred measures of core inflation dipped slightly in October. And on a three-month annualized basis, which is more volatile, it dropped to about 3%. While we saw some welcome improvement in inflation measures in October, we must remember it's just one month. We need to see further progress."

Why are Markets Ignoring Guidance?

Maybe El-Erian has some good points here on why markets may be aggressively diverging from Fed guidance. I think the credibility issue is a key one that is portable to the BoC since they blew it on inflation and forward guidance when they overreached by saying there wouldn’t be any hikes for years and years and then retracted that guidance upon discovering what they had done to ignite inflation. Why believe what they say now? It may also be that markets are captured by history in terms of looking at the average amount of time after hitting terminal rates—if we’re there yet—and when cuts first begin and without taking into consideration today’s differences.

There were also some other considerations worth flagging in Gravelle’s speech.

Immigration’s Effects on Inflation

To date, Gravelle says that immigration has had little effect on inflation (+0.1%), but the strong intimation is that it may very well have a greater effect going forward, given sharp housing imbalances that was a major part of his speech.

Gravelle spent a lot of time in his speech talking about housing. I think the message on population growth and shelter inflation is that they have no desire to add fuel to it given its large weight in CPI. Ergo, don't be in a rush to cut.

Immigration’s Contribution to Potential GDP

Be careful with what Gravelle said about potential GDP, defined as the level of output that could be achieved with full resource utilization.

The footnotes and the body of the speech say that they are estimating that between Q122 and Q223, population growth has expanded the level of potential output by 2–3%. That doesn't mean that's their estimate of potential GDP now; it's just part of it.

An offset is that productivity blows and that’s a surprise to the BoC given that Governor Macklem has repeatedly stated he expects it to pick up. Clear it’s not. More people are arriving in Canada with greater potential to raise output, but the overall working population is producing less and less per hour worked with each passing quarter. Unless Canada turns this around and fast, then it’s a rather large offset to immigration’s effects on potential GDP. Ditto for weak investment.

Immigration’s Impact Upon Short-term and Longer-term Inflation

One of the more important paragraphs in the speech was this one:

"Now let’s turn to how the arrival of newcomers affects inflation. As I just explained, higher immigration has improved Canada’s supply of workers, and that will greatly strengthen our economic prospects over the long run. But we are living in the present. And when newcomers first move to Canada, there is an initial burst of demand for goods and services as they set up home, which can put pressure on inflation."

That's the money quote on how population affects their outlook in the shorter-run timeline of monetary policy actions versus the longer run. Their focus is 1–2 years out, not in the long run when, as Keynes darkly put it, we’re all dead. Cheery fella.

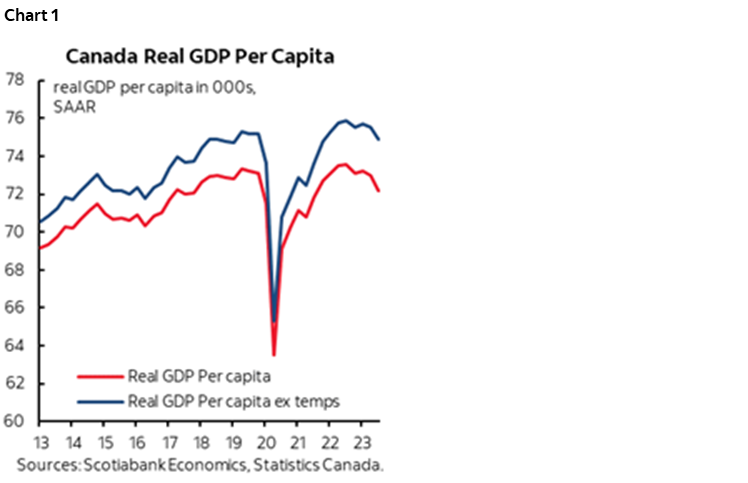

The Per Capita GDP Myth

Gravelle had a good section in his speech where he decomposed immigration flows. It’s important to my view that the crowd that laments poor performance on per capita GDP growth over the past couple of years is getting it wrong.

Nonpermanent residents account for about 60% of newcomers over the past year and include temporary foreign workers, international students and refugees. International students accounted for one-third of the population surge in 2022 and it's continuing.

International students are today's human capital story, but also today’s productivity drag and a drag on per capita GDP numbers. But the future holds out promise that as they transition to the workforce (assuming they stay in the country) then we'll get the GDP per capita and productivity boost as they move through their peak productivity growth years.

This is the problem I have with some of the folks lamenting per capita GDP's weakness as previously written.

1. They shouldn't use total population in per capita calculations. By using all of them in per capita GDP numbers, the implicit assumption is that they should be treated the same in terms of output potential as everyone else. Clearly not. Take out the nonperms and particularly students, and it's nowhere nearly as bad (chart 1).

2. The analog here is to the Alberta oilsands. When it was a capital sink hole with lots of $$ going in and nothing coming out, it was a productivity drag. Then as the megaprojects kicked in the effects reversed. The sudden surge of immigration should be viewed the same way.

In other words, as new arrivals get gradually integrated into job markets, housing and consumer markets, start businesses, etc, they will lift per capital output. You and I were probably doing little by way of contributing to GDP when we were students, but then much more so afterward. The point being we have to view it as a shock vs control experiment. The folks lamenting per capita GDP trends are only looking at the shock period either because they're not thinking, or because they're just being political and I think it's a lot of the latter.

