ON DECK FOR THURSDAY, AUGUST 24

KEY POINTS:

- Markets on tenterhooks as they await Powell, Lagarde tomorrow

- US durable goods orders drop entirely due to volatile aircraft orders

- US jobless claims remain low

- Jackson Hole agenda arrives tonight

- Canada auctions 5s today…

- …as managing its movements highlight the BoC’s core dilemma

- Canadian bank earnings season kicks off with a beat and a miss

- BoK’s hawkish hold drives won appreciation

- Turkey’s central bank ups the ante on the long road to repairing credibility

Relative calm is being temporarily restored before Powell’s potentially key speech on Friday morning and Lagarde’s speech at 3pmET tomorrow. Most of the focus is upon light US data and Canadian bank earnings.

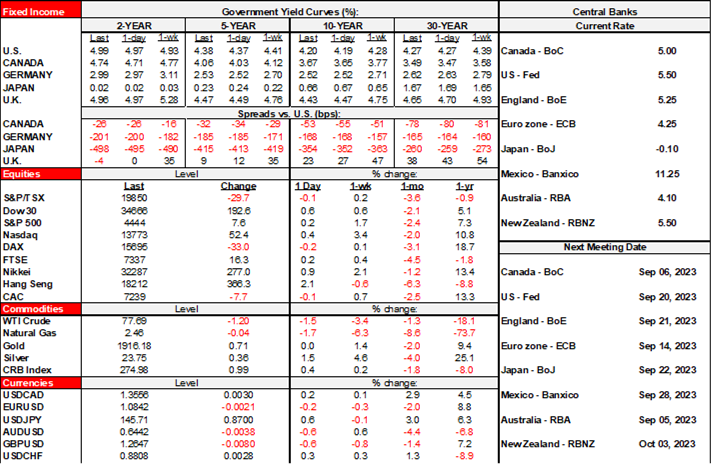

Stocks are mixed as small gains are being posted in N.A. while Europe is averaging out to flat and following small gains across Asian exchanges. US Treasury yields are slightly higher in mild bear flattener terms as Canada’s curve sells off by 3bps across maturities. EGBs are mildly cheaper and the gilts longer-end is rallying. The USD is slightly firmer.

The Bank of Korea left its policy rate unchanged at 3.5% with a hawkish bias as widely expected. The won vaulted to the top of the pack versus the USD as one of the very few exceptions to dollar strength along with, say, the Taiwan dollar and Turkish lira.

Turkey’s Long Road to Repairing Credibility

On that note, what price is paid when politicians mess with central banks? Look at Turkey where a new batch of Erdogan's puppets continues to strive toward restoring credibility after their leader's ruinous interference. They hiked the one-week repo rate by 750bps to 25% this morning. Yes, 7.5 percentage points which is not a typo. That blew away the highest guess in consensus that was 20.5%. The pattern across recent decisions had been to underwhelm on the magnitude of expected hikes as they sought to restore stability to the lira and inflation and so each time the lira depreciated in response and helped to propel inflation higher to 48% y/y in July. Not this time, as the lira sharply gained following the decision. The path to restoring the severe damage to the central bank’s credibility is going to be a long and challenging one—with the erratic man who messed it all up still lurking in the background. That’s a lesson to all politicians everywhere and a reminder to US Presidential candidates of the cost to playing politics with central banks.

JH Agenda & US Data

We’ll get the JH agenda tonight on the KC Fed’s web site (8pmET). Light Fed-speak will feature Philly’s Harker (10amET) and Boston’s Collins (11:15amET).

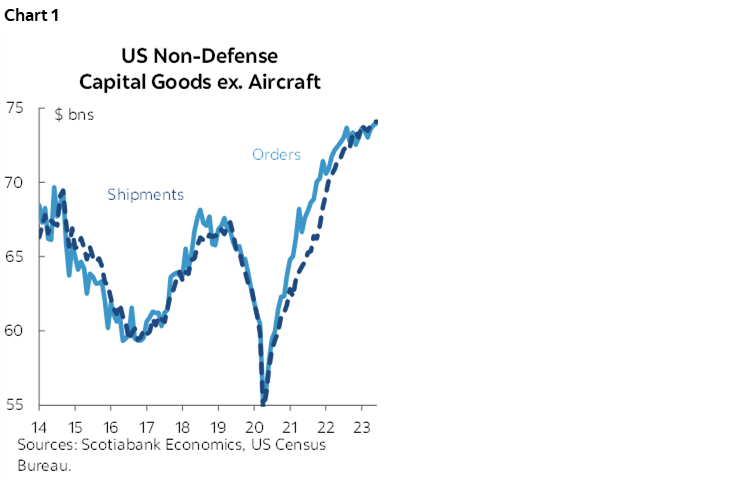

US durable goods orders fell 5.2% m/m (-4% consensus) but weakness was entirely due to aircraft orders that we knew in advance. Durable goods orders ex-trans were up 0.5% m/m. Core capital goods orders (ex-air and defence) ticked up by 0.1% m/m which is not great following the 0.4% dip in June, but they followed strong gains in April and May. Still, the recent trend is indicating a levelling off in appetite to invest (chart 1). Nondefence aircraft fell by about 44% m/m but vehicles/parts were up 0.8% and so the transportation component was entirely about how Boeing's order surge in June gave way to a strong mean reversion effect in July and perhaps now into renewed challenges with its flagship plane.

US weekly jobless claims remained range bound at 230k (239k prior) with no states being estimated in what appeared to be solid data. Jobless claims remain low.

