ON DECK FOR TUESDAY, APRIL 11

KEY POINTS:

- Global markets passing time ahead of the week’s main events

- European bonds catch up to payrolls post-holidays

- Why the BoC should be hawkish tomorrow

- China’s credit expansion is on fire…

- …as lowered bank restrictions are being relied on over rate cuts

- Chinese core inflation remains weak

- Krone underperforms despite firm core CPI

- Light Fed-speak on tap

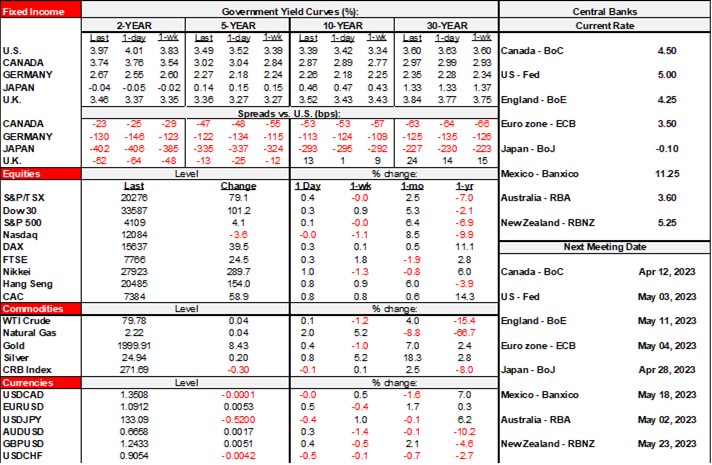

European markets are catching up to developments including nonfarm payrolls after being shut for Good Friday and Easter while markets everywhere await the week’s main events starting tomorrow (US CPI, BoC, Fed minutes) through Friday (US bank earnings). Gilts and EGBs are underperforming US Treasuries with European yields up by 10–14bps in 2s and in a 2s10s bear flattener move. Global equities are little changed and marked by flat N.A. futures and European cash markets that are mostly higher but not by a lot. The USD is a touch weaker.

