ON DECK FOR WEDNESDAY, AUGUST 9

KEY POINTS:

- Stability returns to global markets…

- …on signs that US debt supply is being digested in orderly fashion…

- …as Italy’s unhelpful assault on banks gets pared back…

- …and as markets benignly position for tomorrow’s US CPI

- But talk of Chinese deflation being exported is utter nonsense

- Today’s US 10s auction will further inform Treasury curve pressures

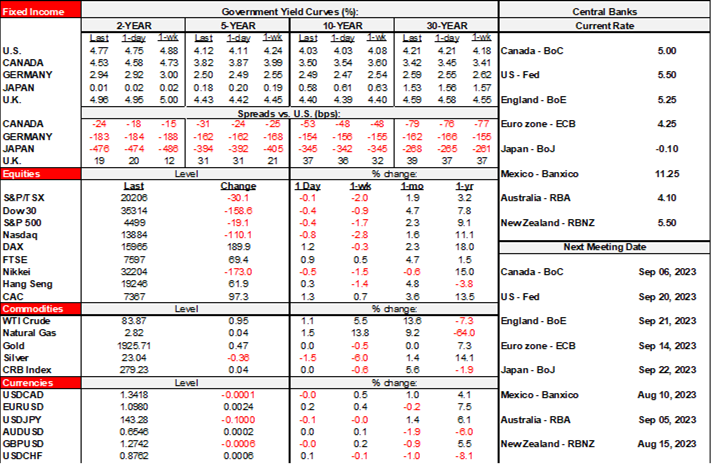

Global asset classes are a little more stable so far this morning. Stocks are broadly higher with N.A. futures up by ¼% to ½% and European cash markets up by around 1% on average expect for a 2% gain in Italy. Sovereign bond yields have settled down after yesterday’s rallies across the long ends of global curves. The USD is a touch softer. Oil is up by about 1% across WTI and Brent.

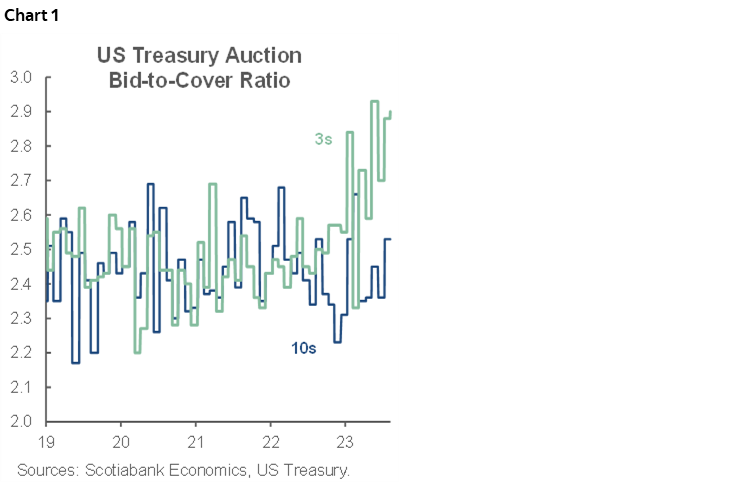

The culprits? Some hypotheses may be more sensible than others. One may be a sense that US debt supply is being taken down in an orderly manner after yesterday’s successful 3s auction but ahead of today’s more critical 10s auction and tomorrow’s 30s. If so, then that allays concern that had crept into markets as part of the bear steepener trade that seems to have passed at least for now. The 3s bid-to-cover ratio held strong on the attractiveness of front-end yields and perhaps the 10s bid-to-cover ratio will close some of the spread between the two measures with the yield holding around 4% this morning (chart 1).

Second is that the populist keystone cops running Italy’s government backpedaled on their dig at banks by watering down some of the tax on “excess” profits including higher definitions of tolerated profit gains before triggering the higher tax and setting a cap relative to assets, albeit still being worked out in definitional terms. Italy, like Canada, prefers populism over sensible policies as tax incidence effects get passed on one way or another whether the average voter gets that or not.

Third is that markets are benignly positioning for tomorrow’s marquee print-of-the-week when CPI arrives.

But Chinese deflation?? Being exported across the world in dovish fashion??? Yeah, that interpretation is about as believable as the likelihood of me being spotted next to our PM at a Taylor Swift concert. The widespread media headlines about deflation are making four interpretive errors.

