ON DECK FOR TUESDAY, DECEMBER 5

KEY POINTS:

- Markets offer two more lessons for central bankers

- Eurozone inflation expectations moved a touch higher…

- …but EGBs are outperforming as an ECB hawk called a rate peak…

- …that markets somehow heard as a cut bias

- RBA holds and remains data dependent…

- …which bonds used as an excuse to rally

- China data beats…

- …but Moody’s negative outlook dominated equity sentiment

- Tokyo core CPI slips, JGBs ignored before rallying on China spillover

- It’s highly uncertain how three US data points will affect markets today

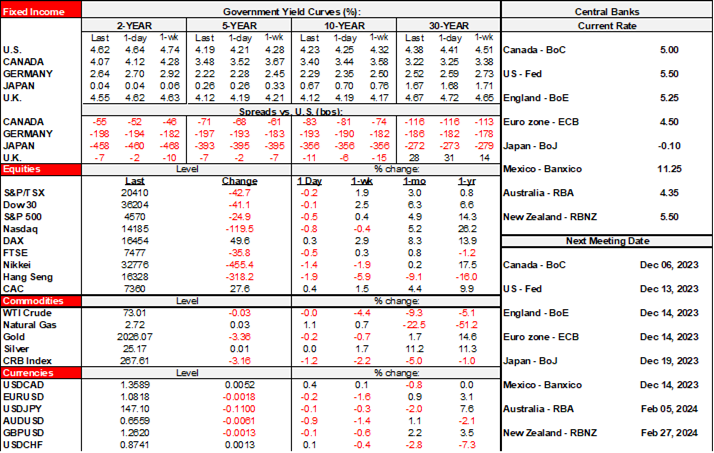

This morning brings two reminders of how central banks need to carefully manage markets and what they are up against in terms of a wall of money that’s pushing them around. The wall of money that they created, to be clear. Talk about Frankenstein turning on his creator. Hopefully the BoC is watching ahead of the next couple of days of its communications.

We saw evidence of how markets hear and see what they want when they listen to central bankers on the backs of remarks from the RBA and an ECB official. As a consequence, EGBs and Australia’s curve are outperforming US and Canadian yields that themselves are mildly richer after yesterday’s cheapening. Yields are bouncing up and down as much as rumours that are coming out of baseball’s winter meetings. US Ts are slightly lower this morning but could face significant data risk out of the US this morning and I for one have little directional conviction around the net effects (see below). I wouldn’t stick one’s neck out into the data, but if you do, well, good luck!

Here is a summary of overnight developments before flagging what’s ahead into the N.A. session.

1. RBA: Almost everyone expected a pause after the prior surprise hike and sure enough they left the cash rate at 4.35%. Guidance was unchanged by repeating a data dependent willingness to do more if inflation doesn't cooperate. Australian rates rallied despite the widely expected outcome perhaps as soon were positioned for a tail surprise on either the rate or guidance. The market narrative could be described as being something like the following:

Trader 1: The RBA held and stayed data dependent with a willingness to hike again if needed.

Trader 2: Did they say anything about cutting?

Trader 1: No they didn’t say when they would cut.

Trader 3: Did you say cut? RBA?

Trader 4: Whaaaa? Cut?? Outta my way, gotta buy!!

2. What happens when hawks give up? Markets hear cut and cut very soon and move to pricing it. That lesson was reinforced in the aftermath of comments by the ECB's Schnabel. She said another hike is 'rather unlikely' and therefore abandoned her bias while pointing to improving inflation. She refused to speculate on timing a first cut but markets raised pricing for a cut by the March 2024 decision which seems aggressive to me. This is more of a lesson on market management by central banks that are notoriously bad at it. Here’s the market narrative on that one:

Trader 1: Schnabel cried uncle, said no more hikes.

Trader 2: When does she think they’ll cut?

Trader 1: She didn’t say. Refused to speculate on when to cut.

Trader 3: Dude, hold on, this Schnabel guy, he said the ECB would cut?? Now??? Like, whoaaa, buyyyyyyy! By the way, Keanu Reeves is, like, my favourite actor, ya know. What’s for lunch??

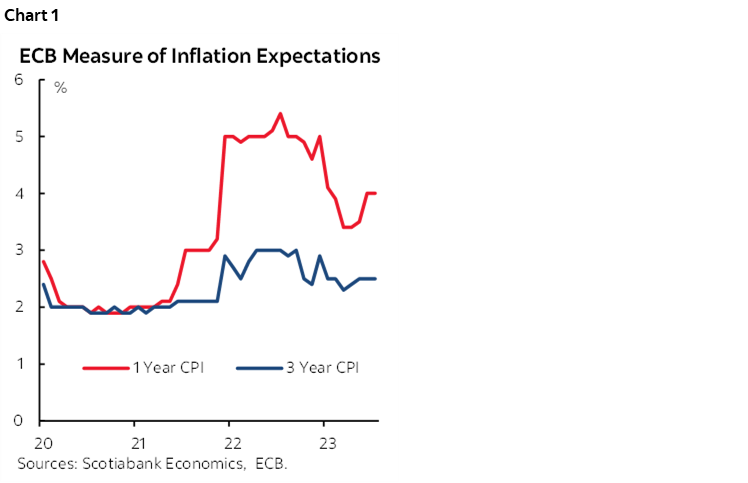

3. The 1-year ahead Eurozone inflation expectations measure surprised a little higher at an unchanged 4% y/y (3.8% consensus) and the 3-year measure was unchanged as expected at 2.5% (Chart 1). They’ve been drifting lower but remain elevated ahead of next week’s ECB. Other eurozone data on industrial output was a bit softer than expected. Rapid wage growth and still high inflation expectations counsel not getting too far ahead of ourselves on ECB cut timing and magnitudes.

