ON DECK FOR THURSDAY, APRIL 27

KEY POINTS:

- Earnings buoy risk appetite

- US earnings are beating by the widest margin since 2021Q3, largely on revenues

- US Q1 GDP faces added last minute uncertainty

- US core PCE inflation could overshadow GDP

- US weekly claims, pending home sales on tap

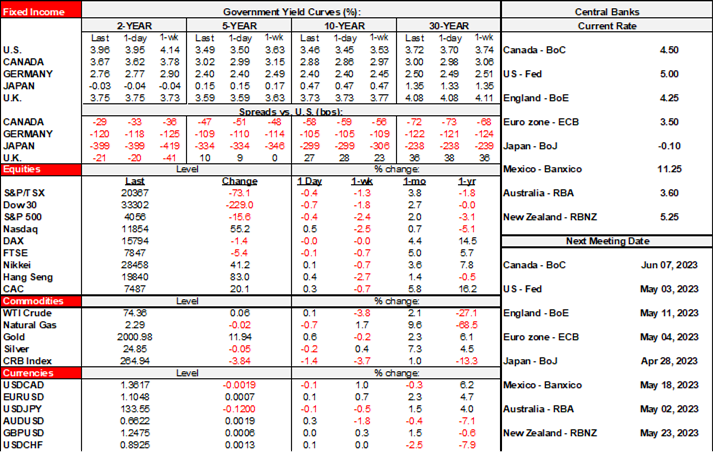

Earnings, US GDP and US core PCE will be the main focal points today. N.A. equity futures are up by about ½% and European cash markets range from flat to up ¼%. Asian equities also pushed higher overnight. Sovereign yields are gently higher everywhere. The USD is little changed on balance.

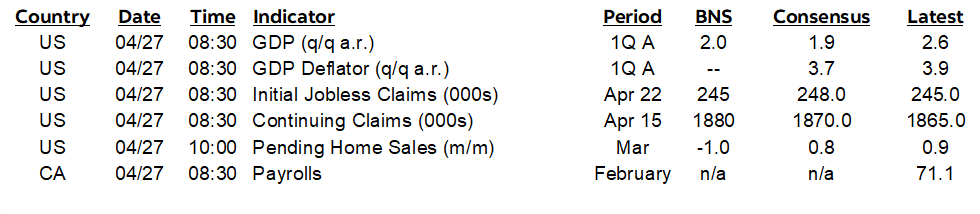

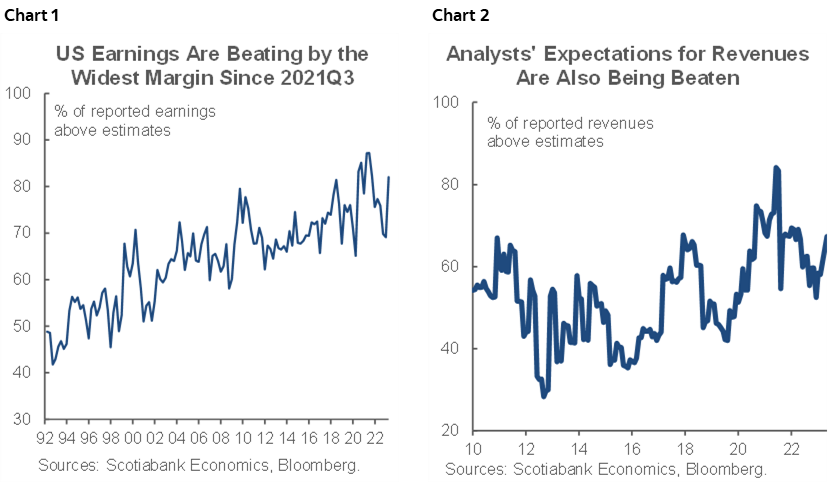

Earnings are buoying risk sentiment particularly in the U.S. as expectations were once again set too low as they have been ever since analysts moved the goalposts following the dot com and SOX clampdown. Chart 1 shows that US earnings are beating expectations by the widest margin in several seasons with 82% of reporting companies so far beating estimates. Chart 2 shows that much of this is due to revenues beating analysts’ expectations with the added kicker being cost cutting; 67.3% of firms are beating revenue expectations so far. A wave of overnight earnings reports out of Europe favourably added to sentiment following Meta Platforms (formerly Facebook) better than expected earnings and revenues last evening when eBay also beat. In the pre-market we got another beat from Caterpillar which is of macro relevance because its guidance can be useful in terms of what they are seeing for heavy equipment spending. The after-market brings out Amazon.