US Trade Policy Risks Harming C-Suite Confidence All Over Again

In addition to cyclical uncertainty, core orders will be the test of business confidence around the 2024 election which repeats a point that I made earlier this week. Softening orders in 2019 occurred even before the pandemic struck and had partly reflected the toll of trade wars on confidence across c-suites to engage in big-ticket cap-ex spending when they lacked confidence toward the rules of the game that would emerge from the tensions. I'm worried that they'll pay a price again for US political uncertainty through 2024–5. To that effect, even the WSJ—that in past years gushed with praise for Trump—issued the same warning that I wrote about earlier in the week on the risks around US trade policy and the threat of a wall of renewed tariff hikes (here). One of the prime risks to the global outlook over coming years is misguided US trade policy that would resurrect battles between America and both friends and foes that would serve no one well including American consumers and workers. I think c-suites need to be very careful toward layering on increased cap-ex budgets into this environment as the US risks an own-goal on trade policy missteps all over again and at the expense of global frictions.

CANADIAN AUCTION, BANK EARNINGS

Canada is focused upon bank earnings and has a 5-year auction today at 12pmET. RBC beat, TD missed for a draw to start the season and the rest are due out next week including my employer’s results in Tuesday.

MANAGING THE BELLY WILL BE THE BANK OF CANADA’S CHIEF CHALLENGE

I’ll leave views on how the five-year auction might go to better hands than mine across the folks who must competently clear it. But it’s worth addressing how the movement in the five-year yield relates to the BoC’s communications and its potential current policy stance.

I think the BoC is probably pleased that, whether through luck or good policy, their influence has been exerted further up the curve into the belly and the key 5-year portion given its importance to the mortgage market. The yield has gone from around 2.75% early in the year following the BoC’s January pause that in my opinion misread the Q4 soft patch in the economy and the likely Q2 rebound, and then again at the low back in March when US banks were blowing up, to over 4% now. The 5-year bond took its time in shaking off the US regional banking developments and was trading around 3% straight through to about mid-May. This combination of external shocks and the BoC’s market mismanagement earlier in the year contributed toward igniting the Spring housing market alongside the other policy missteps that include poor execution of immigration policy by the Federal government. The market wasn’t listening to the BoC’s subsequent communications that kept the door open to further tightening and leaned against premature rate cuts.

With the five-year at about 4% now, the BoC can perhaps take some satisfaction that the market is now listening, but with a strong caveat. It’s listening because it is pricing a decent chance at another rate hike over coming meetings. It’s listening because it has pushed off modest rate cut pricing into 2024H2 and beyond. That could be enough to give the BoC confidence to pause in September and perhaps beyond—and risk courting a renewed chicken-and-egg challenge.

Now let’s say the BoC whiffs in September. Maybe it whiffs again in October. The strong likelihood would be that the market declares the BoC’s tightening cycle is done regardless of whatever the BoC says. Markets being markets then motivate yet another violent positioning swing into the front-end through the belly and start assuming that the clear signal they are done means cuts are coming sooner than priced. The 5-year rallies back to, I dunno, 3% again? Maybe lower? And then the Governing Council does its best Gomer Pyle impression wondering how they lit up the mortgage pre-approvals pipeline into the next Spring housing market all over again. Gawwwly how’d that happen??!!

The best tool to prevent this is to continue to lean toward intermittent rate hikes until you absolutely have clarity that inflation risk has been reduced. I don’t think we’re there yet as inflation risk is still pointed higher. Wage growth is occurring in out-of-sample fashion and relative to productivity growth. A 30% unionization rate makes collective bargaining much more important to the Canadian wage picture than the 10% unionization rate in the US and alongside IMF research that points to higher risk of spillover effects upon other segments of the labour market for countries with high unionization rates and full employment. Combined with poor productivity growth, Canadian unit labour costs (productivity-adjusted employment costs) have been accelerating for many years—ever since 2017—and with a super-acceleration now going on. This risks second round effects upon core inflation as someone has to pay for this and that I think are higher than some others think.

Add to this the fact that the economy has yet to take a material step toward creating disinflationary slack and hence hasn’t even begun the lagged-out influences upon core inflation. The Q2 GDP soft patch was probably mainly due to transitory shocks (wildfires, strikes, flooding, energy maintenance etc). July’s jobs report was fake as previously written. Retail sales don’t capture anything Canadians have been spending more money upon because in Canada they exclude all services which basically makes it a highly misleading account of the consumer sector as written here.

Opting not to hike and leaning instead toward guidance that says they won’t cut any time soon is a high stakes gamble in markets that rightly understand that the BoC’s models are hopeless when it comes to forecasting inflation and hence so is the much maligned tool of longer-term forward guidance. Markets, households and businesses don’t trust their forward guidance. Everyone should have learned that lesson by now even before the pandemic, let alone as the pandemic tossed models right out the window in my opinion. Actions matter more than words.

The BoC should not overestimate its control and influence further up the curve in the same way its forecasts tried to do at the July meeting when I wrote this piece. Consistency is required. The inability to forecast alongside persistent upside risks to inflation and with core measures still running around 3½% m/m SAAR alongside higher-than-target inflation expectations merits a continued hawkish bias—and the willingness to deliver. We are still very much in an environment whereby bond markets are on tenterhooks that require disciplined management by central banks willing to do whatever they have to in order to stay the course toward conquering inflation. If they don’t, then don’t complain when bond markets act accordingly.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.