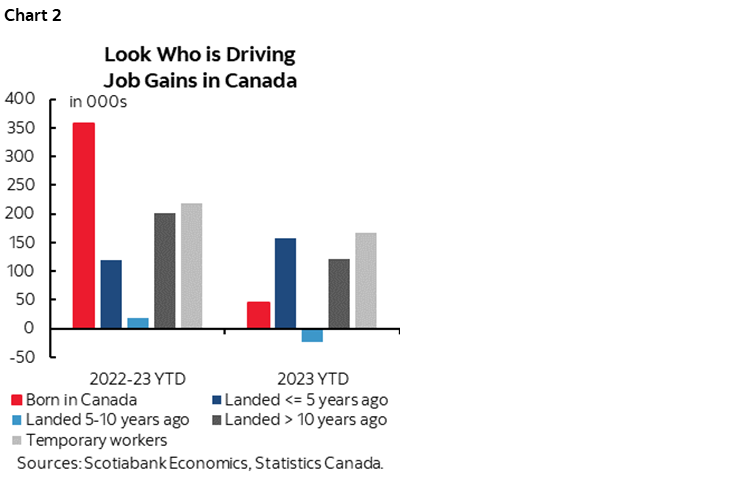

Who is Leading Job Growth?

Chart 2 speaks to what I think is a distorted argument in Gravelle's speech. He's saying permanent residents and nonpermanent residents have been leading job growth in Canada since the start of 2022. He does so by only plotting the % increase in their employment category levels over this time.

The same data source, however, shows that those born in Canada have accounted for the lion's share of the change in 000s of total employment in Canada over the same period. This effect is weaker this year. Temps, relatively recent arrivals who have been perms for <5 years and perms here for 10+ years have accounted for much of this past year's job growth. BICs and those here 5-10 years have been weaker.

The warning around this data is that there are wider confidence bands around the quality of this data than there are around the estimated total job changes.

So, was 2022–23 the norm, or is 2023 the norm in terms of who is driving employment expansion? More evidence is needed. I know that one of the issues with the student summer jobs market, however, was that temps were taking more of them this year. Ergo there may be a crowding out effect for a portion of the workforce but I'm unaware of evidence beyond the student market.

Here are some additional questions Gravelle was asked during his press conference.

Builder Complaints About High Rates

Q. Builders say inflation and interest rates prevent them from building. What do you say to them?

A. Lots of factors affect housing supply. We've had low interest periods marked by under supply and the same within high interest periods which demonstrates there are broader problems. Slow muni approvals, construction worker shortages, complex issue.

Q. You said we need to see further progress on inflation. Can you quantify what you mean by further progress? Does it have to be at or near 2% for a certain number of months before rate cuts are entertained?

A. We are focused upon underlying, core inflation to see if inflation is on a sustained path to 2%. We are looking at other indicators like wage growth, firm pricing behaviour, inflation expectations. What we are seeing in the data will be informative to see if we are on a path to 2%. We are not there yet. We've seen one month of good data that doesn't make a trend. Given the other indicators that we have seen it's pretty clear that we are not on a sustainable path yet. We no longer see any excess demand which should reduce inflationary pressures going forward.

Q. You seem to be more concerned about upside risks to inflation because of services and housing especially. When you speak of the risk of over tightening, is it possible growth is hurt but inflation won't come all the way back down to 2%?

A. We are worried about the risks of over- as well as under-tightening. We don't want to over do it, but we also don't want Canadians to live with high inflation for long. We are concerned about persistence in some of the indicators we are looking at. High wage growth, high inflation expectations, and we haven't seen the pricing behaviour of corporations come back to normal. I'll remind you that in the summer we saw inflation go down by June and it popped back up in August. There is volatility and we're holding onto our view that there are risks to the inflation outlook. October is only one data point. We want more evidence.

Q. Forward guidance was viewed as a helpful tool in the pandemic. Over most of this year, investors have been betting on big interest rate cuts despite central bank guidance. Is this divergence significant for bank policy now?

A. Forward guidance takes two forms. One during the covid crisis was commitment to holding at the lower bound. The other form was providing a hint at the next decision like the Federal Reserve does. We are trying to be more transparent so as to help guide markets but there is still divergence. There will always be a certain divergence. I wouldn't put a lot of weight on the degree of divergence. The bigger concern is when there is big divergence on the next decision and the market has been viewing recent decisions the same way.

Q. Canadian bond yields have fallen 100bps since October. How does this affect efforts to tame inflation?

A. We take financial conditions as given when we use our models. A loosening of conditions improves growth but it's a nuanced process that depends on what is driving those changes in economic conditions. Sometimes they ease because cutting is expected or because of a change in risks like the term premia. Our decisions are based upon many other factors as well.

Q. What is your message to people speculating upon when rate cuts may begin?

A. We have seen some relatively good news in terms of a slowing economy and no longer excess demand and with inflation coming down in October, but I want to be clear that we are looking for a sustainable trend in underlying inflation going to 2%. Some of the indicators we are using to assess this aside from excess demand are wages, inflation expectations, firm pricing behaviour. Once we have more confidence we are on a sustainable path to 2% then we might be in a position to even start thinking about cutting rates but we're not even there.

No Balance Sheet Updates

What we did not hear anything about from their markets head was QT plans, reserves, the CORRA-o/n rate spread, etc. Folks in the media didn’t even ask. The BoC will probably have to address that over H1 in my view especially if the market signals that they are getting closer to optimal reserves than they had previously judged become more acute.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.