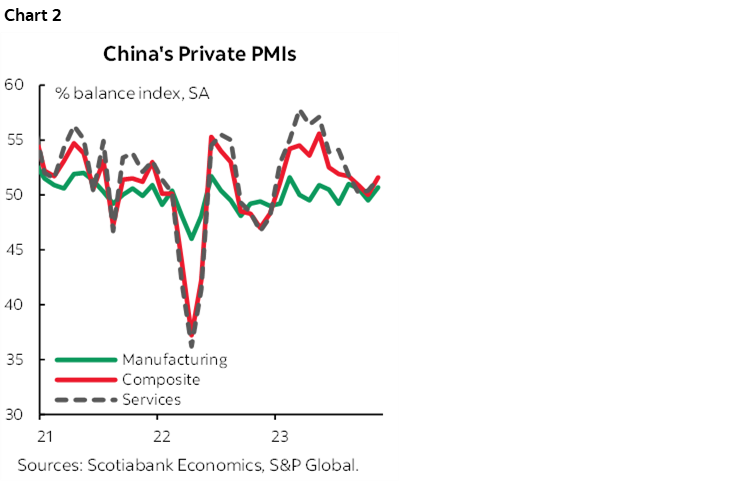

4. China data was better than expected as the private composite PMI moved up 1.6 points to 51.6 (chart 2). Both services and the previously reported manufacturing sectors improved. These gauges are less SOE oriented and more slanted toward smaller producers and manufacturers and exporters along the coastal cities.

5. Despite the decent data, Chinese equities fell by nearly 2% overnight. Among the catalysts was a leaked announcement by Moody’s hours before the official release that kept the long-term A1 rating unchanged but lowered the outlook to negative implying risk of a downgrade. Meh. Ratings agencies are great at reporting on accidents so I’m never sure of their worth frankly, so I’d rather weigh the data upside more heavily than equities did. That said, rumours are swirling about another cut to the required reserve ratio and we’ll see what the PBOC does next week.

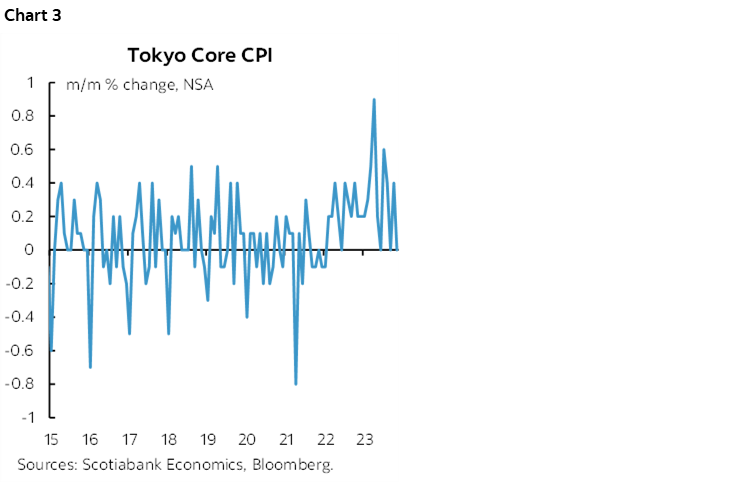

6. Tokyo core CPI landed a little weaker than expected at 3.6% y/y (3.7% consensus, 3.8% prior). The month-over-month core gauge continued its softening trend (chart 3). The yen and rates ignored it as the 10-year JGB yield fell hours later and likely having more to do with spillover from China.

7. South Korean inflation was weaker than expected. Headline fell -0.6% m/m and doubled consensus and core also ebbed. The rates curved mildly richened.

The main focal points into the N.A. session will be:

1. US JOLTS (10amET): Job openings surprised higher last time and prompted a rates sell off as the latest evidence of how they can be impactful before nonfarm arrives. We’ll see what this morning’s lagging update for October reveals as a pre-nonfarm teaser.

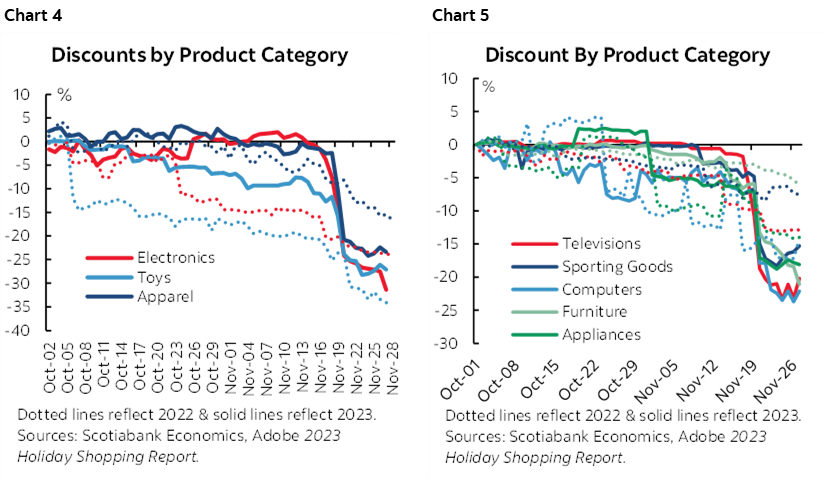

2. ISM-services (10amET): This will be a test of the holiday shopping season’s effects. A modest rise is expected. Price signals should also be watched given evidence of broader price discounting this season than last year’s holiday shopping period (charts 4, 5). Which effect may dominate—whether ISM’s headline, ISM’s details like prices, or JOLTS—is highly uncertain.

3. Canada updates its composite PMI (9:30amET). It's not widely followed.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.