ON DECK FOR WEDNESDAY, DECEMBER 20

KEY POINTS:

- Sovereign yields move lower after a pair of European inflation readings

- Gilts bull steepen as core inflation posts one of the weakest Novembers on record...

- ...but it’s still just one print after a string of hotter than usual readings

- German producer prices mostly followed commodities lower

- Chinese banks left their lending rates unchanged as expected

- US consumer confidence is expected to improve

- BoC’s Summary of Deliberations may be stale on arrival

Thank you for an early Christmas present, Colorado. There is hope for adherence to the US Constitution and for fair justice in general. Now let’s see whether Trump really did buy off the Supreme Court.

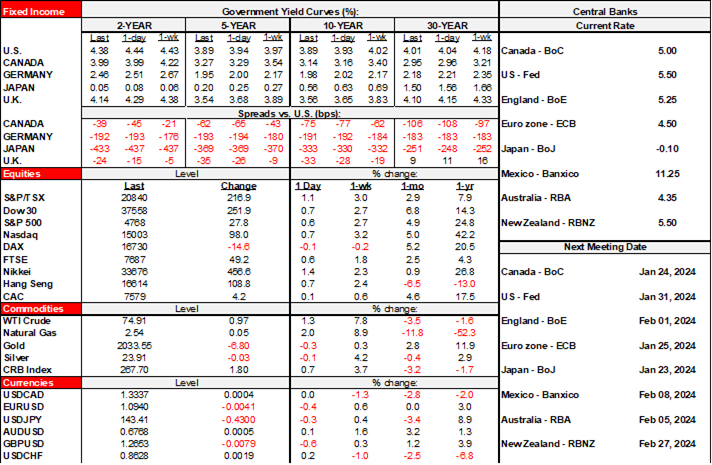

Sovereign yields are rallying and led by the UK on renewed pile on effects into global rate cut bets driven by one data point in one country. Some of the rally in US Ts preceded the European data. Stocks are mixed with London leading the few gainers and US futures lower with TSX futures flat. The USD is little changed on a DXY basis with sterling the main downside performer and the yen and won the main gainers. Oil is up a buck.

The main focal points include the aftermath of soft European inflation readings ahead of some US macro data and more BoC communications.

Chinese banks left their 1- and 5-year lending rates unchanged as expected.

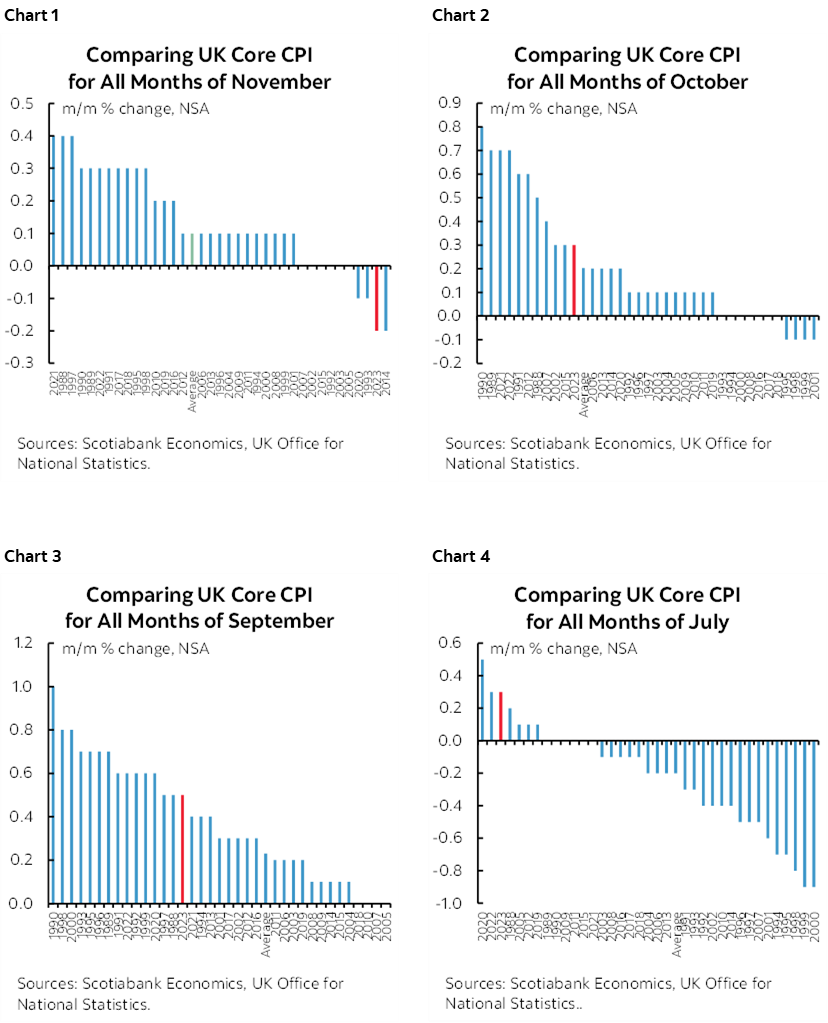

UK CPI tumbled by more than expected and that drove yields on gilts sharply lower in a bull steepener move with 2s rallying 14bps and 10s down 9bps. Sterling is leading decliners to the USD. Markets doubled pricing for a March rate cut with about 50–50 odds now while shifting to more than fully price a cut by May. Those are big moves on one data point. Core CPI in m/m NSA terms was among the weakest on record compared to like months of November in history (chart 1). That pulled the y/y core rate down from 5.7% y/y to 5.1% (consensus 5.6%) for a sizable downward surprise. Is it overdone? Perhaps, as it is just one month of data after a long string of hotter than seasonally normal m/m gains (charts 2–4).

German producer prices fell 0.5% m/m in November (-0.3% consensus) which is broadly in line with the softer tone in commodities last month. Energy prices fell 1.4% m/m, but PPI ex-energy also slipped by just -0.1% m/m with a small dip in food prices contributing alongside flat consumer and capital goods prices. This data reinforced UK CPI in contributing to dearer EGBs.

On tap into the N.A. session will be the following matters.

US consumer confidence (10amET) is expected to improve in December’s reading, given improved cash flow (recently faster wage growth, lower gasoline prices), and lower mortgage rates amid easier financial conditions including equities. The Conference Board’s measure is more driven by employment conditions than the UofM gauge.

The BoC’s Summary of Deliberations in the lead-up to the December 6th decision will be released in the afternoon (1:30pmET). Watch for further discussion around the range of opinion on whether to retain a hike bias in addition to potential further guidance on the guideposts for eventually easing. The Summary might be a tad stale given the Fed and given Canadian CPI.

The US also updates existing home sales for November (10amET). They may hold steady at about 3.8 million SAAR given tracking of pending sales.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.