ON DECK FOR FRIDAY, DECEMBER 1

KEY POINTS:

- Markets await Powell’s last words into blackout

- What Powell might address

- Canadian jobs and wages to update what is already a very strong year

- ISM-manufacturing headlines US macro readings

Done your Christmas shopping yet? Month-end brings new beginnings as the calendar flips over after a wild rally in basically everything last month. There are lots more investing opportunities ahead and it starts today with key developments such as updated thinking from Fed Chair Powell and key releases from Canada and the US. Tuck a nice bond under that Christmas tree. How romantic.

Canada’s bank earnings season ended in a tie with three beats and three misses. BMO disappointed expectations for adjusted EPS this morning while National Bank beat.

CANADIAN JOBS PREVIEW

One month doesn’t make a trend but try telling that to whippy markets these days if we get a surprise when the job market readings get updated for November this morning (8:30amET). A big gain might be less impactful to markets than a loss given the market’s bias these days. All estimates are within the 95% confidence interval of +/- 57k that defines the noise bands. That signals lack of conviction.

To date, it’s hard to say job growth has been slowing on a trend basis. Canada gained 18k in October but posted 40k and 64k gains over August and September and is up by over 400k jobs year-to-date.

Here is a summary of the expectations:

- Consensus median: +14k

- Consensus mean: +14k (no skewness)

- Scotia: +15k

- Range: -5k to +50k, most within about 10–20k

- 95% confidence interval: +/-57k

- Std dev: 12.25

- UR: 5.8% from 5.7% (Scotia 5.9%)

- Wages: ~5% y/y

The expected drivers include the following points:

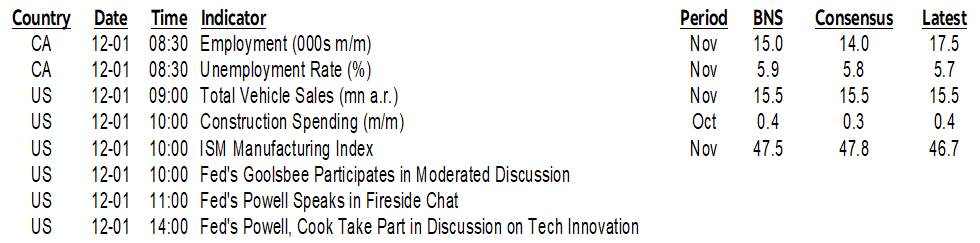

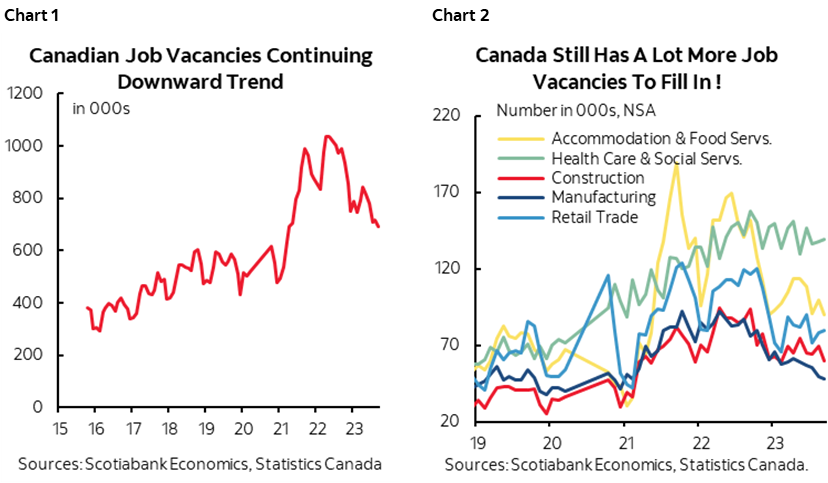

- vacancies could continue to be filled. They have come down but remain elevated especially in categories like health and social services and accommodation and food services (charts 1, 2).

- immigration remains very strong, although the born in Canada category is filling many of the vacancies. Either way, the two forces can continue to fill ongoing openings.

