ON DECK FOR THURSDAY, DECEMBER 21

KEY POINTS:

- U.S., Canadian data still poses risk as holidays approach

- BoC research poured cold water on mortgage reset hysteria

- Canadian retail sales probably posted a gain in October, November guidance key

- US GDP, core PCE revisions on tap

- Will US claims retain the prior dip?

- Bank Indonesia holds, pushes back against premature easing

- Turkey’s central bank hikes, signals it’s nearing terminal

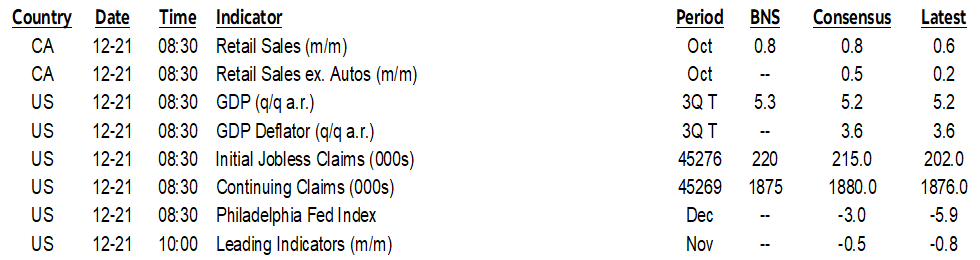

Expect a quiet session with the only main risk being any potential overreaction to minor revisions to US GDP and core PCE (8:30amET), modest Canadian data, and whether the US holds onto the dip in initial claims that fell to 202k the week before last (8:30amET).

The USD is mildly depreciating. There is a bias toward mild cheapening across sovereign bonds led by about a 2–3bps cheapening across US Ts. Equities are mixed with N.A. futures up by roughly ½% but European cash markets following yesterday afternoon’s sell off in N.A.

Bank Indonesia held its 7-day reverse repo rate at 6% as widely expected. Governor Warjiyo said “we will not rush” to ease next year and that they may only have comfort in addressing risks to the stability of the rupiah by “the second half of 2024.” There was little overall effect on the currency or rates.

Turkey’s central bank hiked by another 250bps to a new one-week repo rate of 42.5% as expected. The statement said that “The Committee anticipates to complete the tightening cycle as soon as possible” and emphasized its data dependence in determining future actions.

Canada updates retail sales for October and offers a preliminary estimate for November this morning (8:30amET). Statcan had previously estimated retail sales were up 0.8% m/m in October but this number is subject to revision. The November reading will kick off holiday season tracking.

Canada’s lagging payrolls report is also due out but it’s for October (8:30amET). The US releases its payroll and household survey numbers simultaneously but Canada has a long lag. Tomorrow we’ll get Canadian GDP and US PCE estimates to keep data risk alive.

CANADIAN MORTGAGE RESETS

The Bank of Canada has released a staff analytical note on the impact of mortgage resets (here). It’s highly recommended reading for multiple audiences with any interest in Canada whatsoever, whether from a broad economy perspective or an interest in housing finance or the implications for the Bank of Canada’s potential future policy actions.

The punchline is that under reasonable assumptions, they position the reset shock as a relatively small effect. Keys are the following:

- Absent any income growth over the years ahead, "the median borrower may need to dedicate up to 4% more of their pre-tax income to mortgage payments by the end of 2027" relative to what they were paying back in February 2022 just before the BoC began to raise its policy rate.

- By assuming income growth over 2024–27 at a pace equal to the average annual income gain over the past ten years, they whittle this estimate down further to a cumulative impact upon the mortgage debt service ratio of 1.5 percentage points starting from February 2022 through to the end of 2027.

Put another way, under their no income growth assumption, the average annual increase in debt payments as a share of pre-tax income for the median borrower is around 0.7 percentage points per year at a compounded rate. Under their scenario that assumes income growth, the average annual rise is about ¼% per year.