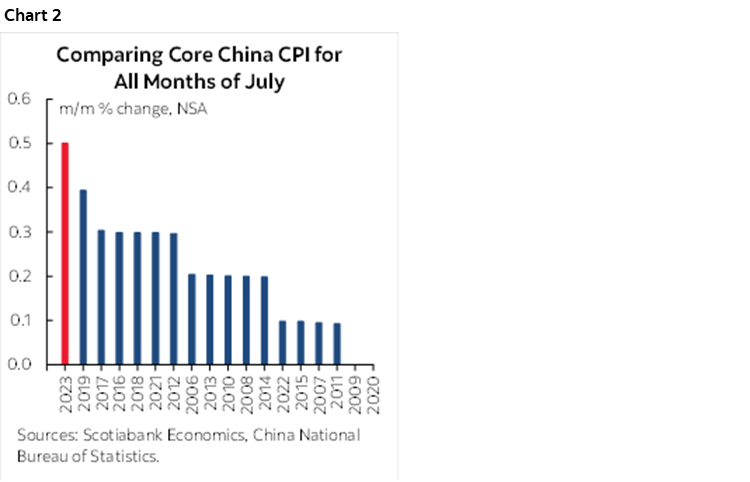

- The most glaring one is that China just posted the strongest month-over-month rise in core CPI for a month of July in records back to at least 2012 (chart 2). At 0.5% m/m NSA, the gain strongly exceeded the average for months of July over the past dozen years that works out to 0% m/m NSA. The evidence at the margin points toward a strong rebound in inflation pressures. I’ll include a chart in the fuller morning note.

- Second is that deflation has to be about more than just year-ago base effects and yet that was the only reason why CPI fell in year-over-year-terms.

- Third is that the negative year-over-year headline CPI reading was narrowly driven by food prices (-1.7% y/y). Ex-food, prices were flat at 0% y/y. Ex-food and energy CPI was up 0.8% y/y. Deflation isn’t just about commodity prices and yet it was commodity prices that drove the negative year-over-year CPI reading.

- Fourth is a casual interpretation of what constitutes deflation. Most economists would define deflation as a sustained, economy-wide decline in a broad array of prices that affects behaviour in such fashion as to result in decisions like postponing consumption and investment into periods when cheaper prices are expected to prevail. That can be a devastating spiral effect that is difficult for policy to turn around. Think 1930s. China is nowhere close to facing this scenario and the talk of deflation is often far too fast and loose.

Granted, all of this assumes that the price figures are reliable and not just the made-up creations of local Chinese Communist Party sycophants who are either seeking approval or avoiding retribution within the ranks of the Chinese dictatorship. That concern is nevertheless omnipresent when it comes to Chinese data and hence it would apply to not just one month’s figures.

If this month-over-month pressure persists as year-ago base effects shake out, then China’s year-over-year readings will be sharply rebounding later this year and through 2024. That would quash the narrative that China is exporting deflation elsewhere in the world and doing the work of global central banks for them. It could give rise to the opposite nonsense that China is exporting inflation to the world. Furthermore, the whole reshoring narrative posits that reconfiguring supply chains away from countries like China to other markets like Mexico merely shifts the inflationary pressures around in shell game fashion. This narrative remains at a highly nascent stage as c-suites seek to reduce financial distress costs within supply chains that have been rocked by serial border shocks since 2016 even if that means accepting higher operating expenses and passing them on to various stakeholders.

Three other inflation prints leaned against any deflation nonsense. One is that Taiwan’s core CPI was up by 2.7% y/y (2.6% prior) and 0.1% m/m NSA. No deflation there.

Two is that Colombia’s inflation reading remained hot last evening. Core CPI was up 11.4% y/y (11.6% prior) and 0.6% m/m NSA which was hotter than seasonally normal for a month of July that has averaged a 0.4% m/m NSA gain over like months of July since the GFC. Certainly no deflation there either.

Thirdly, the RBNZ’s measure of inflation expectations two-years ahead held steady at 2.8% in Q3, unchanged from the Q2 estimate. That remains above the 2% medium-term inflation target as a persistent challenge to the central bank.

Mexico’s CPI reading is next up (8amET). Forecasting monthly Mexican inflation is a bit of a cheater’s paradise in that the country releases bi-weekly estimates. Half the month is already known by the time the monthly reading lands which makes forecasters of monthly Mexican CPI estimates look like geniuses compared to elsewhere. Gains of 0.5% m/m for headline CPI and 0.4% for core CPI are expected.

Then the US$38B 10s auction will be a key focal point that informs whether we truly have put the roughly two-week bear steepener behind us after the 10s yield peaked last Thursday (1pmET). Yesterday’s 3s auction was a nice set up.

Data risk will be very low with just weekly US mortgage applications on tap (7amET) and nothing material out of Canada all week.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.