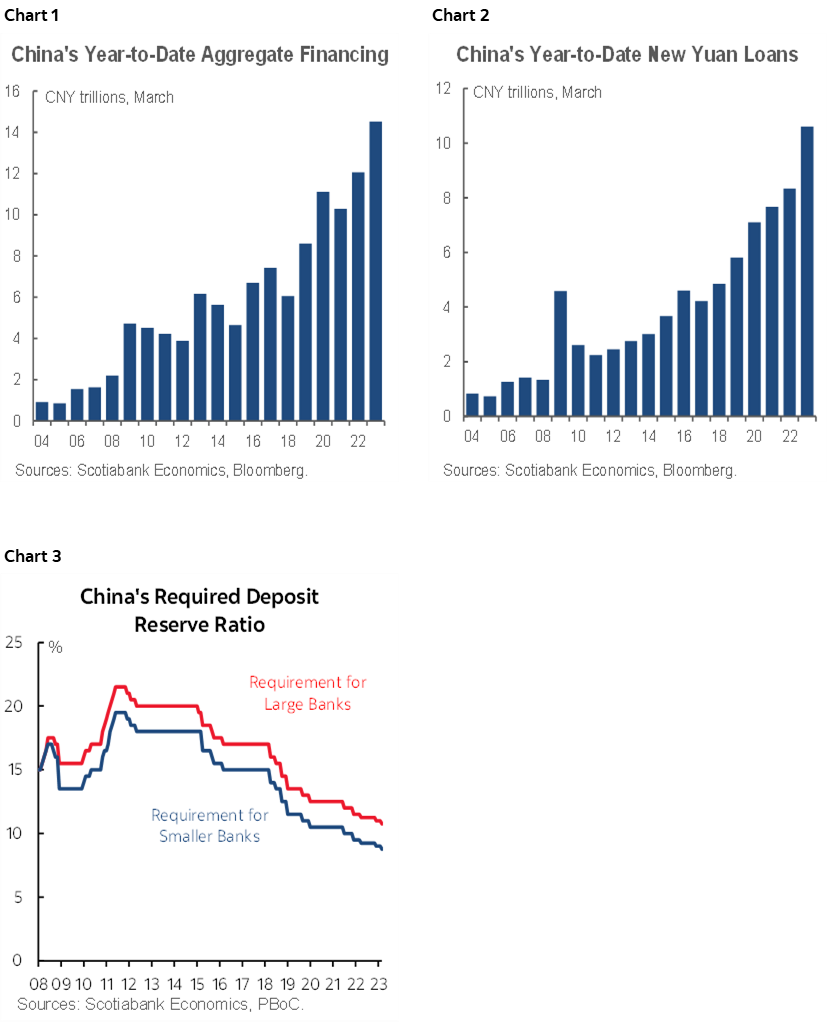

China’s monetary policy stimulus is flowing through credit figures as inflation remains very low. Aggregate financing surpassed expectations in March and for a third consecutive time this year. Ditto for new yuan loans. Both figures are registering their most explosive gains for the January to March period on record as shown in charts 1 and 2. This partially reflects reductions in required reserve ratios totalling 175bps since mid-2021 with 50bps of that reduction occurring since late last year. China’s long-term relaxation of requirements is shown in chart 3 that vividly depicts the country’s reliance upon relaxed lending standards over further rate cuts.

This is set against the backdrop of continued weakness in Chinese core CPI inflation that landed at 0.7% y/yin March (0.6% prior) and which is therefore not really new information. Core inflation has been under 1% for much of the past year. What is interesting is that China is so far not seeing a spurt of inflationary pressures following the abandonment of Covid Zero policies that would be akin to what happened elsewhere in the world as restrictions eased and economies reopened. Perhaps that still lies ahead. The PBoC’s ability to respond to very low inflation is limited by the stability implications of yuan weakness with the Fed not done yet in terms of rate hikes and particularly QT. That’s why they are relying upon easier credit conditions rather than destabilizing hot money flows.

The Bank of Korea held its policy rate at 3.5% as widely expected in a unanimous decision while five of six Board members guide that a higher rate remains possible which is likely geared toward leaning against betting on rate cuts.

The krone is the weakest of the currency pack this morning as core inflation merely met expectations with a 6.2% y/y rise (5.9% prior) and 0.6% m/m NSA. The m/m seasonally unadjusted gain was higher than normal for a month of March compared to history.

There is very little on tap into the N.A. session. Most of the emphasis will be upon Fed-speak including Chicago’s Goolsbee (1:30pmET), Philly’s Harker (6pmET) and the Minneapolis Fed’s Kashkari )7:30pmET) with two of them not speaking until after markets shut.

Canadian markets will face no incremental macro developments today as they await the BoC after US CPI tomorrow. A preview was made available in the Global Week Ahead (here). In my opinion, the BoC should sound incrementally more hawkish and open to doing more and here’s a partial list of the reasons for this view.

- The economy is proving to be resilient with a strong Q1 rebound that defies the over-reaction to softness in Q4 and is therefore making no real progress toward disinflationary slack 1½+ years after markets began anticipating BoC rate hikes. The sustained period of underperformance relative to potential GDP growth remains elusive as the bearish view keeps getting pushed out quarter after quarter after quarter. The BoC has to sharply revise Q1 growth up from its ½% q/q SAAR forecast to something that is several multiples higher and likely north of 3%.

- Measures of core inflation remain well above the 2% headline target in m/m seasonally adjusted and annualized terms. They have proven to be sticky for several months now.

- The Western Canada Select crude oil price is up by 50% from the low in December and buoying the terms of trade which continues to have the effect of an imported positive income shock to the economy.

- The 5-year GoC bond yield—a key determinant of the popular 5-year fixed mortgage rate—has dropped by over half a percentage point since early March and by over ¾% since October. Markets are pricing rate cuts this year that seem premature and it may be that they need a a determined reality check by a hawkish sounding central bank.

- The global shock to banks and markets in the wake of SVB and Credit Suisse has been tamped down and Canada’s banking system is on sounder footings than many others including thanks to a different funding model.

- China’s economy is on the rebound and once it burns off industrial inventories it should buoy commodities.

- Immigration stimulus is arriving in stark contrast to elsewhere in the world and it is arriving in the context of severe bottlenecks including a shortage of housing and basic infrastructure.

- Canadian governments continue to prime the pump while partisan defenders and typically favourable media outlets that support largesse miss the macro points that are deserving of a separate section and a tactful rebuke from the BoC couched in language that rests upon broad interpretations of the overall macroeconomic narrative. Macklem won’t say that fiscal expansion concerns him, but I very much hope that it’s on his mind.

- Federal program spending excluding temporary Covid supports surged by one-third from FY2019–20 before the pandemic struck to the just completed FY2022–23 period. That was almost entirely a surge caused by current consumption, not “investment.” Handouts would be a better term to use. The Budget plans to raise that cumulative spending growth to over 50% over its forecast horizon and I suspect there is more spending waiting in the wings whether examples include further expansion of state-funded dental care to state-funded pharmacare or perhaps election pump-priming.