That’s not nothing, but it’s pretty darn close!

Also note that the income growth assumptions may be low. Income growth is currently proceeding at a considerably faster rate than the ten-year average as employment and wages both soared this year. I think it’s fair to conclude that wages will continue to rise at an aggressive pace over the next 3+ years given what is being incorporated into long-term collective bargaining contracts.

They also do not assume any changes in borrower behaviour "such as making accelerated payments or switching to another mortgage product" and "Thus, our simulation results represent an upper-bound estimate."

You could add to that by noting they say nothing about other mitigating steps being taken by borrowers and lenders alike including adjusting amortization periods and backing into strong home equity gains since the start of the pandemic, not to mention shifts in household behaviour.

A don’t have a problem with their assumptions on rates with the focus being upon fixed rates since variable rate mortgage resets are largely done. At about 3.2% right now, the Canada 5-year GoC yield may be rich in the short-term, but over the coming years it’s probably in the ballpark of what is reasonable after tacking a modest term premium onto a reasonable range of neutral policy rate assumptions.

It's important to read their whole study and also important to note that while the math leans against resets being a big macroeconomic shock, the distributional effects will be important. For instance, lenders see only the indebted folks and not the 60% of Canadians who don’t even have a mortgage.

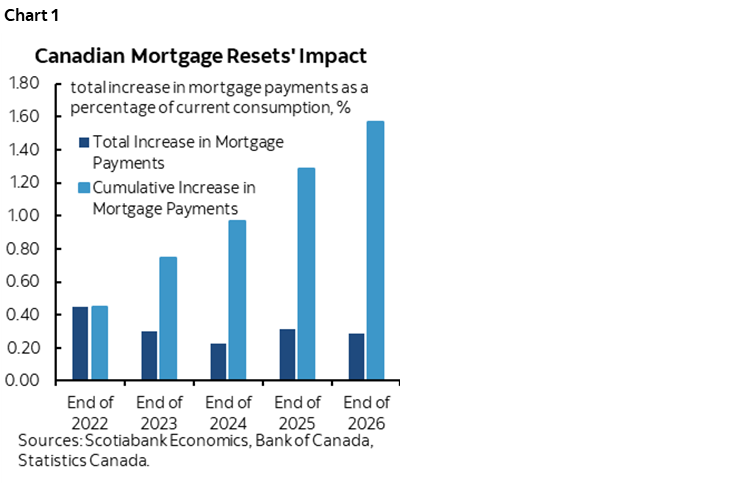

How does their work compare to spit balled estimates on the street given that the BoC has access to more system-wide data and greater resources? It leans close to my earlier estimate that resets would take up about a cumulative 1% of total income over the years ahead as argued in this piece back in September. I had argued that the effect on consumption would be trivial (chart 1).

By contrast, the BoC’s research makes a mockery of some of the rest of the street’s shrill cries especially its loudest and most alarmist voices.

Now how did the BoC research get covered and did market participants even notice it? Instead of Bloomberg—that, recall, hyped the ridiculously alarmist estimate—flagging that the BoC came up with little by way of any macroeconomic shock from mortgage resets, they only flashed that “higher payments hit 45% of mortgages” according to BoC research. Alarmism over substance. Frankly that’s appalling and it misinforms a considerable part of the world’s market participants who stare at their screens treating its content as the divine truth.

I still contend that mortgage resets are like an economic mirage. From a distance it looks like a dark, ominous, shimmering danger. The closer you get to the shock period leaves you standing with mouth agape wondering where all the worries went.

For BoC watchers, the clear conclusion is that while staff research doesn’t necessarily represent the opinions of Governing Council, it informs them and likely results in the following takeaways:

- The BoC is not going to ease just because of mortgage resets;

- As they have noted, resets are how monetary policy works in the first place;

- and the shock factor isn't anywhere close enough to something that could derail the outlook on its own.

On both counts, this further leans against premature rate cuts with markets overpricing easing too soon.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.