- striking workers don’t drop out of the Canadian numbers, but there may still have been a strike effect weighing on the October manufacturing numbers that could rebound

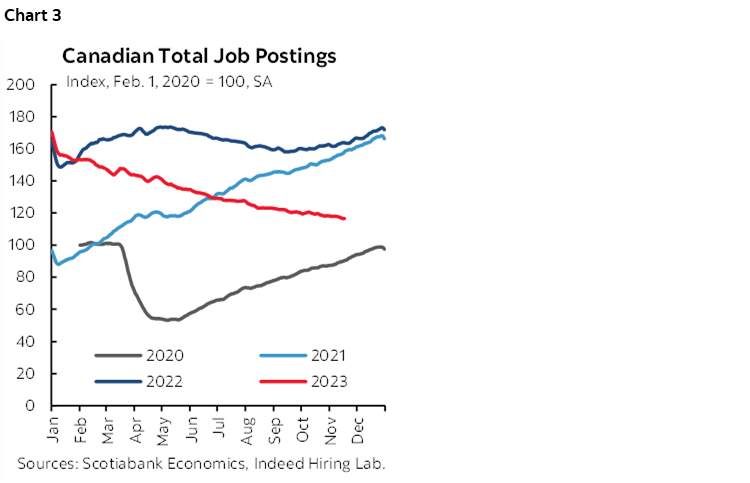

- job postings have been trending softer but are still strong enough for job growth (chart 3).

- firmer GDP growth in September and October from earlier months may be correlated with employment gains.

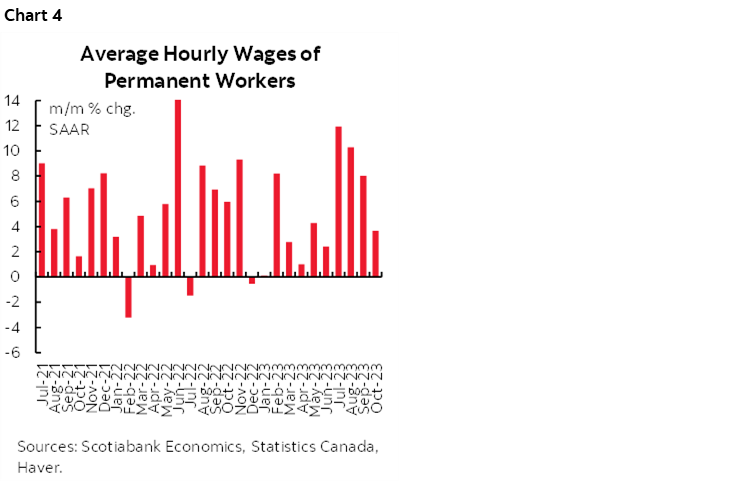

- wage growth eased to 3.7% m/m SAAR in October which is still well above the BoC’s 2% inflation target but it was the softest reading in four months (chart 4). November’s reading will inform whether there is a new trend. Nevertheless, wage growth is sharply exceeding tumbling productivity and the two have to be considered together as we await the Q3 update on productivity and unit labour costs next week.