- Incremental “investment” that was announced in the latest budget has become a euphemism for heavy current spending and massive subsidies to the white elephants of our time as Canada gets willingly pulled into a bidding war between the Biden and Xi Jinping administrations. Large, interventionist states are distorting the playing field and picking winners and losers at taxpayers’ expense while driving energy demand toward despotic regimes. These distorting subsidies prove yet again how global trade bodies fail us time and again and not just the rich world’s taxpayers; the developing world’s economies will find it impossible to compete against such subsidies and we’ll see what good it all winds up doing for the global environment over time. Canada is joining countries with big interventionist governments that are willing to spend large sums for each of the modest numbers of jobs created at the expense of activity elsewhere in the economy if more of the focus was upon setting the macro foundations for a healthier economy that is less distorted by big government spending. This is one reason why the argument that such subsidies represent “investment” that could aid potential GDP is rather exaggerated to say the least.

- How so? Fiscal stimulus is causing some of the inflation and with that some of the BoC policy rate hikes to date—both of which have their most punitive and regressive effects on often highly leveraged lower- and middle-income households.

- Higher rates are crowding out private investment that would have otherwise occurred by making the cost of capital more punitive than would otherwise be the case.

- Weaker private investment does not help the country’s huge productivity problem alongside persistent tightening of the job market. It harms it through the cost of capital and harms it through follow-the-subsidies financing distortions.

- Government hiring is directly causing shortages of workers as one-in-two new jobs since the start of the pandemic have been in the public sector including within that tally over 180k more civil servants. Civil servants threatening to go on strike in an effort to secure wage gains that would be well above the rate of inflation and when there has become a surplus number of them I might add. No wonder the country’s wealth-creating businesses cannot find workers to fill what are still massive vacancies. The lost economic output from these private businesses that cannot find workers is a stiff price to pay for all of that government spending.

- Interest payments on the debt are approaching levels (soon $50B/year) that are crowding out other initiatives and adding to stockpiling debt to be paid for by future generations. Yes, Canada’s debt is affordable now, but we’ve seen this movie about creeping relaxation toward deficit-financed consumption before and we know how it ended. Deficits are temporary, the budget will balance itself, surpluses lie ahead... and now its deficits forever with an endless list of spending proposals waiting in the wings.

Overall it’s my belief that if the BoC sounds incrementally dovish tomorrow then it will make a policy misstep. The BoC should repeat prior messaging about how they are more concerned about upside risks to inflation than downside risks and leave the door very wide open to further tightening as further developments are evaluated. Absent thus far is the knock-out blow to inflation risk.

DISCLAIMER

This report has been prepared by Scotiabank Economics as a resource for the clients of Scotiabank. Opinions, estimates and projections contained herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable but no representation or warranty, express or implied, is made as to their accuracy or completeness. Neither Scotiabank nor any of its officers, directors, partners, employees or affiliates accepts any liability whatsoever for any direct or consequential loss arising from any use of this report or its contents.

These reports are provided to you for informational purposes only. This report is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any financial instrument, nor shall this report be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The information contained in this report is not intended to be, and does not constitute, a recommendation of a swap or trading strategy involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individually tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any other transaction. Scotiabank may engage in transactions in a manner inconsistent with the views discussed this report and may have positions, or be in the process of acquiring or disposing of positions, referred to in this report.

Scotiabank, its affiliates and any of their respective officers, directors and employees may from time to time take positions in currencies, act as managers, co-managers or underwriters of a public offering or act as principals or agents, deal in, own or act as market makers or advisors, brokers or commercial and/or investment bankers in relation to securities or related derivatives. As a result of these actions, Scotiabank may receive remuneration. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. Officers, directors and employees of Scotiabank and its affiliates may serve as directors of corporations.

Any securities discussed in this report may not be suitable for all investors. Scotiabank recommends that investors independently evaluate any issuer and security discussed in this report, and consult with any advisors they deem necessary prior to making any investment.

This report and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced without the prior express written consent of Scotiabank.

™ Trademark of The Bank of Nova Scotia. Used under license, where applicable.

Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, including; Scotiabank Europe plc; Scotiabank (Ireland) Designated Activity Company; Scotiabank Inverlat S.A., Institución de Banca Múltiple, Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Casa de Bolsa, S.A. de C.V., Grupo Financiero Scotiabank Inverlat, Scotia Inverlat Derivados S.A. de C.V. – all members of the Scotiabank group and authorized users of the Scotiabank mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia is authorized by the UK Prudential Regulation Authority and is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available from us on request. Scotiabank Europe plc is authorized by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority.

Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V, Grupo Financiero Scotiabank Inverlat, and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.

Not all products and services are offered in all jurisdictions. Services described are available in jurisdictions where permitted by law.