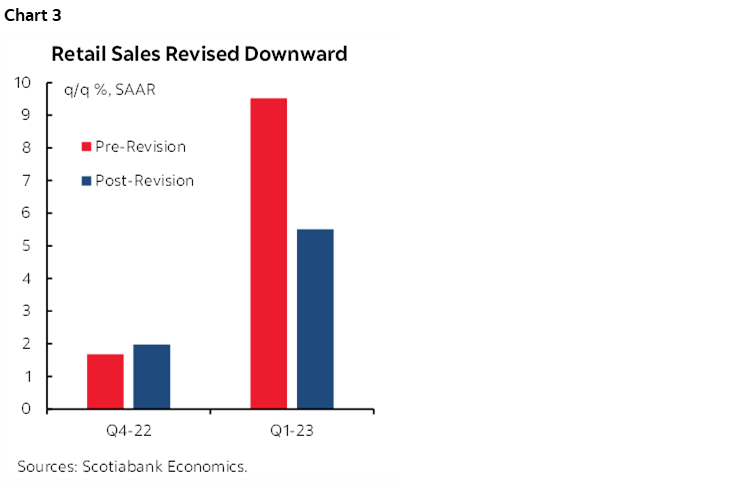

There is concern that Q1 GDP growth (8:30amET) could land materially weaker than consensus expects after downward revisions to retail sales that were introduced on Monday. I’m not so sure about that, but in any event the first pass is always guesswork that then gets revised multiple times until we get firmer data such as on services.

Sure enough, the retail sales control group (RSCG) that matters to GDP went from tracking a 9.5% q/q SAAR gain in Q1 to just 5.5% post-revisions. One caveat is that we don’t know how much of this revision was due to volumes versus retail prices and it is volumes that matter to GDP. Chart 3 shows the 2022Q4 and 2023Q1 revisions.

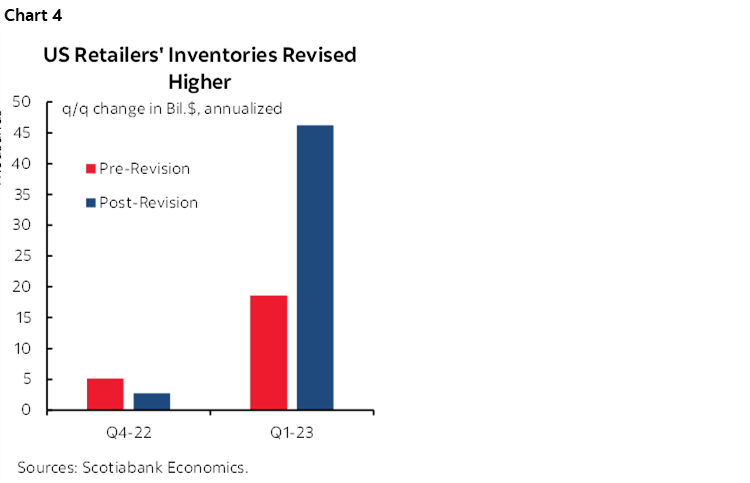

What offsets the downward revision to the RSCG, however, is that the retail inventory contributions to GDP growth moved sharply higher with revisions and yesterday’s March data. The swing in the flow of retail inventory investment went from about US$13B annualized in Q1 to US$43B for over triple the pace of investment in retail inventories post-revision compared to pre-revision (chart 4). That swing in inventory contributions to growth can be more than offsetting to the downward revision to the RSCG. Here too, however, we don't know how much of the revision was to real inventories versus nominal. Total inventories may be less of a drag on GDP than previously thought.

Also, if my estimate for March core PCE is right, then core PCE in today’s Q1 accounts will be up by about 4.7% q/q SAAR. There could be revisions to prior months and also March’s estimate faces uncertainty and will be implied in the quarterly number ahead of tomorrow's monthly estimates. Any surprise higher or lower on core PCE could dominate GDP in terms of market attention.

So could claims if they break out of the recent range (8:30amET). US pending home sales during March are expected to post a small rise (10amET).

Canada updates the seriously lagging payrolls report for February (8:30amET). We get the fresher and more complete Labour Force Survey for April next Friday.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.