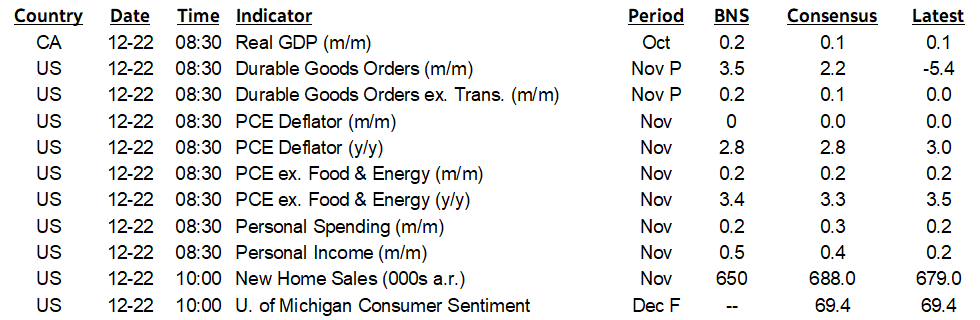

ON DECK FOR FRIDAY, DECEMBER 22

KEY POINTS:

- Global markets in holiday mode

- UK consumers smashed expectations

- Japanese core inflation is trending lower, supporting a cautious BoJ

- Canadian GDP: Likely a solid October, November question mark

- Will US core PCE land softer than core CPI?

- US consumer data will kick off holiday tracking

- Key to durable goods orders will be core

- US new home sales expected to rebound

- Global Week Ahead—Double Holiday Edition!

Please see the Global Week Ahead—Double Holiday Edition! here in publication format and the accompanying summary deck should be in your inboxes. This issue covers expectations through to January 5th 2024; the first week will be light, but the first week of 2024 will be packed with key developments.

The last day before Christmas will go out with a bang as several macro reports are digested. Thus far, the market effects are small. Early closes will likely give a concentrated period for N.A. markets to react as Canadian bonds shut at 1pmET and US bond markets shut at 2pmET.

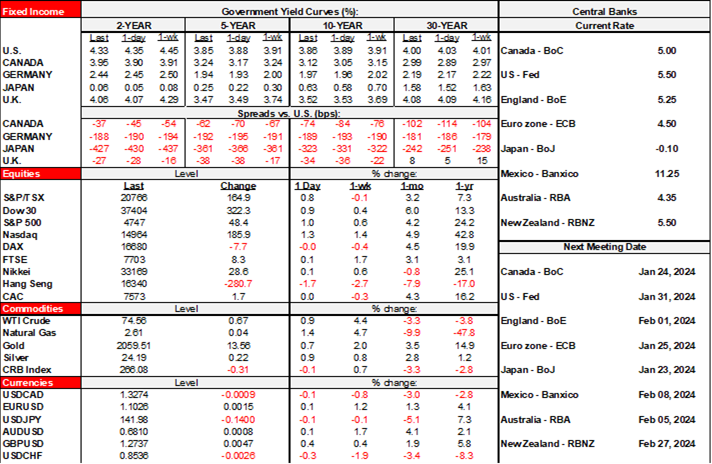

The dollar is very slightly weaker primarily against sterling and Scandies. Gilts are a touch richer despite a strong beat on retail sales. N.A. equity futures are little changed and ditto for European cash markets. US core PCE and consumer data poses mild risk and so does Canadian GDP.