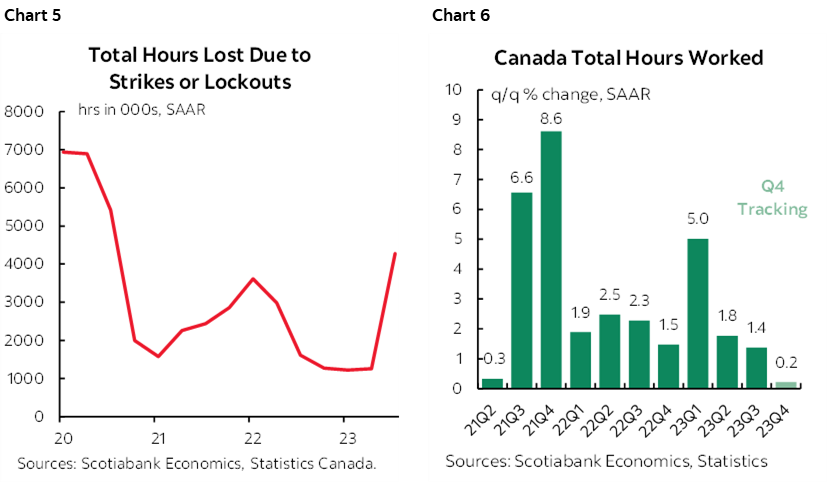

- Also watch hours worked. We lost a lot recently due to strikes and the result is that so far there is no growth in hours baked into Q4 (charts 5, 6). Will that rebound from strikes this morning, or continue to be soft?

FED’S POWELL AND DATA TO DRIVE US MARKETS

US markets will focus upon Fed-speak and macro releases as follows.

Fed Chair Powell gets his last remarks in before the communications blackout kicks in tomorrow ahead of the December 13th FOMC decisions. He’s in a fireside chat at 11amET (watch here). A hold is widely expected at the upcoming meeting, but Powell’s appearance could be useful in other respects.

For one, how are they presently viewing financial market conditions? He might have to soften references to tightened financial conditions given the powerful moves in bonds and equities since they statement-codified reference to tighter financial conditions in the November 1st statement. They did that basically at the peak for the 10-year Treasury yield that has since rallied back to about mid-September levels. That still retains some of the sell off in fixed income that occurred particularly from late July through September, but instead of the 10s yield (that drives 30-year mortgages in the US) being up by 130bps since late June, it’s now up by only about 60bps. At the same time, the S&P500 has pushed toward a record high on a nominal index basis with a trailing price-earnings of over 22 times and 1-year forward price-earnings ratio of 20½.

For another, will Powell provide any guidance that could inform expectations for the coming dot plot? What does he think of market pricing for cuts to begin as soon as March/April and over 100bps of easing by the end of next year? The September dot plot showed 50bps of cuts in 2024 which would also imply a probably later start than is priced.

We also get three forms of data out of the US this morning:

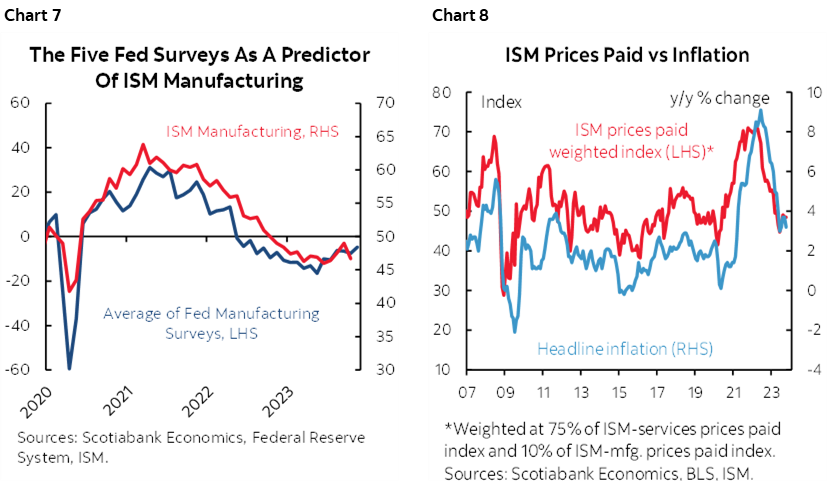

- ISM-manufacturing (10amET): Most of the focus will be upon this reading for November. It’s expected to improve but remain in contraction partly due to what we know about the regional surveys and transportation production (chart 7). Also watch prices paid given the connections to inflation (chart 8).

- Industry guidance also points to expectations for vehicle sales during November (e.o.d.) to remain around 15.5 million and hence trending at the highest levels since early 2021 when they rebounded from the pandemic’s initial effects.

- Construction spending during October (10amET): a mild gain is expected to extend an uninterrupted streak of increases throughout this year.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.