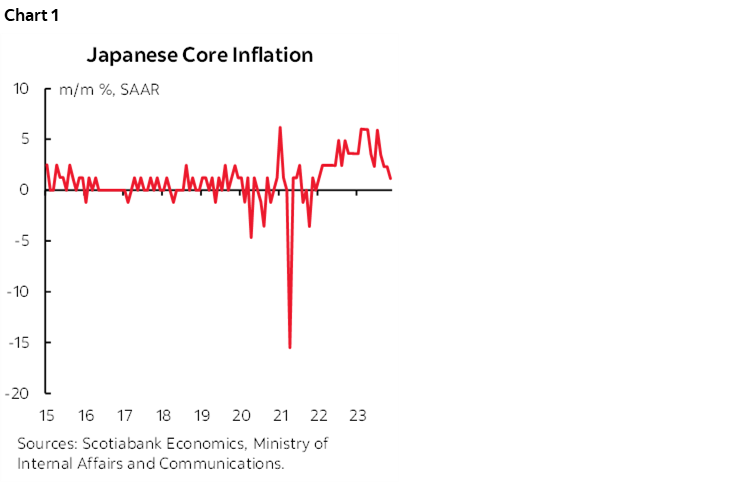

Japanese core CPI was weak in November and reinforces the lack of any BoJ urgency to end negative rates. Ex-food and energy prices were up by only 1.1% m/m SAAR following a pair of 2.3% prior gains which gives three months of increases that are signalling a material softening from earlier in the year and over 2022H2. The trend is pointed lower (chart 1).

A question is whether this is a soft patch driven by waning effects of the prior passthrough of oil and yen movements that could rise again with support from what could be the two strongest back-to-back years for wage gains since the early 1990s depending upon Spring negotiations. There is one more inflation reading before the BoJ’s next decision on January 23rd.

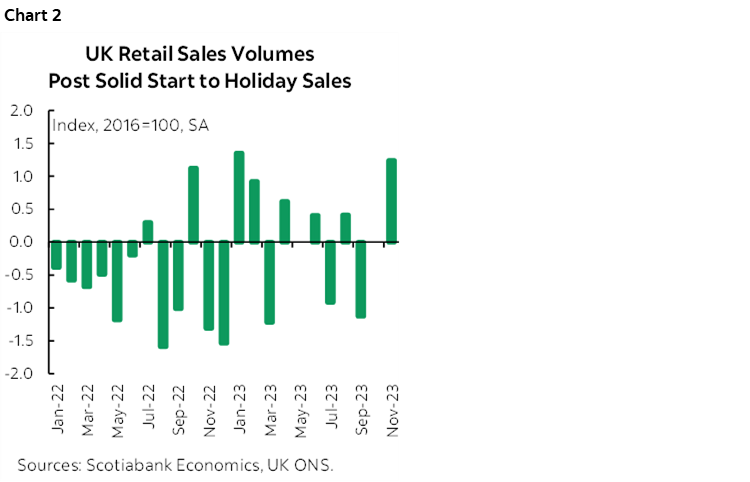

UK retail sales volumes strongly beat expectations along with positive revisions. Total sales were up 1.3% m/m in November (consensus 0.4%) and October was revised up a bit to flat from a mild -0.3% drop (chart 2). Sales ex-fuel were also up 1.3% (consensus +0.3%) and the prior month was revised up three-tenths to +0.2%. There was high breadth to the gain with household goods up 3.5% m/m, clothing and footwear up 1.3%, food up 0.8%, and most of it was done in person as a proxy for e-commerce sales was only up 0.2%.

Here’s what’s on tap into the North American session.

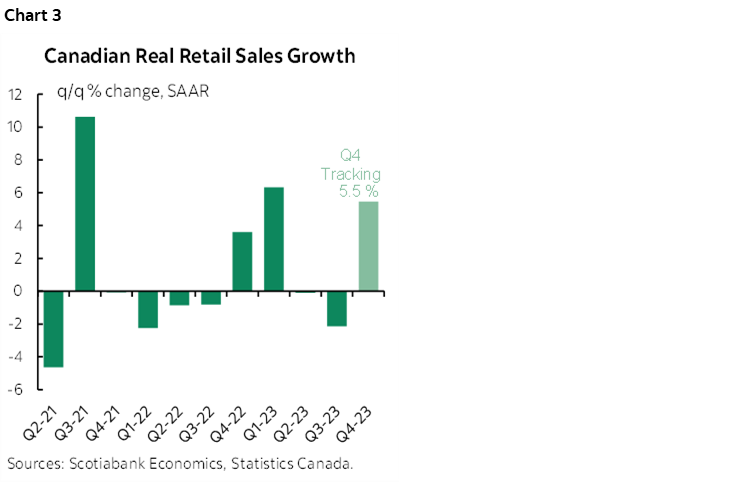

Canadian GDP—Solid Growth?

October’s reading is expected to grow by 0.2% m/m based on StatCan ‘flash’ guidance but as noted above I think there may be upside risk. We’ll also get the first preliminary estimate for November GDP that will advance tracking of Q4 growth. One upside is likely to be the retail sector. October’s sales volumes were up by 1.4% m/m SA and while Statcan only provided vague guidance that November’s sales in value terms were “relatively unchanged” we can probably infer likewise for volumes. The math works out to tracking a 5.5% q/q surge in retail sales volumes in Q4 over Q3 (chart 3).

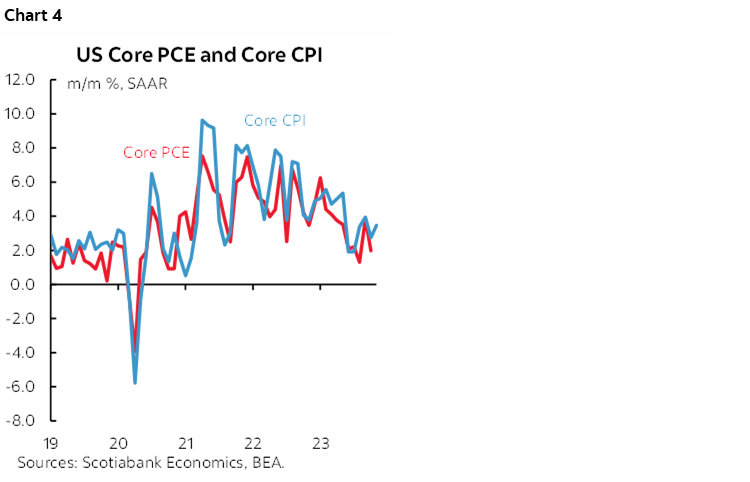

US core PCE—Soft with a Revisions Question Mark

How do yesterday’s downward revisions to Q3 core inflation impact tracking? I’m not sure. We can’t tell if October may be revised which in turn depends upon how the monthly revisions worked through Q3 including September. Therefore, we can’t really say with much confidence what the jumping off point for November may be like now. Before all of this happened, most were expecting 0.2% m/m which would be a touch softer than the 0.3% rise in core CPI for the same month. Core PCE has been tending to undershoot core CPI given its different methodology including a much lower weight on shelter (chart 4).

US Income Growth and Consumer Spending

A decent gain in consumption on the back of November’s holiday sales is expected to be accompanied by a stronger rise in incomes largely through the wages and salaries component (8:30amET).

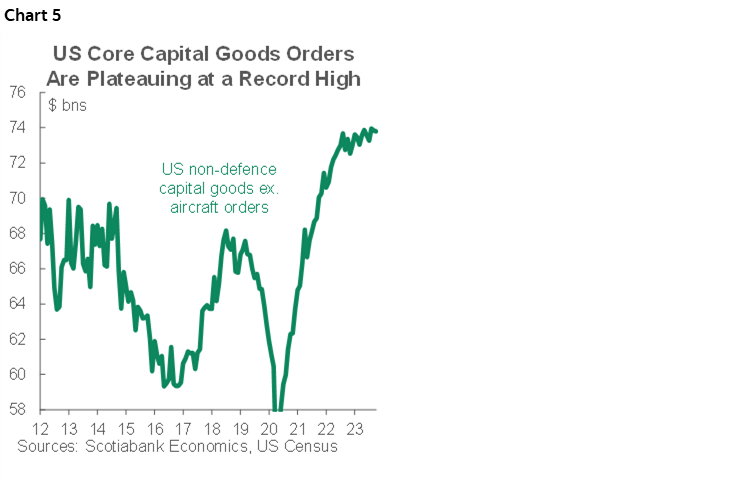

US Durable Goods Orders—Key Will be Core

November’s tally is expected to sharply rebound based on transportation orders but watch core orders that have been weak of late (8:30amET). Order levels are high but growth momentum has stalled out (chart 5).

US New Home Sales Expected to Rebound

November’s sales are expected to rise partly due to higher model home foot traffic that serves as a leading indicator (1030amET).

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.